")

")

")

")

")

An Ambitious Firm From the Start and Still Staying Afloat

It’s still early September, and as we head into a new trading week one, the stock that came across my watchlist is actually a firm I worked at several years ago as an IT contractor, and happens to be one of the largest financial firms in the US.

The Charles Schwab Corp. (NYSE:SCHW), according to its SA profile, is a Texas-based firm that “provides wealth management, securities brokerage, banking, asset management, custody, and financial advisory services,” and has been in business since the early 1970s, currently trading on the NYSE.

Those who follow the brokerage sector may know that company founder Charles Schwab is known for being a pioneer in the discount brokerage business.

In the company’s own words:

Schwab’s corporation took an early lead, offering a combination of low prices with fast, efficient order executions, and soon became the nation’s largest discount broker. Today, it’s the nation’s largest publicly traded investment services firm, with over three trillion dollars in client assets.

I would say this is a highly competitive sector, and in today’s article the 3 peers of Schwab that I will use as comparables will be Morgan Stanley (MS), Goldman Sachs (GS), and Raymond James Financial (RJF), which incidentally are listed by SA as this firm’s peers.

For example, E*TRADE was a major discount brokerage that was acquired by Morgan Stanley, while another major brokerage, TD Ameritrade was acquired not long ago by Schwab. Raymond James and Goldman, from my perspective, are competitors in the wealth management space, as is Morgan, although Goldman Sachs does not have a discount brokerage shop.

In a May article, US News & World Report listed Goldman Sachs in the 7 top financial advisor firms, while Barron’s listed Morgan Stanley private wealth management teams in 6 of the top 10 for 2024.

So, as we can see, Schwab is playing in a lake with a lot of big fish and a whole lot of money being managed for clients, so this picture should paint the backdrop for our discussion today to determine if this stock is a buy, sell, or hold at this time.

Currently Trading Below its Moving Average

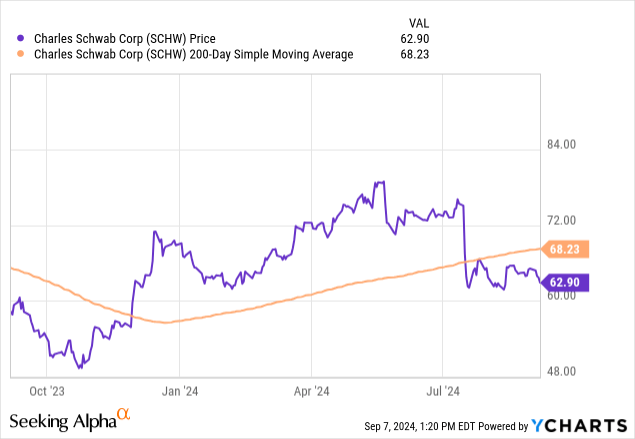

What catches my attention is that Schwab is trading at just $62.90 as of Friday’s close (and the writing of this article), almost 8% below its 200-day SMA and not having recovered yet from its summer price dip, as the YCharts below shows.

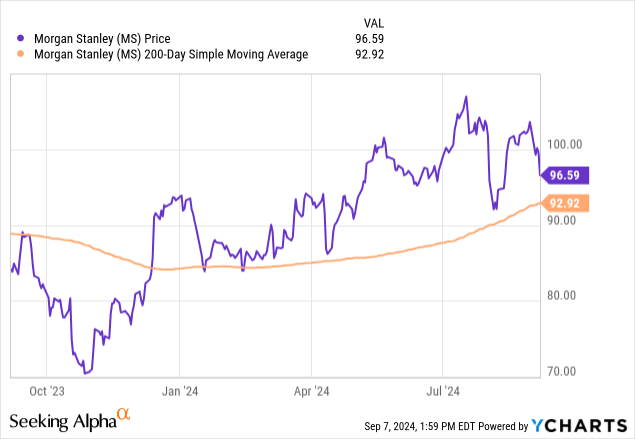

By comparison, its key competitor I would pick from the peer group, Morgan Stanley, is trading well above its 200-day SMA, as the graphic shows:

What could be some causes for the drop in Schwab shares?

