")

")

Q1 2025 Earnings Call Transcript")

(NASDAQ:MU)")

")

The Chinese air travel market will see significant growth in the years and decades ahead. That might capture the interest of investors to be invested in those airlines. In this report I will discuss the risks and opportunities and provide a stock price target and rating. Since there are various ways to own Air China (OTCPK:AIRYY) stock, I will also discuss what options there are to buy Air China stock.

Air China Is Loss Making But With Strength On Unit Level

Air China

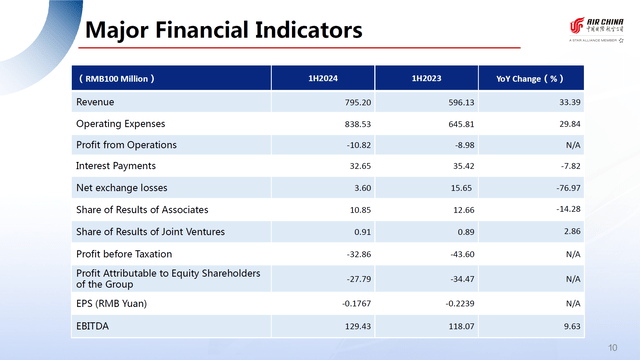

In the first half of 2024, revenues grew 33.39%. This was driven by 31.9% growth in passenger revenues and cargo and mail revenues grew 136%. Domestic passenger revenues grew 15.1% accounting for nearly 75% of the passenger revenues while international passenger revenues grew 146% and 44.6% growth in regional passenger revenues. Passenger capacity grew 33.4% while total airline capacity grew 37.65%. So, overall we see strength in the unit revenues for passenger traffic. Operating expenses climbed 29.8% driven by higher jet fuel costs which accounted for nearly a third of the costs. Take off and landing fees, catering, aircraft maintenance and SGA all showed costs in excess of capacity expansion. Costs excluding fuel decreased by 20% driven by higher fuel consumption and higher fuel prices. Unit costs declined by 2.6% while unit costs excluding fuel declined by 6%.

So, from unit revenue and unit cost perspective, we saw good development. However, the company remains loss-making on operational profit level. On EBITDA level, we saw profits increase 9.6%

What Are The Risks And Opportunities For Air China?

The long-term increase in demand for air travel in China provides significant opportunities for Air China. What should be kept in mind, however, is that the airline is primarily state-owned. State-owned entities own most of the Chinese airlines, which in some way is a good thing, as it makes entering the domestic market for private airlines very challenging. At the same time, I do believe it brings a pressure as the airlines are not necessarily focused on generating a profit but more about being connectors for the Chinese economy.

Another potential pressure could be any weakening in unit revenues as observed in major parts of the world, which could lead to earnings growth on EBITDA level evaporating. It is not the case that none of the Chinese airlines are generating, but as Nikkei reported it are the private airlines that generate profits while the primarily state-owned airlines are still loss making.

Air China Stock Offers Opportunities

The Aerospace Forum

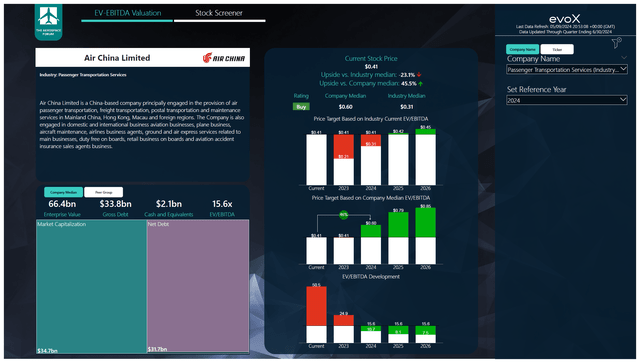

To determine multi-year price targets The Aerospace Forum has developed a stock screener which uses a combination of analyst consensus on EBITDA, cash flows and the most recent balance sheet data. Each quarter, we revisit those assumptions and the stock price targets accordingly. In a separate blog I have detailed our analysis methodology.

Air China is certainly not a name without risk given the yield pressure, but I do believe that as the company increases utilization on its aircraft and demand for air travel continues growing. Analysts are expecting EBITDA to grow at a 75% rate between 2023 and 2024 driven by the acquisition of a controlling stake in Shandong Airline and free cash flow growth of 2%. That would indicate a $0.60 price target, representing 46% upside.

If you are interested in purchasing shares, there are two OTC tickers, namely AICAF which represents one ordinary and AIRYY representing 20 ordinary shares. However, both of these tickers lack volume, which could make buying and selling at desired prices and quantities a challenge. Therefore, the Class H shares listed in Hong Kong under the ticker 753 with several millions of pieces traded might be a better option.

Conclusion: Air China Is Worth A Shot

I believe that Air China has upside. However, it should be noted that since the company is owned for over 50% by Chinese state entities, the focus might not always be on generating profits and more on having Air China function as a connector in service of the Chinese economy. If investors, feel comfortable with that I believe that the stock is a buy as its significantly undervalued against its historical median valuations.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

Q1 2025 Earnings Call Transcript")

(NASDAQ:MU)")

")