")

Stock: Let Your Winners Run")

Thesis Recap

I covered Banco BBVA Argentina (NYSE:BBAR) in April 2024, with the thesis that Argentina’s improving economy and inflation trends would push Argentinian bank stocks up even further. Since then, the stock has given investors a total return of 57%, and yet I still think there is more upside today. From a bottom-up perspective, BBVA Argentina’s earnings still trade at a low multiple, leading me to reiterate my buy rating with an updated price target of $14. Put simply, I expect a combination of multiple expansion and earnings growth to keep pushing the stock price higher.

Earnings Can Keep Growing

The company reported Q2 earnings with the following results:

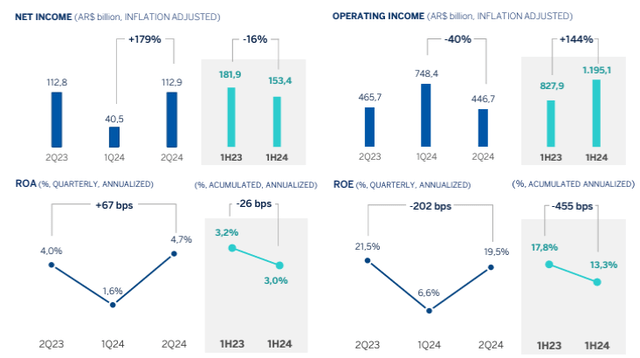

BBVA Argentina’s inflation-adjusted net income in 2Q24 was $112.9 billion, 178.8% above the $40.5 billion reported in the first quarter of 2024, and 0.1% above than the $112.803 billion reported in the second quarter of 2023.

In 2Q24, BBVA Argentina posted an inflation-adjusted average return on assets of 4.7% and an inflation-adjusted average return on equity of 19.5%.

As of 2Q24, the non-performing loan ratio reached 1.18%, with a 165.50% coverage ratio.

Investors can see that net income continues to perform well alongside an improving inflationary environment. Management explains that falling inflation has led to subsequent interest rate cuts, which has led to lower net income for the first half of 2024 compared to 2023. Nonetheless, I think that the long-term outlook is still very positive and that changes in rates, inflation, and consumer behavior will sustain strong returns on capital for BBVA Argentina.

Investor Presentation

One of the benefits of declining inflation in Argentina has been the improvement in the efficiency ratio for BBVA Argentina. For Q2 of 2024, the efficiency ratio reached 55.3% according to the investor presentation, down around 10% QoQ. I expect this trend to continue as Milei implements further austerity cuts, stabilizing the currency from further devaluations. Thus, earnings have more room to run up as BBVA Argentina adjusts their operation to fit a more deregulated, free-market economy.

Allowances for loan losses increased 30.4% in the second quarter, as management cites “a genuine growth in loan portfolio” necessitating these risk management measures. This reserve for bad debts is part of the reason operating income decreased by 40% QoQ, which in my opinion is a good thing as management has shown to be prudent and cautious in managing their risk. NPL coverage ratios continue to be very high at 165%, which is lower than before but still high enough to cover future potential losses.

In conclusion, scanning the fundamental KPIs of this bank reveals that it’s mostly business as usual. The tailwinds behind most of Argentina’s banks continue to drive resilient earnings, and returns on equity still stay well into the double digits. There’s always a bit of noise from quarter to quarter, so the ups and downs of NIM, interest and non-interest income, and profitability can sometimes be noisy. However, I think the long-term picture is still very much intact and investors should take a long-term view based on the regulatory improvements Milei is making for his economy.

It All Comes Down To The Consumer

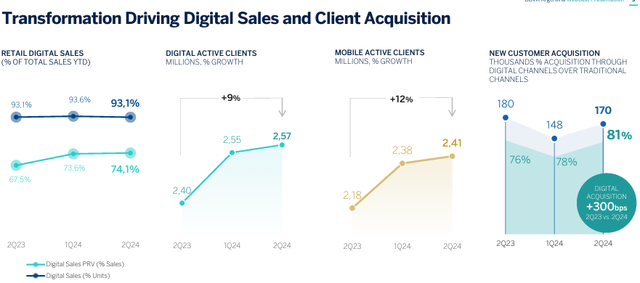

In my opinion, the retail crowd continues to be one of the core driving factors for net interest income growth for many banks in Argentina. In BBVA Argentina’s case, I see their digital investments paying off as the percentage of retail digital sales, digital active clients, and new customer acquisition continues to grow the bank’s reputation and credibility as a trustworthy deposit taker. Also, their loan portfolio is growing rapidly, as “BBVA Argentina managed to increase the retail, commercial and total loan portfolio by 41.1%, 50.1%, and 45.8%, respectively during the quarter, surpassing quarterly inflation levels in all cases” according to the transcript.

