")

Q4 2024 Earnings Call Transcript")

")

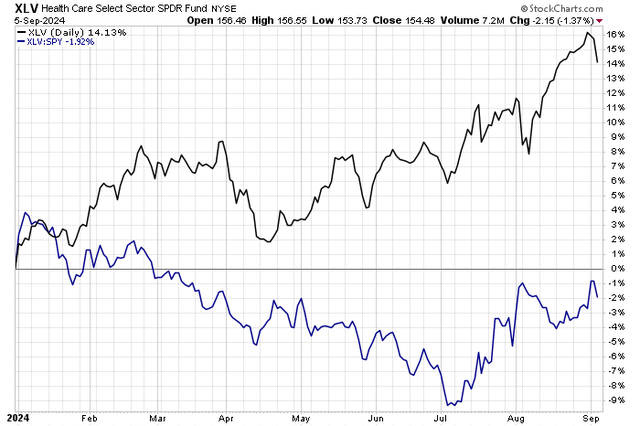

Bristol-Myers Squibb Company (NYSE:BMY) produced its best bottom-line beat in more than five years back in July. Shares rose significantly after reporting, helping the broader Health Care Select Sector SPDR ETF (XLV) sector begin a period of outperformance against the S&P 500 ETF (SPY). It’s almost always a favorable setup when we see a gangbuster company earnings update, just as sector relative strength turns for the better.

Not surprisingly, BMY shares are up more than 20% since the springtime, back when I initiated coverage on the stock with a buy rating. I remain concerned about the long-term EPS trajectory, but following the top and bottom-line beats and a full-year EPS increase from the management team, I see the valuation as higher today. Hence, I reiterate a buy rating.

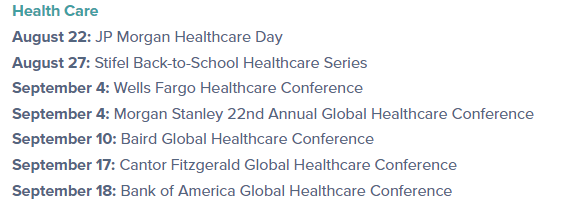

Moreover, the technical picture looks much better – I’ll note why that’s the case later in the article. Investors should also be on guard for industry updates from a slew of conferences in the next few weeks.

Health Care Stocks With Strong Second-Half Momentum

Stockcharts.com

Q3 Health Care Conference Schedule

Wall Street Horizon

Let’s shed light on BMY’s Q2 results and why shares surged 11.4% in the session that followed (the best post-earnings move going back at least three years, according to data from Option Research & Technology Services, ‘ORATS’). The company produced Q2 non-GAAP EPS of $2.07, a strong $0.44 beat relative to Wall Street’s expectations.

Revenue was also impressive at $12.2 billion, a 9% increase from year-ago levels. Backing out adverse foreign currency moves, the sales jump would have been 11%, thanks to strong sales from its Growth Portfolio and blockbuster drugs like Opdivo and Eliquis. Strength was seen particularly in the US market with a 13% revenue jump, while international revenues declined by 1% due to the FX impact and weakness in Revlimid.

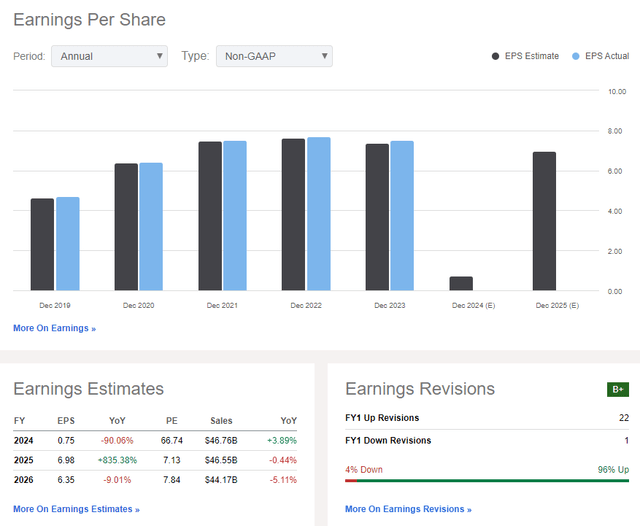

The management team also raised its FY 2024 EPS guidance to be in the range of $0.60 to $0.90 while announcing positive results from Phase 3 trials of cendakimab, an experimental therapy for eosinophilic esophagitis.

