")

(Note: All amounts in the article are in EUR unless stated otherwise. At the current exchange rate, 1 EUR is around 1.11 USD. Per share figures refer to the AANNF ticker.)

Investment Thesis

I first covered Aroundtown S.A. (OTCPK:AANNF) in July, giving a Buy recommendation. Aroundtown is a European real estate company focusing on office, residential, and hotel properties. Most properties (around 85%) are in Germany, and the rest are in the Netherlands and London. The investment in residential real estate is through its subsidiary Grand City Properties (OTCPK:GRNNF, OTCPK:GRDDY). Aroundtown owns 63% of Grand City Properties.

When I initiated my coverage, I said that Aroundtown is a good investment for those who think that the real estate sector in Europe, and especially Germany, is at its cyclical low and an upswing movement over the next one or two years is likely. With an LTV (Loan-To-Value ratio) of now 62% (including hybrid debt as per the standard EPRA method) Aroundtown is quite leveraged. This would certainly not be good at the start of a downturn. However, if you believe (as I do), that the European and German real estate markets are at the end of the downturn, the additional leverage can be a benefit – while it also increases risk.

Aroundtown reported H1 financial results on August 28. Operational performance was strong, but the company fully reevaluated all its properties, resulting in a value decline of -2.4% and a net loss of EUR 329.6mn for the first half of the year. At the same time, the company said it does not foresee a further devaluation. The net value of assets is now EUR 7 per share, versus a share price of EUR 2.3. To me, that gap looks too wide and should narrow over the next quarters.

Since my recommendation in July, shares are up around 10%, but I see the investment thesis validated by the strong H1 numbers and confirm the Buy recommendation.

H1 2024 results

Aroundtown again showed a solid operational performance in Q2 2024. As a result, the full-year guidance for FFO was increased slightly to between EUR 290mn and 320mn (EUR 0.27-0.29 per share) from between EUR 280mn and 310mn.

Due to asset disposals, FFO decreased by 12% YoY to EUR 154.1mn. Net rental decreased by 1% YoY to EUR 587.6mn. A like-for-like rental increase of 2.9% almost compensated for the disposals over the last quarters. Additional disposals of EUR 475mn were signed and EUR 340mn of those were closed over the first half of the year. The disposals were done around book value.

The bottom-line saw a net loss of EUR 329.6mn. Aroundtown did a full revaluation of its portfolio, which resulted in a value decline of -2.4% versus December 2023. In absolute numbers, the decline in property value was EUR 593.2mn. The decline was most significant in the Office category, with -3%. Residential and Hotel decreased less, by -2% and -1.5%.

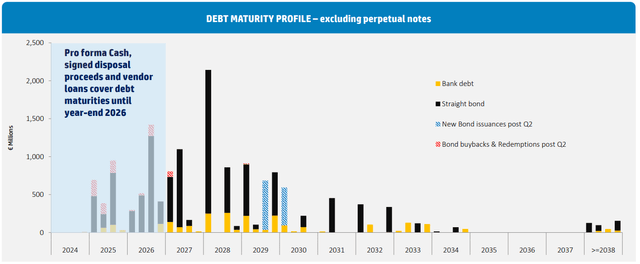

The LTV ratio now stands at 62%, which is high. On the positive side, the company has reduced its financial debt (although by just around EUR 90mn or -1%). The average cost of debt is below 2% and the debt maturity profile keeps improving. At the end of H1 all debt maturities until the end of 2026, so more than two years out, are covered.

Source: Aroundtown

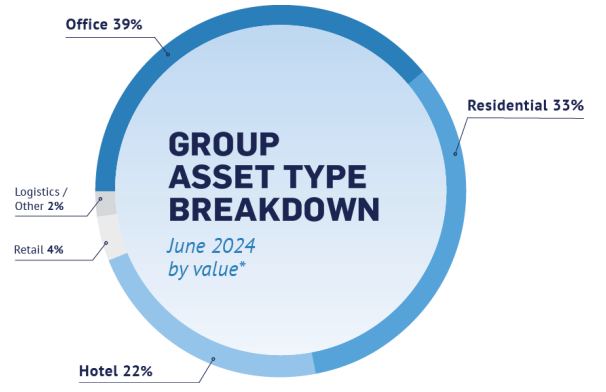

YoY the asset composition has slightly moved towards the Hotel category (+200bpp) from the Office category (-200bpp). Office/Residential/Hotel make up 94% of assets (by value). Retail and Logistics are just 4% and 2%, so those two asset classes are negligible.

Source: Aroundtown

This was driven by valuation changes, but also by (re)opening of hotels in 2023 and 2024. The rental yield is almost the same across the different asset classes (5.2% for Office, 5.0% for Residential, and 5.1% for Hotels), so this does not make much of a difference from a yield perspective, but from a risk perspective, a more balanced portfolio is a positive, in my view.

Valuation

Despite the recent share price appreciation and the devaluation of assets in H1, Aroundtown still looks undervalued when we compare the net value of assets to the share price. The EPRA net tangible value of assets of EUR 8.1bn comes down to EUR 7 per share, compared to a share price of only EUR 2.3. I think the market prices in a lot of downside risk here, and probably also the fact that with a loan-to-value ratio of 62%, Aroundtown is quite leveraged. However, this spread is simply too wide – in my view.

I think the dividend is another catalyst. As is common for German and European companies, the dividend payment is once per year. To preserve liquidity, no dividend was paid for 2022 and 2023.

Per policy, Aroundtown wants to pay out 75% of Group FFO as a dividend. This is in line with peers. Vonovia (OTCPK:VONOY) (OTCPK:VNNVF), for example, has a dividend policy that says it pays out 70% of FFO. LEG Immobilien (OTCPK:LEGIF) pays out 100% AFFO, which is around the same. At 0.28 FFO per share (the midpoint of the guidance), the dividend yield for Aroundtown would be around 9%, despite the recent increase in the share price. I expect Aroundtown to start paying a dividend again next year, but not the full 75% of FFO.

Risks to the investment thesis

The investment thesis rests on the assumption that real estate prices in Germany will not depreciate further and that interest rates will continue to go down. The two conditions are linked and depend on how inflation develops.

The good thing is that the inflation rate in Germany is trending downwards. Inflation was down to 2.3% in July, and the first indication is that it will reach 2.1% in August. It looks like we should expect further interest rate decreases in September from the ECB. However, the geopolitical situation is certainly unpredictable, and nothing is assured.

Conclusion

H1 results have confirmed the bullish investment thesis for Aroundtown. The company showed a strong operational performance, and there are clear indications that property values will not go down further and will even appreciate again. A high dividend yield and the large spread between net asset value and share price should move Aroundtown shares higher. My target price for the next 12 months is EUR 3, an upside of around 30%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here