")

Q4 2024 Earnings Call Transcript")

")

")

Investment action

I recommended a hold rating for Korn Ferry (NYSE:KFY) when I wrote about it in June, as I no longer think the business will see a growth recovery in FY25 given the prevailing interest rate situation and management guidance. Based on my current outlook and analysis, I recommend a hold rating. Although 1Q25 results had several positives, I am not certain that a growth recovery will happen in the coming months given the macro uncertainties ahead. Moreover, valuation multiples have already improved to a historical average, reflecting the market’s optimism in a recovery next year. If the macro situation doesn’t get better, we could see multiples inflect downwards.

Review

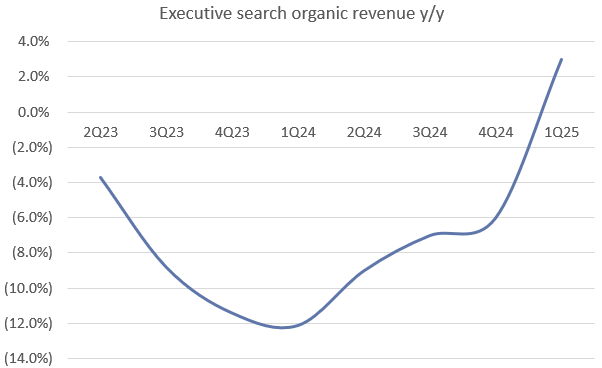

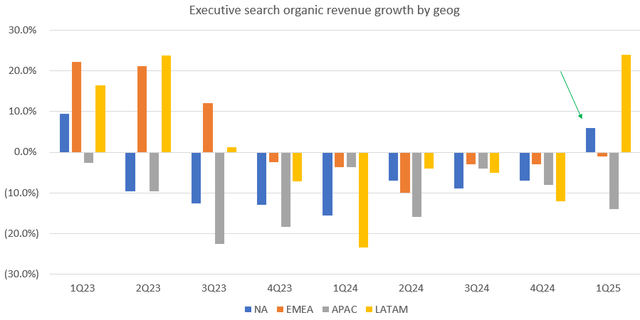

KFY reported 1Q25 fee revenue of $674.9 million, representing a decline of 3.5% y/y (this is better than consensus expectation for 5.1% decline). Growth on a constant currency basis came in better at -2%. By segment, on an organic growth basis, revenue in executive search grew 3%, revenue in consulting grew 1%, digital grew 2%, RPO (recruitment process outsourcing) declined 7%, and professional search and interim declined 14%. Despite the revenue decline, KFY profit margins surprised on the upside, with EBITDA margins expanding by 280 bps y/y to 16.5%, driven by cost management and productivity gains, resulting in EPS of $1.18 that outperformed consensus of $1.12.

Author’s work Author’s work

I believe KFY’s 1Q25 results are a mix bag of positives and negatives. Starting with the positives, I think the most positive message is that KFY is seeing stabilizing labor market trends. This is especially for executive search that was down for the past 7 quarters, driven by KFY’s largest market—North America—that saw growth of 6% due to recruiter productivity gains and demographic tailwinds, potentially signifying the start of a recovery cycle. Management guided 2Q25 revenue to be flat sequentially for this segment, indicating the positive trend has continued into the quarter. Given that management already has 5 weeks of 2Q25 data, I’d say this guidance has a lot of merits.

This quarter also amplified the impacts of KFY’s diversified revenue streams in consulting and digital solutions. Both continued to show positive growth despite the macro backdrop, and while consulting revenue decelerated from 5% to 1%, I don’t see this as a sign of major weakness. Sales are simply deferred due to an elongated sales cycle for smaller clients that are waiting to make decisions after the election. Importantly, KFY saw 10% y/y growth in consultant productivity and 8% growth in consulting bill rates, which suggests that KFY is winning larger deals—a very positive early sign of a recovery cycle as large corporations typically start investing first in a turnaround cycle.

The last positive takeaway was that cross-line-of-business referrals now represent 27% of fee revenue, up 100 bps from 26% in FY24. Notably, large marquee and regional accounts continue to be the areas that see the most cross-referrals (now representing ~ 37% of revenue), and that marquee account purchases at least three offerings. Financially, this tells me that KFY growth potential has turned structurally better as it has demonstrated this strategy enhances its distribution capabilities and at a lower cost.

The negative aspect that is holding me back from turning bullish is that RPO, professional search, and interim y/y growth are still negative. This places doubt on whether we have gone past the trough of this cycle. Moreover, quarterly new business ex RPO declined 2% y/y on a constant currency basis. While this is in line with 4Q24, showing stabilization, it does not indicate a recovery trend. In addition, just two days ago, it was reported that the number of US job openings fell to the lowest level since 2021, which makes me even more worried that there might be another leg of negative growth before we see the trough of this cycle. Comments from peers also suggest that we have yet to enter a growth cycle (refer below). Lastly, it was also disappointing to learn that management is not executing well on integrating its legacy digital assets from prior acquisitions into a single tech platform. This caused management to delay their timeline of achieving revenue growth of 10 to 15% y/y growth for the digital segment.

So yeah, a good start, early days, but a good start. But I think, you know, we will clearly need some macro improvement to get on track to deliver against the objective that we set out on the Capital Markets Day. Pagegroup 1H24 call

In Q3, we expect the macroeconomic environment to remain challenging, so we’re increasing our focus on reducing indirect costs to ensure we can afford sufficient field capacity, as well as strategic investments in talent engagement, delivery excellence, and technology. Randstad NV 2Q24 call

Valuation

In terms of valuation, KFY has traded up to ~14x forward PE, the historical average over the past 10 years. Looking at how the multiples have moved in recent months, I think the market is pricing in a recovery in the coming months (consensus has FY26 EPS growth of 11% and revenue growth of 6%). Although I see merits to this optimism given the potential fed rate cut and slowing inflation, I don’t think it is certain enough today to say that a recovery will happen. For instance, depending on how the US election plays out, we could see a sharp increase in inflation, which may lead to another round of rate increases. Also, we don’t know for sure if the Fed will cut rates. If we make the assumption that these uncertainties turn out negatively, the equity story for KFY could be heavily impacted, which may cause multiples to revert back to ~10x (previous low in 2022).

Final thoughts

My recommendation is a hold. While the results showed some positive signs, including stabilizing labor market trends and improved consultant productivity, the ongoing macroeconomic uncertainties continue to hold me back from turning bullish. In particular, the potential for further economic downturns and the uncertain impact of the upcoming election. Hence, I think it is safer to maintain a hold rating until there is more concrete evidence of a growth recovery.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")

")