With strong sales and earnings, and a one-off impairment charge now in the rearview mirror, the trajectory heading into 2025 appears sanguine, though there is still the risk of some patents rolling off due to the loss of exclusivities from the Inflation Reduction Act. Slower worldwide sales amid macroeconomic weakness and increased competition from other pharma companies are other risks to weigh heading into the new year. Another unknown is what comes about after the general election with respect to capped drug prices.

On valuation, operating EPS is expected to rise close to $7 in the out year before declining back into the mid-$6s by 2026. But with favorable guidance provided by BMY in July and a more bullish turn among the sellside, I would not be surprised to see earnings upgrades get stretched out looking several quarters ahead while revenue expectations continue to hover in the mid-$40-billion range through the next two years.

BMY’s trailing 12-month free cash flow yield is now up to 12.9%, a very high figure, which could result in dividend increases in the periods to come. The current dividend yield is already high at 4.8%.

BMY: Sales, Earnings, Revisions

Seeking Alpha

On earnings, If we assume normalized EPS of $6.90 over the next 12 months, a slight increase from my previous forecast given the very robust Q2 report, and apply an 11 multiple (below the 5-year average of 14.7x), also a turn higher compared to my Q2 analysis, then shares should be near $76, resulting in still-undervalued stock despite the 20%-plus rally in the last handful of months. A concern is a lofty price-to-book ratio, but earnings strength should support the valuation.

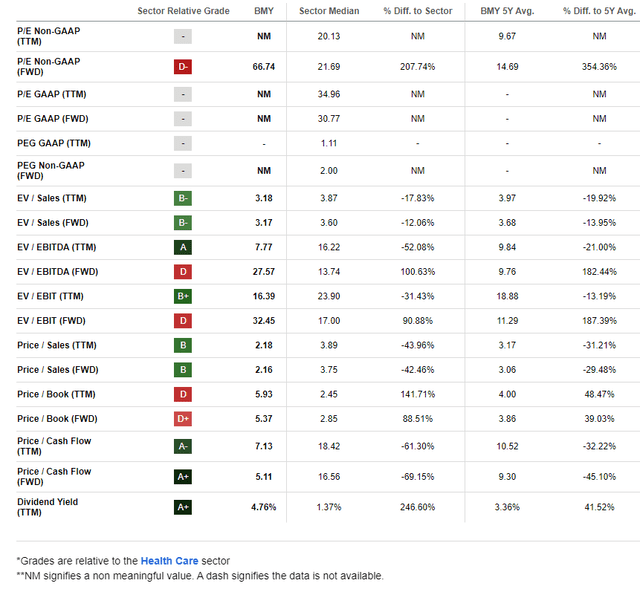

BMY: Compelling Valuation Metrics, High Free Cash Flow

Seeking Alpha

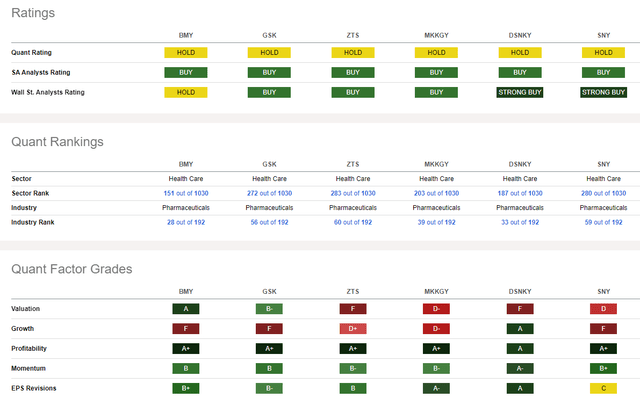

Compared to its peers, BMY sports among the best valuation ratings you’ll come across in the Pharmaceuticals industry, while the $101 billion market cap firm has a better forward growth outlook compared to its historical trajectory. Profitability metrics remain quite favorable, while Wall Street analysts are coming around to the reality of better earnings clarity in the quarters ahead.