For one thing, an August article in Barron’s indicated the following:

Canada’s TD Bank has set aside $2.6 billion for fines it is likely to face from U.S. regulators. That’s bad news for Charles Schwab, because TD sold shares in the wealth manager to help offset the hit.

Further, July’s report by Investopedia highlighted another impact facing this firm’s stock:

Charles Schwab shares plunged after the financial services firm warned it would be downsizing its bank to maintain profitability.

The financial site went on to report that Schwab missed analyst estimates on growth of new brokerage accounts, and this sent shares plunging this summer.

However, my sentiment is that these are short-term and temporary events, and looking to the future we could see a more streamlined firm come out of it which would make sense for shareholders.

Not only that, but this price drop below the SMA could present a buying opportunity for the savvy value investor. The good news is that the firm is still a steady dividend payer and profitable, two areas I will discuss next.

Dividend Stability But Low Yield

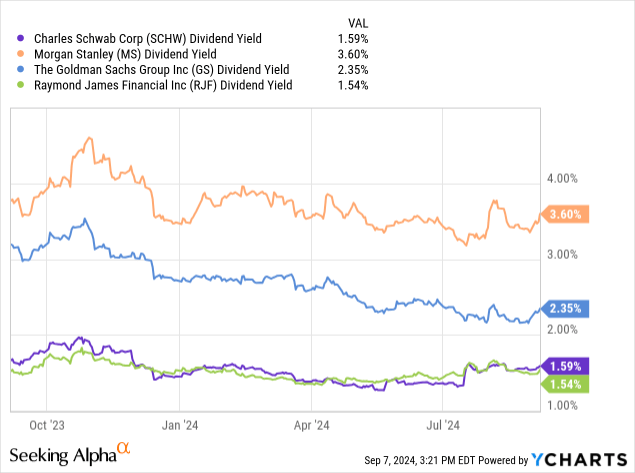

The following study I created compares the dividend yield of Schwab vs the 3 peers I selected, showing that Schwab which has a quarterly payout of $0.25/share has a dividend yield of 1.59%, which is towards the bottom of this peer group. I care about dividend yield because it gives me an idea of what my invested capital will yield on dividend income, compared to investing in another firm. In this case, Schwab does not present a very attractive yield.

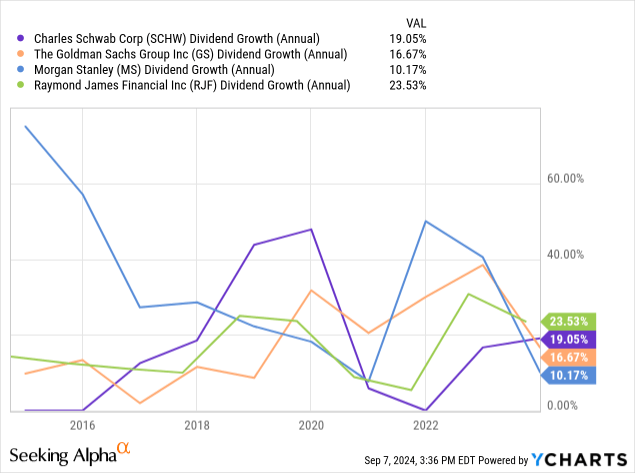

Next, we know from SA dividend growth data that Schwab has a proven track record of steadily growing its dividend over the last 5 years, and currently with a payout ratio of 34.25%, which is essentially the percentage of earnings paid out to shareholders as dividends.

When looking back at the last decade, Schwab’s annual dividend growth was in the top two of this peer group comparison, and as the graphic below shows they made a nice recovery in the post-pandemic period after the 2020 drop.

This tells me that Schwab is an established dividend payer and continues to have the cash on hand to pay shareholders, although the quarterly payout of $0.25/share remained the same after they declared their dividend in July, which usually tells me they are wanting to hold on to more of their cash for now.

