")

")

The iShares Russell 2000 Value ETF is a poor proxy for the smallcap value premium. I do not agree with the actual factors used to determine value. In addition, the fund by design includes growth stocks. This is a fund built for a large amount of AUM and not for accurate capture of the small value premium.

The Small Value Premium

In 1992, Eugene Fama and Kenneth French designed what is now known as the Fama-French 3 factor model. It was an attempt to improve on the capital asset pricing model to explain the excess returns of stocks. The 3 factors are the market returns minus the risk-free rate, size and value. In general, small value stocks outperformed. Price to book was the factor used to determine value.

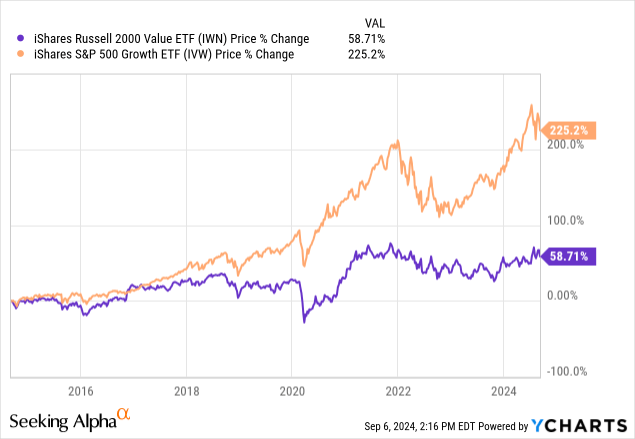

Well if that is the case, then why is the small-cap value fund getting absolutely pounded by the large-cap growth fund?

[object HTMLElement]

Measuring Value

Price to book is an old school financial ratio used by legendary investors such as Benjamin Graham. Book value is value of assets minus liabilities. While this value metric may still have some utility, it is becoming increasing less useful as many companies, particularly in the tech industry, have less assets than traditional firms. I prefer to use a combination of value factors such as the following:

- Price to Sales

- Price to Operating Cashflow

- Price to Free Cashflow

- Price to Earnings

- Price to Book (both tangible and intangible)

How IWN Measures Value

According to the Russell index construction methodology document, Value is measured using 3 factors:

- Price to book

- 2-year earnings growth forecast

- 5-year trailing sales growth

50% of the weight is based on price to book at the other 50% is based on the growth factors. Already, I see a major problem. Not only is the price to book ratio a bit outdated and needing complementary value factors, but now they are mixing it with growth factors.

Admittedly, value stocks will often exhibit low growth both trailing and future expected. But this doesn’t mean that low growth is the same as deep value. What about the PEG ratio made famous by Peter Lynch where you compare value to future growth? Growth and value are not mutually exclusive. You can have both. In fact, the best performing stocks are often ones that have value and are under the radar with higher-than-average growth. By the time mainstream investors figure out what is going on, you can take the ride while the multiple expands.

This is a serious strike against the fund as I don’t believe that these 3 factors are useful in finding pure value stocks. But it gets worse.

Value vs. Growth Scores

The index methodology document goes on to relate how it determines weighting. The 3-factor ranking system determines a composite score. The more ‘value’ a stock is, the less ‘growth’ it is. And vice versa. A stock will be fully represented between the growth and value index. This might sound confusing but stay with me and I will explain why this is a poor methodology.

- To make this simple, assume we have just 10 stocks. We want to create 2 funds – a value fund and a growth fund. Now the easiest way to create these funds would be to take the 5 funds with the best value ratios and the 5 stocks with the best growth ratios and make 2 funds. It is even possible that one stock would be in both funds if it had both strong value and growth properties.

According to the methodology of this Russell index, we instead use a combined value plus growth ranking system. A stock that is ranked 70 out of 100 on the growth scale is clearly a growth stock. This growth stock would get 70% of its weight in the growth index and 30% of its weight in the value index. Do you see the problem here?

- First, if we determine the stock to be a growth stock, it should have zero weight in a value index.

- Second, very large growth stocks are going to have an even greater influence on the value index. Value stocks often have smaller market-caps due to the multiple compression. The biggest stocks in an index have a growth tilt.

As an example, I took the top 100 weighted stocks in the ETF. I created a ratio of price to book of the stock compared to the industry group average. You would assume that the stocks should have a P/B ratio less than the industry average. But only roughly half of them did.

The median price to book ratio of the Russell 2000 index is around 1.6 – 1.7. And the median price to book ratio of the top 100 weighted stocks in the Russell 2000 value index is just under 1.5. Not a big value tilt at all.

Their methodology makes 2 errors in my view. The first is by assigning ANY weight of growth stocks in the value index. The second is that by doing this according to cap weight, both the size and the value premium are being diluted heavily by larger growth stocks.

But there is yet another reason for my dislike of the Russell 2000 value ETF.