Finally, and this is a key difference from what was seen during much of the first half of the year, share-price momentum appears much better today – a B+ Factor Grade from Seeking Alpha’s quantitative system compared to an F rating just three months ago. I’ll highlight key price levels on the chart to monitor heading into the end of 2024 later in the article.

Competitor Analysis

Seeking Alpha

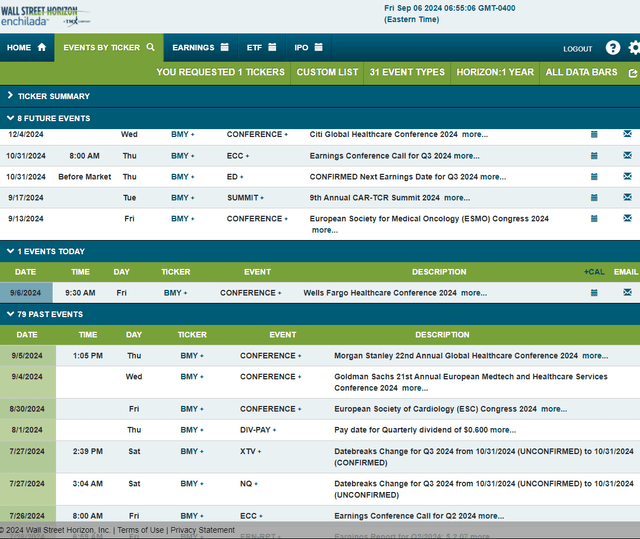

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2024 earnings date of Thursday, October 31, before market open. Before that, BMY’s management team is expected to present at the European Society for Medical Oncology Congress 2024 event next week and the 9th Annual CAR-TCR Summit 2024 during the middle of the month, which could draw volatility.

Corporate Event Risk Calendar

Wall Street Horizon

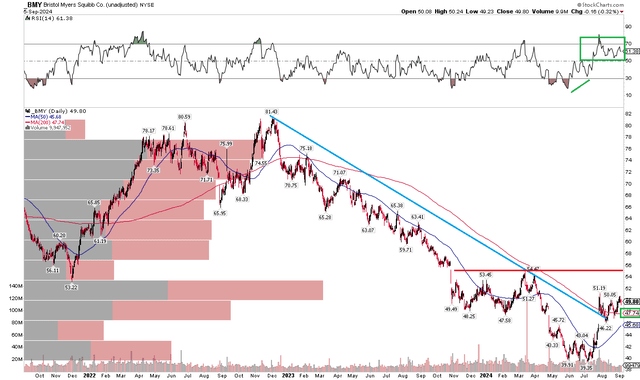

The Technical Take

With a valuation boost after the breakout Q2 profit report, BMY’s technical chart has made key positive moves too. Notice in the graph below that shares broke out from a downtrend resistance line after the July earnings update. While upside resistance remains in play between $52 and $54, the long-term 200-day moving average is now flat in its slope after trending lower since the start of last year. What’s more, the RSI momentum oscillator at the top of the chart is now ranging in a bullish zone between 50 and 80, suggesting that the bulls control the trend.

Also take a look at the shorter-term 50-day moving average – it is poised to cross above the 200dma in what would be a bullish golden cross event. But with a still high amount of volume by price up to the mid-$50s, the onus remains on the bulls to carry BMY through long-term resistance. On the downside, support is now between $46 and $48.

Overall, the technical and momentum situation appears more favorable today.

BMY: Shares Breakout, Watching Mid-$50s Resistance, Improve RSI Momentum

Stockcharts.com

The Bottom Line

I have a buy rating on BMY. Strong Q2 results, a guidance raise, and a better situation on the chart warrant a continued optimistic view and price target increase.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")

")