I think whether its dividend will be sustainable a year from now and continue to grow will depend on continued earnings growth, so in the next section let’s talk about recent performance and future earnings potential.

Despite Recent Earnings Growth, Analysts are Skeptical

With its next earnings not due until mid-October, let’s briefly recap how their Q2 results looked, and give my thoughts on where this firm could be in a year.

Beating earnings estimates, in Q2 Schwab saw a YoY growth in net income, driven by YoY growth in top-line revenue, according to SA income statement data.

Although net interest income fell on a YoY basis, as did trading income, the firm saw YoY growth from asset management fees, which tells me that this is an important business segment of this firm for analysts to keep an eye on. In fact, it appears from income statement data that it is +29% of total revenue, so 1/3rd of their top line is benefitting from asset management.

One factor that could impact future asset management fees, but also future revenue from its brokerage business, is recent/current growth in clients and accounts in those two segments, which could lead to those future revenue flows in a year assuming those new clients stay with the firm.

What we know from the firm’s Q2 earnings release is that “active brokerage accounts increased 4% YoY to 35.6 million.”

In addition, “client assets receiving ongoing advisory services are up 16% YoY, including YTD net flow increases.”

Keep in mind that Schwab has an entire series of its own mutual funds, called Schwab Funds, and it earns fees from managing those too, so the more client monies flow into those funds the more fees can be earned potentially.

According to the Q2 results, “strong YTD net buying of mutual and exchange-traded funds totaled $77B – the 2nd highest first half ever.”

I should mention that net client flows are not the only way the firm could grow fees, but also equities market growth which can drive up the underlying values of equity assets and the fees earned on those assets.

At the same time, mutual funds that are primarily bond funds and not equity funds are affected by the underlying value of the bonds, and we know that Fed rate decisions can impact bond values.

So, I think since CME FedWatch is predicting that the Fed will start a rate lowering cycle soon, it could eventually boost the value of fixed-income assets that Schwab is holding or managing, but can also lower interest income the firm earns in a year.

For now, other analysts seem to be saying in their estimates that the firm will see an EPS of 3.05 in December 2024, a YoY decline, while 19 downward revisions have already been made on this stock with 0 upward revisions.

A key event happened that impacted Schwab not long ago, and next let’s talk about the risk that entails for this firm.

Risk Picture Impacted by Recent Downgrade

According to a news article from Seeking Alpha back in July, the firm got hit with a downgrade to neutral from overweight from Piper Sandler (PIPR), and here is why:

Specifically, the company said earlier this month that it may look to reduce its bank level debt over the next several quarters, a move that may affect its stock buyback plans.

While we do not disagree that a less capital intensive model could be a positive for (SCHW) in the long run (and likely warrant a higher multiple), it adds an element of near term uncertainty that we believe will be an overhang on shares for several quarters,” analyst Patrick Moley wrote in a note.

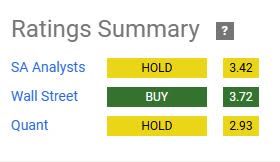

I think a downgrade like this from such a prominent firm like Piper certainly is a major impact to this stock, and we can also see from the below graphic that the SA analyst consensus and SA quant system are both neutral on Schwab, while Wall Street continues to be bullish.

Schwab – ratings (SA)

Because of this mixed sentiment on Schwab stock, another risk factor I want to consider is their financial health overall.

Schwab’s Stress Test Successful

With a tier 1 leverage ratio of 9.4%, well above the 6% minimum standard, what we know further from the company’s official Q2 statement is the following from the CFO:

Similar to prior years, our strong capital levels and all-weather model enabled us to successfully complete the 2024 Federal Reserve stress test, with Schwab notching the highest post-stress ratios among all major banks.

