")

")

")

")

")

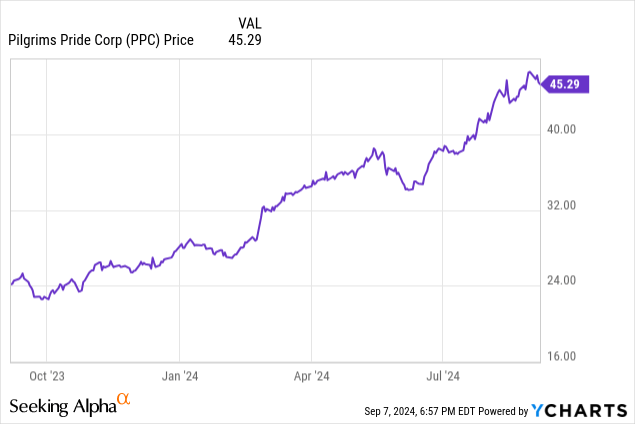

After stock prices have surged for months, meat products seller Pilgrim’s Pride (NASDAQ:PPC) is sitting at close to the top of its 52-week range. This time last year was, it seems, very much a good time to buy the company.

But what about now? We’re going to be looking at what the company is offering as a value stock and its potential to return value to shareholders, taking its higher share price into account, and see if it is still worth considering for people not already invested. Has the ship sailed? Hopefully, we’ll get a better idea.

Understanding Pilgrim’s Pride

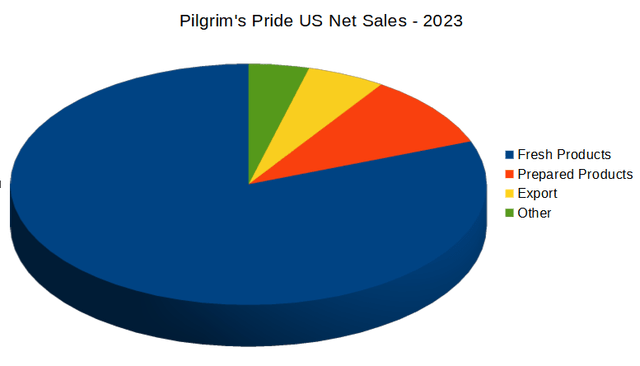

Most people in the US are likely familiar with the Pilgrim’s Pride name, and see it every time they visit a grocery store. The company is a seller of fresh and value-added chicken and pork products, which provides the products to retailers, distributors, and food service operators.

10-K from SEC

Fresh product sales are the overwhelming bulk of Pilgrim’s Pride’s business, especially in the US, its largest market. The company also has sales in the UK, Ireland, continental Europe, and Mexico, which they are hoping will be a source of growth in the future.

Balance Sheet

|

Cash and Equivalents |

$1.3 billion |

|

Total Current Assets |

$4.5 billion |

|

Total Assets |

$10.1 billion |

|

Total Current Liabilities |

$2.5 billion |

|

Long-Term Debt |

$3.2 billion |

|

Total Liabilities |

$6.2 billion |

|

Total Shareholder Equity |

$3.7 billion |

(source: most recent 10-Q from SEC)

Pilgrim’s Pride is quite a large company for a pure play on chicken and pork products. It is worth noting that the company has a fairly sizable amount of debt. While I don’t mean to suggest that this is a dangerous amount of debt, as the cash on hand and the current ratio of 1.8 shows they are in decent shape, but the large debt does likely limit their options for making major changes in the future.

The company is currently trading at a price/book ratio of 2.88. This is slightly above the sector median of 2.54, which to me is a bit of a red flag for a company that isn’t expecting much in the way of growth in the future. It is possible, with their price near the 52-week-high, that investors may have gotten ahead of themselves.

The Risks

Pilgrim’s Pride is a well-established company with important customers, but that doesn’t mean that they don’t face considerable risks that investors need to be aware of before considering an investment.

Dealing with a large number of chickens and pigs, the company is always at risk of a breakout of livestock diseases. A large outbreak could impact operations and could also scare some customers away from eating their products for a time.

Despite being a big provider of chicken and pork, they’re far from a monopoly, and there is a lot of competition, especially in the international market. This limits Pilgrim’s Pride’s ability to raise prices without facing a risk, and could be a drag on gross margins in the future.

Pilgrim’s Pride isn’t a big ranch either. The company depends on contract growers and independent producers for its livestock, which once again means they are subject to competition to keep their product moving to customers.

In the long term, they also face a risk if customers in their countries of operation decide their preferences are for less pork and chicken. Americans eat a lot of chicken these days, but that may not always be the case, and a decrease in demand could generally shrink the company’s business.

Statement of Operations

|

2021 |

2022 |

2023 |

2024 (1H) |

|

|

Net Sales |

$14.8 billion |

$17.5 billion |

$17.4 billion |

$8.9 billion |

|

Gross Profit |

$1.4 billion |

$1.8 billion |

$1.1 billion |

$1.1 billion |

|

Operating Income |

$211 million |

$1.2 billion |

$522 million |

$691 million |

|

Net Income |

$31 million |

$746 million |

$321 million |

$501 million |

|

Diluted EPS |

13¢ |

$3.10 |

$1.36 |

$2.11 |

(source: most recent 10-K and 10-Q from SEC)

Though far from a growth company, Pilgrim’s Pride has seen some increase in revenues in recent years. Unfortunately, the company is not seeing similar growth in its gross profits, and the margins seem to be under some pressure.

Estimates are that 2024 is going to be a very good year for Pilgrim’s Pride, with expectations of an $18 billion revenue and earnings of $4.51 per share. That puts them at a P/E ratio just over 10, which is quite a bit below the sector median. It’s not going to completely last, however, as 2025 is going to see a slightly higher revenue of $18.45 billion, and earning down to $3.98 per share. That’s a forward P/E of 11.37, which is still decent, but not exactly the direction we want to see.

In late July, Pilgrim’s Pride came out with earnings which showed they were beating earnings per share on a non-GAAP basis, and only narrowly missed on revenue.

If there’s one disappointing thing about a company that has pretty strong earnings, it’s that Pilgrim’s Pride does not pay dividends, and has no intention of paying any in the future. To be fair, the company’s debt probably limits their ability to return value to investors in this way, but to my thinking, even a small dividend would be a vote of confidence in the company’s position being sustainable in the long term.

Conclusion

Pilgrim’s Pride has been very good to people who bought in the past, but at these levels, I have to say I’m not a huge fan of the stock for a value investor. The price is just too high for a company that seems to be priced on the assumption that everything will continue to go right for them.

With current debt levels and the lack of any dividend at all, I just don’t see the appeal to investing at this point. I’m rating the stock a hold because it isn’t by any means a bad company, but the price its shares trade at doesn’t offer very much at all for new investors to like.

I would continue to keep a close eye on where the gross margins are going for the company in the future, as if it continues to shrink, the company likely is not going to see revenue growing enough to keep its earnings at the high range expected in the near term.

Read the full article here

")

")

")

")

")