")

By Christopher Gannatti, CFA & Bradley Krom

A central story of markets over the past few years could be ripe for change. The U.S. Federal Reserve transitioned its policy rate away from the so-called zero boundary and moved it up significantly. Relative to other major central banks, such as the Bank of Japan, the Bank of England, the European Central Bank or the Swiss Central Bank, the policy rate moves out of the U.S. were significant in both magnitude and speed.

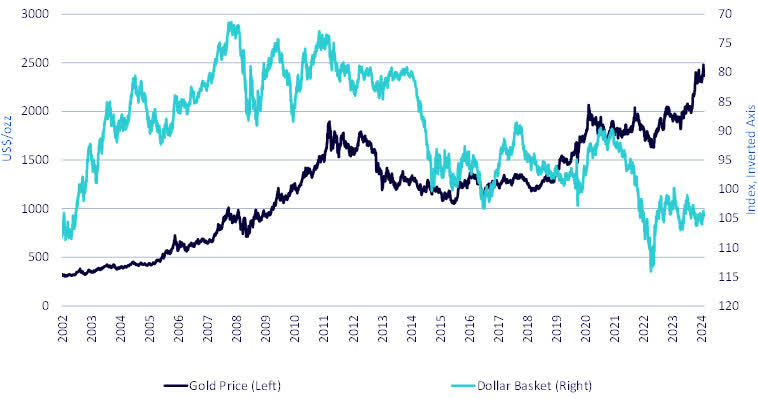

The result, as we can see in figure 1, is that the U.S. dollar (USD) appreciated against major global currencies, from a level of about 90 as of 2021, to nearly 115 in 2022.

- One interesting juxtaposition that we can see in figure 1 is USD and the price of gold. Since gold is priced in USD terms, the assumption is that as the dollar strengthens, all other things being equal, the gold price should fall. However, from 2021 to the present, the price of gold has trended higher.

While it may be tempting to say that this trade has run its course, if USD’s appreciation trend changes as a result of the Fed easing monetary policy, the dampening impact on the price of gold from a strong dollar could mean enhanced returns for investors.

Figure 1: Gold and USD Basket

Sources: WisdomTree, Bloomberg. Data is from June 2002 to April 2024. Data frequency is daily. Past performance is not indicative of future results.

Gold and Equities in a Portfolio

Historically, many investors have used gold as a strategic piece of their asset allocation. Their rationale is that as gold is the “original store of value,” they want to own it to help bolster traditional assets like stocks and bonds during periods of high inflation or market unrest. The challenge for this type of strategic allocation is that it requires reducing either stocks or bonds. Historically, both these assets have tended to outperform gold over market cycles, resulting in a less efficient portfolio and lower returns.

In our opinion, there may be a better way to allocate to gold, combining equities and gold to help overcome this problem in asset allocation.

Gold Overlays and Capital Efficient Allocations

WisdomTree is a leading proponent of overlay strategies where you can, within one strategy, stack the returns of more than one asset class through the use of leverage. Simply put, leverage means that for each dollar of exposure, it is possible to gain more than one dollar of exposure.

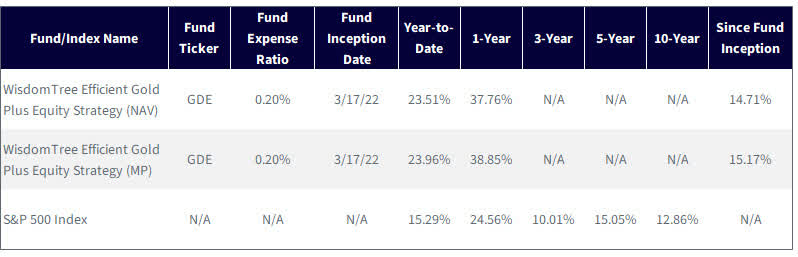

The WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE) seeks total return by investing in a portfolio of U.S.-listed gold futures and U.S. large-cap equities. For every $100 of investment:

- $90 of exposure to large cap, U.S. equities

- $90 of exposure to gold futures

- $10 held as collateral in U.S. Treasury Bills

So, for an investment of $100, there is $180 of exposure. With this Fund, investors are able to target a specific allocation to gold while maintaining their exposure to equities. During periods when gold outperforms equities, GDE can potentially offset losses relative to a 100% equity portfolio or reduce volatility.

Figure 2: Year-to-Date Returns

Source: WisdomTree, as of 9/4/24.

So far in 2024, both equities and gold have delivered impressive returns. As a result, a leveraged strategy like GDE has outperformed a 100% equity and a 100% gold portfolio. While this may not always be the case, this is one example of how investors could potentially maintain exposure to core assets like equities, while at the same time generating returns from investments in gold. If people are thinking that the value of USD may fall, it’s possible that gold’s price could continue to appreciate-a positive source of return within this strategy.