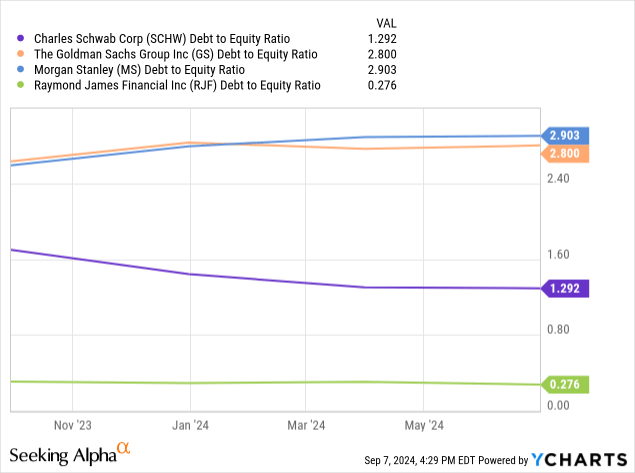

The stress test result certainly adds confidence to my sentiment on Schwab, in addition to the following study I created which shows that Schwab is on the lower end of debt-to-equity ratio among this selected peer group.

For now, I am positive on this stock but let’s see if the current valuation makes sense or not, and why, which leads into the next topic.

Valuation Shows Investors Paying a Premium

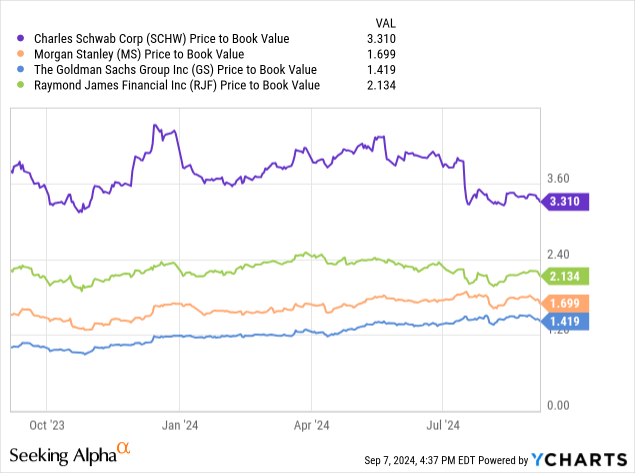

Because this is a financial firm which has a considerable amount of assets on its balance sheet, to the tune of $248.55B worth of investments in debt and equity securities, let’s first look at this firm’s price to book (P/B) ratio compared to peers:

What this graphic tells me is that Schwab exceeds this peer group in P/B ratio, which tells me investors are paying a premium over the firm’s book value, which, I think, is a show of confidence in this firm’s future success. Earlier I mentioned that if the predicted Fed interest rates come down, over the next few years, it may boost the value of bonds the firm holds, potentially boosting its balance sheet.

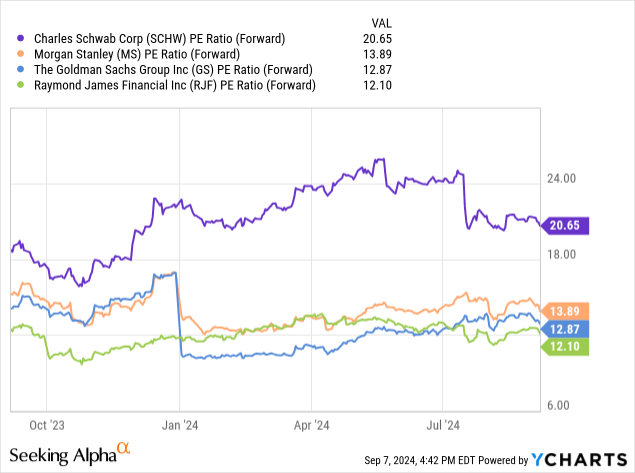

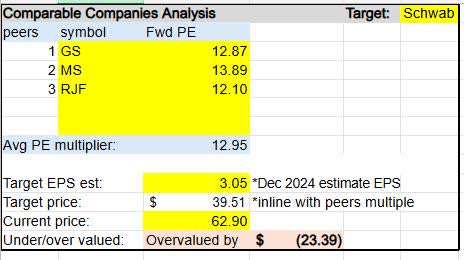

Next, what does forward price-to-earnings (P/E) tell us? What the graphic below shows is that investors are paying a premium on this stock in terms of future earnings potential, in terms of forward P/E ratio, with Schwab being the most overvalued in this peer group at a forward P/E multiple of 20.65.