Lack of Junk Filter

The problem with smallcap stocks is that there is a lot of high-risk junk in the mix. The one good aspect to their being a lot of junk is that this can create value in stocks as many investors turn their nose at it. I consider any stock that is not profitable as being at higher risk. Story stocks may spin a powerful narrative of huge future growth yet they are not profitable. And the stock continues to take on additional debt or dilute shares while they sell the dream.

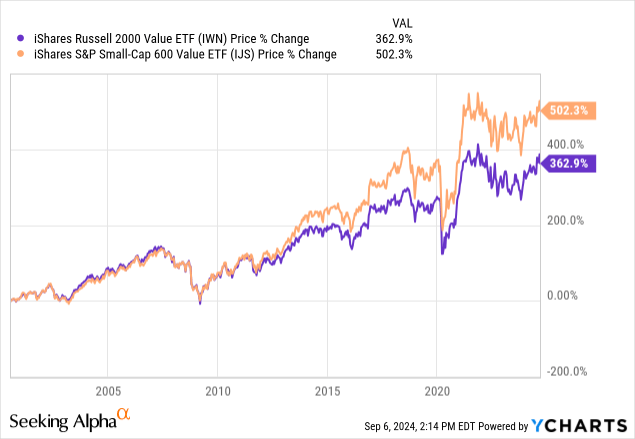

The S&P 600 smallcap index realizes the value of a profitability filter. To be in the S&P 600 a stock needs to have its most recent quarter earnings and trailing 12 months be positive. I have studied this extensively and use free cash flow instead of earnings (although they are highly correlated). But the point is the same, small stocks with positive profitability perform better as a group.

The chart below compares the Russell 2000 value ETF with the iShares Small-Cap 600 value ETF.

[object HTMLElement]

The Russell 2000 value index makes no effort to remove this stocks. And there is some suggestion that the smallcap universe is getting increasingly junky with time as large companies such as Google buy up smaller private firms with potential. If a firm does not get bought up, this leaves the public equity market as a second-best exit strategy for early investors. Which means we need an increasing amount of critical filtering in smallcaps with time.

Simple Alternate Russell 2000 Value Index

I created a very simple index which highlights how poorly the Russell 2000 value index really is. The steps are as follows:

- Start with the Russell 2000 index (I approximate this as closely as I can using point in time data)

- Remove stocks with negative free cash flow (quarterly and trailing 12 months)

- Keep the 800 stocks with the best price to sales ratio

- Hold stocks equal-weight and rebalance and reconstitute every 52 weeks

portfolio123.com

This is a very simple model.

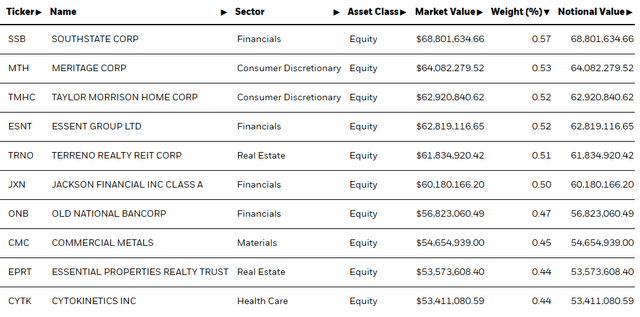

Top 10 Stocks

This is a list of the top 10 stocks. You will notice a lot of financial stocks on the list.

ishares.com

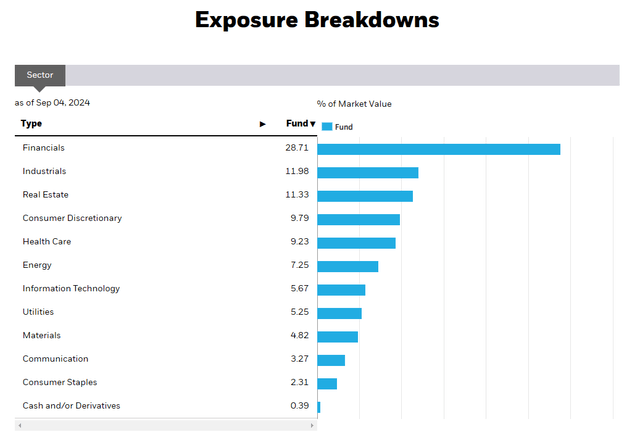

And the sector weighting shows this to be true.

ishares.com

However, I am not overly concerned by the sector weighting. This may change over time. But what will remain constant is the poor portfolio construction methodology.

Final Thoughts

The Russell 2000 Value ETF has zero appeal for me. The factors used are both outdated and unrelated to the value factor. Their weighting methodology favors both larger stocks and includes stocks with a growth tilt in the fund. A lack of profitability filter is also a serious ongoing concern. If you are looking for the size/value premium, I would look somewhere else. This fund was built to handle a lot of AUM and not much else.

Read the full article here

")

")

")

")

Q4 2024 Earnings Call Transcript")