")

")

")

Overview

I’ve grown to appreciate high-quality credit funds that have the power to provide total returns that are comprised of both income and some capital appreciation. I’ve come across FS Credit Opportunities (NYSE:FSCO) and I believe that this has this structure in place to be a solid choice to get some credit exposure. FSCO operates as a closed end fund that invests in a diversified portfolio of different credit instruments such as senior secured loans and high-yielding bonds. These types of funds typically involve a bit more risk because of the varied credit quality within holdings, which can make these funds more vulnerable to fluctuations in interest rates.

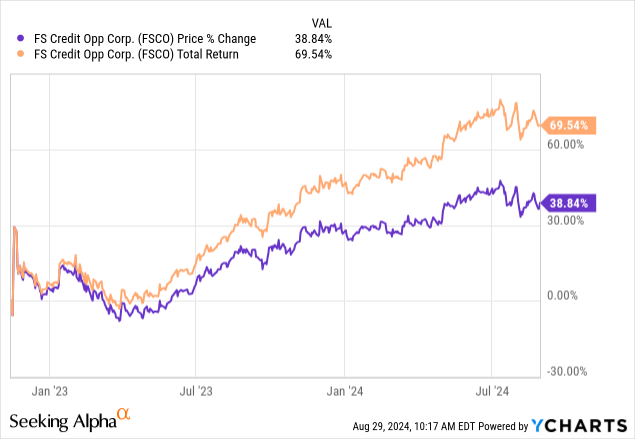

FSCO has a very recent inception, dating back to November of 2022. The fund’s advisor is FS Global Advisor and according to the most recent prospectus, the management see sits at 1.5% of average gross assets. Despite this short history, the performance has been stellar. Price returns sit over 38% while the total return including distributions is approaching 70%. This is helped by the large dividend yield of about 11.7%. While I do maintain a portfolio of traditional dividend growth stocks, I find that high-yielding credit focused funds such as FSCO are a great addition as they can still provide massive income growth over time.

Since the fund is still relatively new, it can be hard to get a sense of how attractive the current valuation is. However, I believe that the portfolio of investments within FSCO will greatly benefit from future interest rate cuts. Lower rates would provide both relief for current portfolio companies within, as well as create more ideal conditions for growth of FSCO’s portfolio. FSCO has survived all of 2023 and 2024 so far while operating with interest rates sitting at their decade high, which also helps instill some confidence that the fund will remain resilient over long-term market cycles. Let’s first review the portfolio of investments that makes FSCO attractive.

Portfolio Strategy & Financials

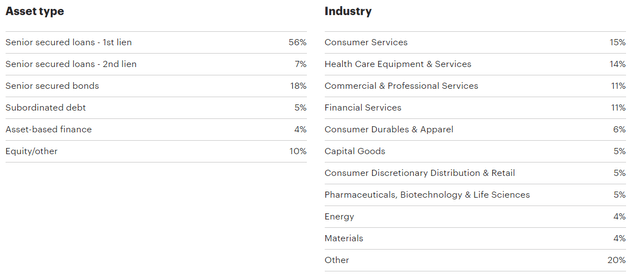

FSCO maintains a portfolio of diverse credit investments that span across many industries. The largest slice of industry exposure is to consumer services, which accounts for 15% of net assets. This is followed by exposure to health care equipment & services and commercial & professional services, which account for 14% and 11% respectively. It’s always nice to see a wide reach of exposure because it limits concentration risk to any one specific sector and increases the probability of the fund navigating sector headwinds.

FS Investments

Total assets amount to $2.15B, and this is spread across 82 different portfolio companies. What I like is that approximately 81% of their portfolio is structured on a senior secured basis. Senior secured debt sits at the top of the corporate capital structure and limits the amount of risk of these investments. Since this form of debt sits at the top of the capital structure, it has the absolute highest priority for repayment in cases where portfolio companies are going through a bankruptcy and liquidating assets. This reduces the probability of FSCO losing all invested capital in a bad deal.

What makes FSCO unique is that the portfolio of investments gives shareholders exposure to both public and private markets. Both of these have their own unique benefits that can contribute to growth. The private exposure encompasses the debt investments I previously mentioned, which allows investors to capitalize on the higher interest rate environment. Approximately 54% of their total portfolio is comprised of these floating rate investments.

Interest rates were aggressively hiked throughout 2022 and 2023 and now sit at their decade high. While this can create an unfavorable environment for borrowers, it’s a great environment for lenders that are able to rake in higher levels of income. In addition, the public exposure that FSCO provides allows the fund to benefit from more traditional things like earnings growth or acquisitions.

FSCO Presentation

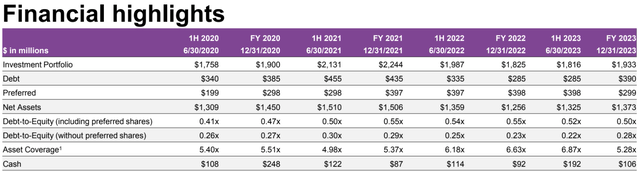

Looking at the fund’s financials reveals that the investment portfolio has grown since inception. At the close of 2020, the investment portfolio was valued at $1.9B and has grown to a total of $1.93B at the close of 2023. Net assets amount to $1.37B for the most recent year-end and is accompanied by a strong asset coverage ratio of 5.28x. We can see that FSCO has been able to generate a higher NII yield of 11.1% over the prior years because of the current higher interest rate environment.