Keep in mind that the Piper downgrade I mentioned earlier was not due to concern over profitability or liquidity but the ability of the firm to engage in stock buybacks in the near future, so I think this overvaluation on this firm is justified as I am expecting that the growth in brokerage accounts and asset management clients will help grow future earnings, while potential for lower interest rates heading into next year could mean a better interest margin with lower interest expenses for the firm.

Using my comparable companies analysis tool, I created below when using the average forward P/E multiple of the peers a share price for Schwab in line with this multiple and its December EPS estimate would be closer to a price of $39.50 to $40:

Schwab – comps analysis (author work)

So, it is currently trading at $62.90, or about $23 above this target price. While it may appear wildly overvalued, in the next and final section I will give my thesis on why I would still consider this valuation as justified.

An Opportunity to Own a Top 20 Bank in US For A Below-Average Price

To summarize my talking points on Schwab today, the positives of this stock are future revenue growth potential from current growth in new clients, future rising values of fixed-income securities if interest rates fall, the fact that the firm passed the Fed’s stress test which is a huge plus in this industry that has seen several struggling regional banks, a Tier 1 ratio above regulatory minimums and low debt-to-equity ratio vs peers, proven profitability over many quarters and expected ability to sustain or eventually hike its dividend again.

At the same time, some concerns are the downgrade from Piper, which could scare many investors away from this stock in the short term at least, along with the 19 downward revisions to earnings estimates, and the paltry dividend yield below 2%.

My clinical impression is that it is a modest buy rating, and in fact it is my first buy rating of the month, so I’ll be siding with the Wall Street bulls on this one.

What tipped the scale for me into the buy category was that it is trading well below its moving average yet has strong fundamentals: proven profitability, potential future growth, well capitalized, stress test passed, and a highly diversified banking model (bank, brokerage, asset manager, wealth advisor) all under one very recognizable brand umbrella and according to Wikipedia it is actually the 12th largest bank in the US, with a market cap of $125B as of last year, and over +$400B in assets.

My buy target is the current price range of $62.80 – $62.90, with the expectation it will climb back above its moving average and soar further in a year, driven by the factors I mentioned in this summary, while the Piper Sandler downgrade eventually fades away, I think.

Further, the banking sector overall has seemed to recover nicely from the regional bank failures a few years ago by Silicon Valley Bank and others, and Schwab along with its peer group has proven that it can withstand such turbulence and continue to steer the ship to port.

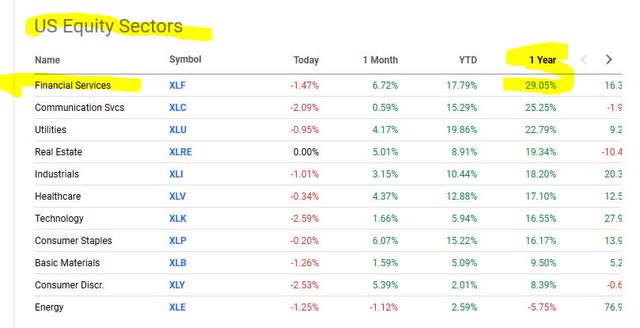

To end on a positive tone, SA market data in the table below clearly shows the financial services sector being the top performer of all sectors in the last year:

market data from SA (SA)

To echo what an August article in Fortune said, “If the federal funds rate declines later this year, rates on everything from credit card APRs to mortgages will follow.”

This, I think, could spell a hurricane of new customer demand for borrowing at the lower rates, and therefore not bad news for Schwab’s banking business either.

Read the full article here

")

")

")

")

")