")

")

")

Q1 2025 Earnings Call Transcript")

Aker ASA (OTCPK:AKAAF) (ISIN:NO0010234552 for the OSE listing) continues to trade significantly below NAV, which has been the basis of our coverage for a while now, which is not reasonable as the portfolio elements accrete. Aker Carbon Capture has been merged with Schlumberger (SLB), which was maybe the weakest asset in the portfolio, and what remains on the industrial side are solid businesses. While some trading down can be attributed to pressures on oil, which affect Aker ASA’s largest holding of Aker BP (OTCQX:AKRBF), we do see a possible catalyst as early as 2025 of the IPO of Cognite which will launch into markets that at the moment still rate AI-related stocks as its ARR and cash flow profile continuously improve. Aker ASA remains a buy, although the pressures from oil cannot be denied as supply cuts phase out and speculation around industrial conditions in the US mounts.

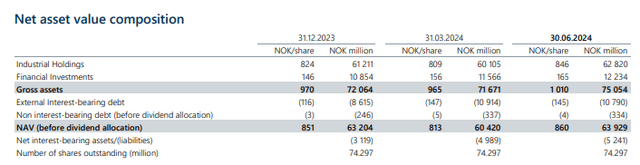

Aker ASA NAV

NAV (Q2 PR)

Usually, we run our own NAV calculations due to the mark-to-market effects, but even with quite conservative assumptions the values are quite close to each other as the stocks composing the portfolio haven’t moved too much since the end of June, and where they have moved they’ve been offset by other stock movements. The provided NAV figure is above, and it is relatively updated.

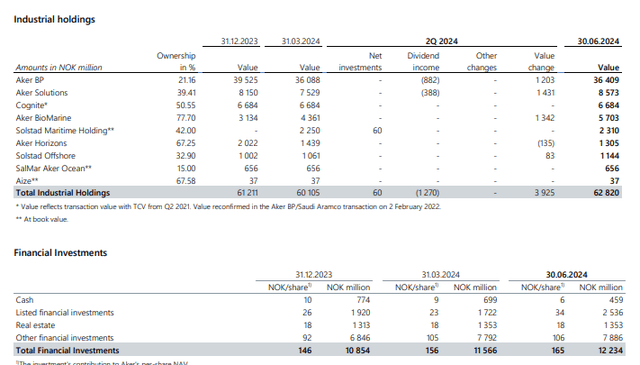

Elaborated Gross Assets (Q2 PR)

Cognite continues to be valued according to a 2021 precedent, which is concerning because that was before costs of capital rose. On the other hand, AI is hyped right now, so valuations like that might still stand. Moreover, the business has progressed significantly and being backed by Aker ASA doesn’t really have any reflexivity risks associated with financing – although it is anyway approaching cash flow positivity.

Headline revenues for Cognite are up around 10%, but ARR, reflecting the annualised subscriptions for its industrial AI and digital twin product, are up 42% YoY in the current quarter, and monthly active users have doubled. Negative EBITDA margins are shrinking from -15.4% to -13.3%. Cognite is 10% of the NAV picture for the company. Continued growth coupled with IPO prospects as soon as the business becomes more sustainable, possibly in 2025, on the US markets could seriously increase the fair value of the holding as it taps primary markets once again in a frothy environment for AI. Current given values for Cognite are around 6x Price/annualised Sales. While you might think it’s wild, median multiples for AI companies are in excess of 20x P/S right now. Moreover, Cognite’s ARR is growing quickly, with sales always lagging ARR figures due to revenue recognition, so the annualised sales figures understates things.

Aker BioMarine is performing well. They’ve made a partial disposal of their krill-based feed business which we always liked and thought was highly valuable, confirmed by this transaction, and the stock has almost tripled since about this time last year. They are also announcing an extraordinary dividend associated with the disposal.

Aker Solutions (OTCPK:AKRTF) backlog is large and profits are large. Except for in some rare cases where oil and gas EPC projects were quoted and assessed poorly, all players in this segment are seeing significant mounting of backlogs and projects. Despite the retreat in oil prices, levels are still far above breakeven and therefore the strategic interest in developing oil assets trumps all.

For Aker BP, which is a straightforward Norwegian Continental Shelf E&P play, they are seeing some natural volume declines that will be eventually offset. However, there are concerns over the price of oil. Supply cuts are being phased out by OPEC+, and those were saving oil from price pressure due to weak Chinese and EU industrial activity levels. The US is now a concern as well, although to a lesser degree. There are signs that things are decelerating industrially, which of course concerns end market demand for oil.

Bottom Line

We aren’t necessarily betting on Aker ASA’s IPO of Cognite bumping value significantly.

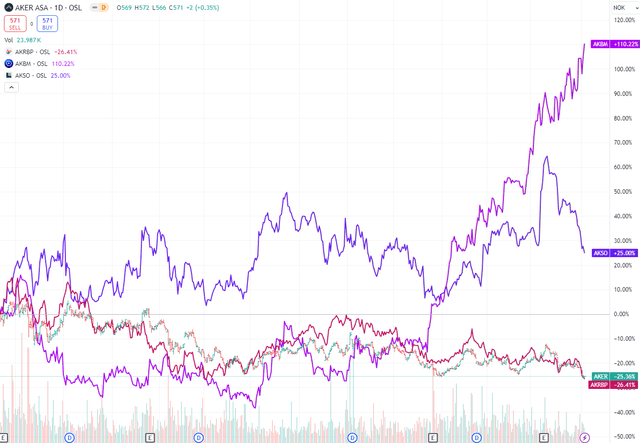

Relative price performance (Tradingview.com)

But what we are noticing is that Aker BP and Aker ASA’s price changes since two years ago are very close to one another. This cannot be explained well as the other components of the Aker ASA portfolio were performing very well. The defensiveness of the Aker ASA portfolio should have been more obvious than trading in line with Aker BP, which is only around 50% of NAV.

In general, we find that Aker ASA’s quality is ignored. They have strong assets, and not everything is tied to the oil commodity either. We find them the better way to approach Aker BP, as well as a more compelling overall play. The NAV discount is at around 35%. That is significant.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

Q1 2025 Earnings Call Transcript")

(NASDAQ:MU)")