At the fund’s launch, NAV per share sat at $6.56. This has since grown to a NAV of $6.92 per share. A growing NAV is a healthy indication that the fund generates enough earnings to support the distribution paid out to shareholders, while simultaneously retaining enough earnings to grow the fund over time. However, it should be noted that the majority of FSCO’s portfolio of investments has credit ratings that are considered below investment grade.

Valuation & Outlook

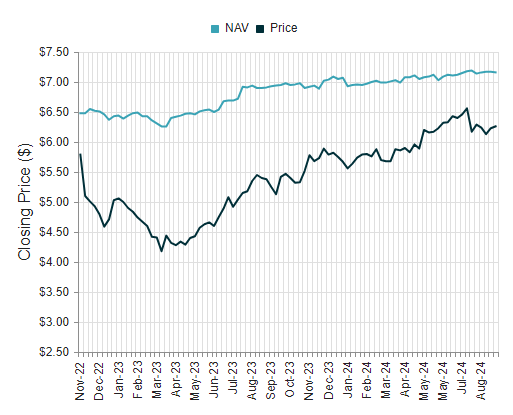

Since FSCO operates as a closed end fund, the price can vary from the actual value of the underlying assets. As a result, FSCO currently trades at a discount to NAV of nearly 14%. However, we can see that since the funds’ inception, the discount window has been slowly creeping back up towards the fair value range due to the strong performance. I consider fair value the cross point where the price trades at neither a discount nor premium to NAV. As previously mentioned, NAV has been steadily growing since inception and this has been supported by large earnings growth. Earnings per share ended 2020 at $0.35 per share and has since increased to $1.23 per share at the end of 2023.

CEF Connect

I believe that interest rate cuts will further decrease the discount level as the NAV continues to grow. Interest rate cuts are a positive catalyst because they will provide relief to current borrowers within FSCO’s portfolio, while simultaneously making conditions more attractive for potential new borrowers. I read through the most recent quarterly update and management has shared the following outlook:

The first quarter of 2024 was characterized by generally strong economic data and solid performance across the leveraged credit markets. However, we believe that financial markets remain susceptible to periods of volatility through the remainder of the year as investors continue to monitor geopolitical conflicts and wrestle with the forward path of the U.S. economy and the potential for Fed rate cuts in 2024 amid persistent inflationary pressures.

I tend to agree that the remainder of 2024 can see higher levels of volatility and uncertainty than usual. We still have the US Presidential elections upcoming by the end of 2024 and while investors await the results of that, I anticipate there to be elevated levels of buying and selling driven by the uncertainty. In addition, the Fed have confirmed that the time for interest rate cuts has come. There are some estimates for three rate cuts, but I take that likely since we’ve heard similar expectations of multiple rate cuts this year as well, which never actually happened.

When rate cuts do happen, this will create a more ideal environment for borrowers, as companies will now have access to debt at cheaper interest rates. Additionally, it will make it less expensive to hold debt on the balance sheet as the required interest payment amounts decrease for floating rate loans. I anticipate this creating a higher volume of borrowers that FSCO can use to its advantage to continue growing NAV over time. If FSCO was able to consistently grow NAV in unfavorable conditions, the growth should be compounded in better environments.

FSCO Presentation

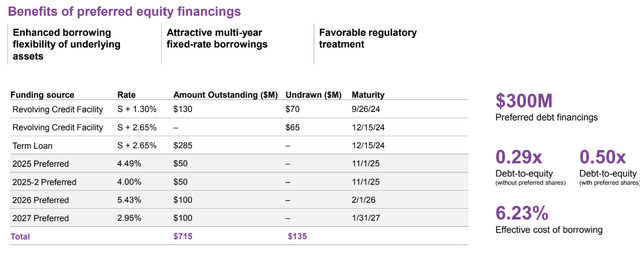

Lastly, lower interest rates should also help FSCO grow more efficiently because it will reduce the cost of their debt. FSCO currently holds $715M in debt outstanding, which is comprised of revolving credit facility and term loans. This debt sits at an effective cost of borrowing of 6.23% and if the cost of borrowing gets reduced, this allows for a greater margin of earnings to be retained since less would need to be allocated towards repayment of these debts.