Investor Presentation

I think the individual consumer is ultimately the backbone of any economy, and their success translates into an economy’s success. The more money people can earn, the more they can deposit, invest, and credibly borrow, all of which is bullish for the fundamentals of Argentinian banks. I’m happy to note in the press release, “In the quarter, the variation was driven by an overall growth in all lines, especially in credit cards by 15.3%, in consumer loans by 45.3% and in discounted instruments by 30.1%”.

Deposits continue to do well, increasing 2.6% quarter over quarter. Management explains in the transcript:

The quarterly change is mainly affected by a 36% increase in time deposits, a 21% increase in saving accounts offset by a 19% fall in checking accounts, especially non-interest bearing checking accounts.

I can see that consumer confidence in Argentina is improving based on these numbers, as they are more willing to put money in the bank and leave it there in interest-earning time deposits. Increasing consumer confidence is another bullish factor for banks and the economy, as it can stimulate economic and borrowing activity. A lot of what dictates consumer behavior is their expectations, and based on these numbers, it’s obvious to me that the consumer has gotten more confident and optimistic. Thus, I think Argentina’s banks should continue to rally off of a stronger, more optimistic consumer.

Privatization Is Good For Argentina

Milei, a free-market economist, believes in limited government intervention and thus has built up a private sector in Argentina’s economy. His economic reforms have led to the privatization of state-owned assets, which in my view is a positive for banks like BBVA Argentina. Investors can already see that BBVA Argentina has more confidence in lending to the private sector, where there is no moral hazard and the free market can dictate where capital ends up. In the press release and earnings transcript, management says:

As of June 2024, private credit in pesos for the system grew 176% YoY, while BBVA Argentina increased its private loan portfolio in pesos by 230%.

In terms of activity on Slide 6. Private sector loans as of the second quarter of 2024 totaled ARS3.9 trillion increasing 23.1% in real terms. Loans to the private sector in pesos increased 24.2% in the second quarter of 2024.

By privatizing these companies, I believe that banks have more confidence and incentive to pour investment and provide credit to these organizations. Thus, they can actually deploy capital at attractive rates of return, as we are seeing now in the recent quarter. Reduction in government interference can allow these institutions to run themselves more efficiently, improving their financial creditworthiness and stability. Therefore, I believe that the private sector is another growth opportunity for banks like BBVA Argentina, and we are already seeing evidence of loans pouring in to this area. I continue to believe privatization to be a major positive both for Argentina’s economy and their banks.

Valuation – $14 Fair Value

I reiterate upside for BBVA Argentina based on their earnings estimates from Seeking Alpha. I believe a Forward P/E of 3-4x is way too low, and that earnings growth combined with multiple expansion can realize significant upside for investors.

Seeking Alpha

For the sake of conservatism, I will assume that EPS results come in at around $1.50, which is half of the estimates made by analysts. If we assume revenues stay at around $2.5 billion annually, and an average profit margin of 15% which is around the sector median, earnings can come in at $375 million a year. Divide by shares outstanding of 204 million gets me EPS of $1.5, rounded down for conservatism.

Multiplying EPS of $1.50 by a P/E multiple of 9, below the sector median of 12x, gets me around $14 per share, rounded up. Therefore, I see more upside in the stock and reaffirm my bull thesis. The main takeaway is that investors may expect to see a double-play, where the earnings grow and the multiple continues to re-rate higher.

Risks

Argentina continues to be in recovery mode, but this recovery may not last and could even potentially reverse. Shock therapy doesn’t lead to a straight line-up in terms of economic recovery, and it still may take a while for GDP, foreign investments, and inflation to stabilize into normalcy. Investing in Argentina also means taking on currency risk, as the earnings are earned in Argentinian Peso.

Political instability and opposition to Milei’s reforms may reverse what he’s done, which in my opinion would revert Argentina back to a poor economic condition. Some critics will argue that Milei’s policies only benefit the rich, and make life worse for the poor. Furthermore, unemployment and poverty continue to be pretty bad in Argentina, at 7.7% and 57%.

The multiple may never expand like I expect it to, leading to a stagnant or flatlining stock price. Investors may continue to remain skeptical and shun Argentina as a viable investment place, which would affect the earnings multiple the stock could achieve. So, the double-play may actually end up being a single, with earnings growth lacking a re-rating in the P/E multiple.

Buy BBVA Argentina

I like Argentina’s economic recovery story, and applaud Milei’s economic reforms. The major beneficiaries of this trend are the banks, and BBVA Argentina among others is likely to benefit from this trend. With reasonable earnings, privatizations, and a stronger Argentinian consumer, I believe it all spells a buy rating for BBVA Argentina.

Read the full article here

")

")

")

")