Figure 3: Since-Inception Returns

Source: WisdomTree, as of 9/4/24. Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For the most recent month-end performance, click here.

WisdomTree launched our first capital-efficient strategy in August 2018, which focused on an overlay of U.S. Treasury futures on top of equities to mimic a traditional 60/40 portfolio. Realizing that gold has the potential to hedge portfolios in a similar way to bonds, we continued expanding that overlay concept, launching GDE in March 2022. Since then, the market has experienced a variety of shocks and challenges, resulting in periods when equities have outperformed and underperformed gold. In periods when both gold and equities are negative, that has resulted in drawdowns for GDE. However, investors would have experienced negative performance in their traditional portfolios as well.

Figure 4: Standardized Returns

Source: WisdomTree, as of 6/30/24. Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For the most recent month-end performance, click here.

Catalysts for Gold

It is difficult to go through 2024 without thinking about geopolitics. Russia is still at war in Ukraine. There remains significant tension and fighting in the Middle East between Israel and Hamas. Even though China is not fighting the U.S. in a kinetic war, the tone of “U.S. vs. China” is still emphasizing tension and rivalry over collaboration.

Few asset classes have remained in use over more than 1,000 years. There have been dominant societies that have created empires that have risen and fallen. However, gold is one of the only things that has stood the true test of time. Every currency backed by solely the full faith and credit of a government has ultimately depreciated into insignificance-though some were around quite a long time.

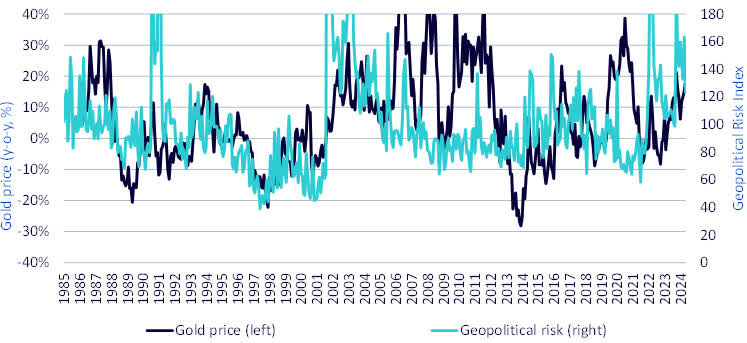

Still, we see in figure 5 that geopolitical risk is another factor that could be pushing upward on the price of gold as we move through the rest of the year.

Figure 5: Gold and Geopolitics

Sources: Dario Caldara and Matteo Iacoviello’s Geopolitical Risk Index based on a tally of newspaper articles covering geopolitical (war) tensions, Bloomberg and WisdomTree. January 1986-March 2024. Past performance is not indicative of future results.

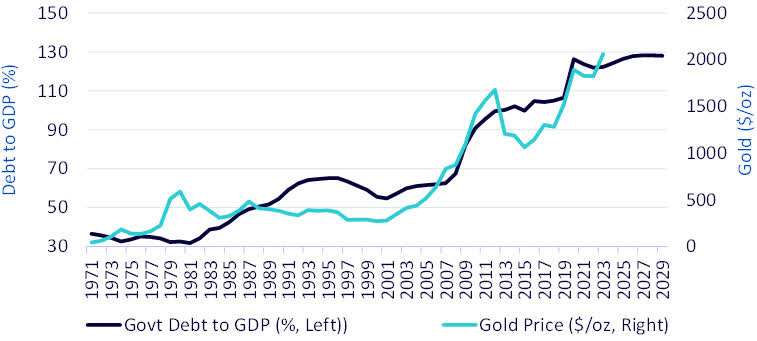

Now, 2024 is also an election year, which means that we will hear how different candidates and legislators globally will be promising all sorts of things. Some will promise the government will spend more and do more; some will promise that taxes will be lower to let people and businesses do more and spend more. Few policies, if any, will lead to lower U.S. government debt over time.

We see in figure 6 that the price of gold has a very positive association with the level of debt to gross domestic product (GDP) in the U.S. If this relative indebtedness continues to rise, it could be a factor pushing the price of gold higher.

Figure 6: U.S. Government Debt and Gold Prices

Sources: WisdomTree, Bloomberg, White House Office of Management and Budget (federal plus other agency debt estimates). 1971 to 2022 actual, 2023 to 2028 forecast. GDP is gross domestic product. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

Gold is unique in that it is one of the only things intertwined with human history for a few thousand years. It can be viewed as more of a monetary asset, but it can also be viewed as a commodity, with a distinct level of supply and demand and mining like many other commodities.

The price of commodities can be boiled down to supply and demand. If the gold price is rising, simply put, we have more buying pressure in the market than selling pressure. Many times, investors are interested in who is doing this buying. The global exchange-traded product market-even if you don’t know all the underlying buyers-is useful in that it is easy to see the flows into and out of different gold investment vehicles in different exchanges.