Risk Profile

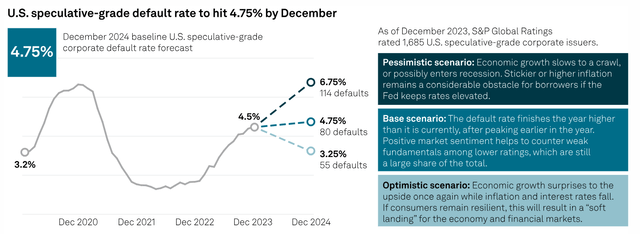

It should be clearly understood that the risk of an investment in FSCO is that the portfolio of investments is in assets that have poor credit quality ratings. FSCO invests in growing a portfolio of debt instruments that are rated below investment grade, which typically have a rating of BB and lower. This means that the portfolio companies may not have the most well-secured balance sheet that is capable of navigating prolonged headwinds. While higher interest rates can generate more income for FSCO, it can also increase the rate at which these portfolio companies default on their loans.

As interest rates remain elevated, so does the interest payments that these borrowers have to pay in order to service that debt. As a result, these higher costs can chew into operating margins and limit profitability. Therefore, it’s been quite common to see default spike during times when interest rates are high and default decrease when interest rates are low. According to forecasts compiled by S&P Global, the speculative grade default rate is estimated to average a base case rate of 4.75%. However, we can see that throughout 2021, the estimated default rate decreased as rates sat near zero levels.

S&P Global

I typically like to refer to the amount of poorly rated companies as the non-accrual status. This represents the amount of portfolio companies that are significantly underperforming original expectations and can no longer keep up with the required debt payments. Borrowers that get put on non-accruals status have failed to pay the required payments on that debt and are no longer generating any earnings growth for FSCO.

On the last earnings call, management confirmed that the non-accruals sat at 3% of the portfolio. The way I see it, FSCO has done a great job at minimizing the non-accrual rate, as their portfolio is currently performing better than some business development companies. Just for comparison, here are some of the popular BDCs and their respective non-accrual rates:

- FS KKR Capital (FSK): 4.3% non-accrual rate at cost and 1.8% of portfolio at fair value.

- Hercules Capital (HTGC): 2.5% non-accrual rate at cost and 0.9% of portfolio at fair value.

- PennantPark Investment (PNNT): 4.2% non-accrual rate at cost and 2.5% of portfolio at fair value.

Dividend

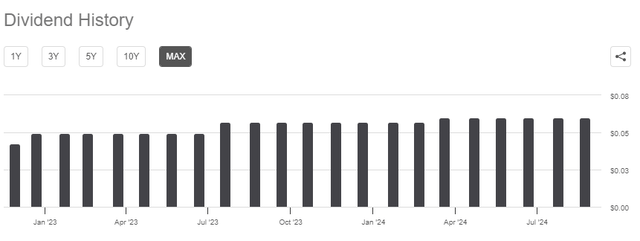

As of the latest declared monthly dividend of $0.06 per share, the current dividend yield sits at 11.7% If the net investment income earned by FSCO remains the same, the distribution has a comfortable rate of coverage. Based on the last full-year net investment income amount of $0.77 per share, we get a coverage rate of approximately 107%. We can determine this by multiplying the monthly distribution rate by twelve to get the annual payout amount of $0.72 per share. Therefore, there are no concerns about a dividend reduction at the moment, but this could change with future interest rate cuts.

While it’s likely that interest rate cuts can drive long-term growth through a growing portfolio of investments, it can also have a negative short-term impact on the level of net investment income that’s generated by FSCO. Since the majority of FSCO’s portfolio operates on a floating rate basis, lower interest rates would directly translate to lower earnings generated. While the dividend is currently covered at a rate of 107%, a larger coverage cushion would instill a bit more confidence here. It ultimately depends on how well management can grow the fund and offset any negative impacts to net investment income over the year.

Seeking Alpha

Although the fund already has a double-digit dividend yield, it has been able to reward shareholders with a few raises over its short history. This was likely a result of higher interest rates and the debt investments pulling in higher amounts of income. I do not expect this frequency of distribution raises to increase over the next year, as I think the fund should remain a bit more conservative right now to preserve the current distribution. It will be interesting to see how rate cuts ultimately impact the net investment income and whether or not FSCO’s future performance can support the current rate. However, management seemed fairly confident in their ability to continue out earning the distribution rate on their last earnings call.

As has been the case since the FS Global Credit team assumed management of FSCO in January of 2018, net investment income fully covered distributions paid during the quarter. We believe our performance reflects the dynamic nature of our strategy investing across public and private credit with a focus on generating return premiums driven by the complexity of a company’s balance sheet, the illiquidity of an asset, unconventional ownership or corporate events.

Takeaway

In conclusion, FSCO is a solid fund that has been well managed as NAV continues to grow over time and the distribution is fully covered by net investment income. While I expect the dividend yield of 11.7% to remain solid, future raises may slow down due to the lower interest rates having a negative reaction on the higher levels of NII generated. The monthly nature of the distribution makes it highly desirable for income oriented investments that may be looking for their next source of reliable income.

While there are risks involved since FSCO invests in below investment grade debt, the pros continue to outweigh the cons at this moment. FSCO has impressed by providing a total return that is comprised of both income and capital appreciation. The fund remains highly diverse in nature and the focus on senior secured, floating rate debt instills a lot of confidence to hold FSCO for the long term. Therefore, I am rating FSCO as a buy.

Read the full article here

")

")