The first half of 2024 was confusing for many investors because the exchange-traded product data was not showing a lot of demand to allocate to gold, but the price of gold was rising significantly.

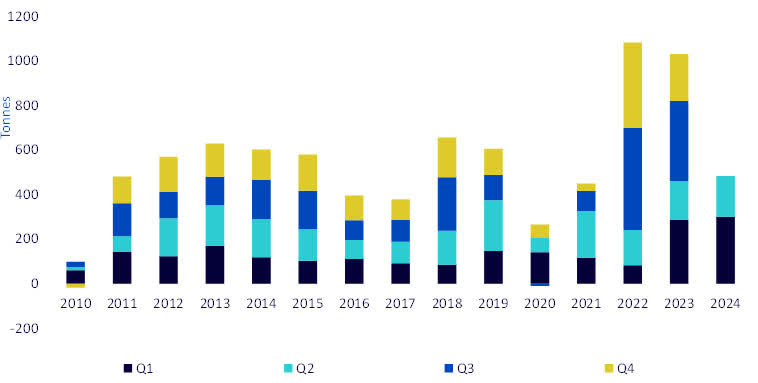

Another big source of demand for gold can be central banks, although the data on central bank buying is not always as transparent or “real time” as that of exchange-trade products. Figure 7 breaks down central bank demand for gold by calendar quarter.

- Looking at where we are so far in 2024, the demand looks very similar to 2023, and going back to 2010 there is not another year when this level for the first half of a given year was attained. We are on pace to see another year similar to 2022 and 2023-notably the two high years in this time series.

One can never, of course, guarantee the future on things like this, but central bank buying is another detail that could be pushing the price of gold more upward than downward.

Figure 7: Central Bank Demand for Gold

Sources: WisdomTree, World Gold Council, Q1 2010 to Q2 2024. Past performance is not indicative of future results.

Now, part of what we may have seen in July 2024 is a change in trend:

- For the better part of two years, we saw the ChatGPT Moment, which began in late November 2022, catalyze very strong share price appreciation within certain large companies with a compelling story connected back to the proliferation of artificial intelligence. The returns were so strong-and the companies subsequently became so large on a market capitalization basis-that we started calling these firms the Magnificent 7.

- Most investors assume that no trend will last forever, but it can be absurdly difficult to forecast how or when these trends will change. It’s possible that July 2024 will be viewed as such a shift where small-cap stocks suddenly shift to outperforming large-cap stocks or value-oriented stocks shift to outperforming growth-oriented stocks. Even if we don’t know for sure that trends will change, we do tend to see higher levels of volatility as investors search for the next source of market leadership.

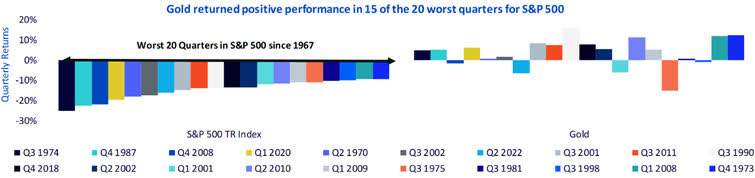

Figure 8 looks at the worst 20 quarters for the S&P 500 Index, in terms of returns, going back to 1967. Within an analysis like this, the known factor is that the S&P 500 Index quarterly return was bad, but the question being asked is-what did the gold price do during that same time?

If the gold price tended to rise during these difficult U.S. equity periods, gold could indicate a case for at least historical diversification. Interestingly, looking at figure 8, we see five quarters when the gold price was also negative, meaning there were 15 quarters when, while the S&P 500 Index was negative, the gold price appreciated.

Figure 8: Gold Delivered Positive Performance in 15 of the 20 Worst Quarters for the S&P 500 Index

Sources: WisdomTree, Bloomberg. Returns are measured in U.S. dollars, 12/31/1967-6/30/2024, using quarterly data. Gold is represented by the LBMA Gold Price PM Index, and the S&P 500 Index is measured on a total return basis. Past performance is not indicative of future results. You cannot invest directly in an index.

Conclusion

In our view, gold can serve a variety of purposes in a portfolio. However, where an investor chooses to fund this position from can sometimes lead to unintended consequences. By combining these positions via a capital efficient strategy like GDE, investors can maintain exposure to core assets while at the same time gaining exposure to diversifying hedges. In the event that USD begins to depreciate broadly, we believe exposure to gold may be poised to benefit, leading to better outcomes for investors.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Christopher Gannatti, CFA, Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Bradley Krom, U.S. Head of Research

Bradley Krom joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.

Original Post

Read the full article here

")

")

")

")

Q4 2024 Earnings Call Transcript")