")

Invesco S&P SmallCap Value with Momentum ETF (NYSEARCA:XSVM), launched on 03/03/2005 by Invesco Capital Management LLC., is an ETF that tracks the performance of the S&P 600 High Momentum Value Index.

While its valuation is attractive right now, XSVM’s past performance, though not indicative of future results, should give long-term investors pause. The theoretical incompatibility of value and momentum could be the main driver of such returns, although some may object that high turnover offers us another likely explanation; but then again, value needs time to work and momentum changes rob it of exactly that so we’re back at the same explanation.

Investors are most likely better off with more traditional smart-beta products as this one seems to cater to those who want to be value investors but can’t bring themselves to hold recent losers in their portfolios.

Smart-Beta Offering

The index that the ETF tracks is constituted of the 120 stocks included in the S&P SmallCap 600 Index that have the highest value and momentum scores based on the index’s methodology. The index uses a value-weighting system, in that it attributes greater weight to the relatively more undervalued stocks, and it reconstitutes semi-annually.

The indicators it uses to calculate the value score are the following: book value to price ratio, earnings yield based on TTM EPS, and sales to price ratio based on TTM sales. As for the momentum score, it is determined by the percentage change in each stock’s price in the last 12 months, adjusted for its volatility during that period.

First, the index selects the 240 stocks out of the available universe that have the highest value scores and then ranks them by momentum score to include as its constituents the top half based on momentum score.

In theory, such an ETF will appeal to investors who seek diversified factor exposure. Any judgment on XSVM is, therefore, a judgment on such an investor. There’s nothing wrong with being intentionally exposed to multiple factors, but one needs to consider how well the factors blend together.

The prospectus of this ETF states that “A “momentum style” of investing emphasizes investing in securities that have had better recent performance compared to other securities.” Does this sound like the index will select the most undervalued stocks? Probably the opposite because the market tends to price stocks by extrapolating past price performance too far into the future.

Value investing can work but it has the most potential when selecting low-momentum stocks (losers). This is probably why such stocks are the most undervalued in the first place; their recent price performance has been anything but good. So, what XSVM seems to be doing is filtering based on value only to probably filter out the most undervalued stocks right afterward because of the momentum factor. Most of the time, these two factors should be in conflict.

The ETF’s performance in relation to other funds supports this claim.

Performance & Cost

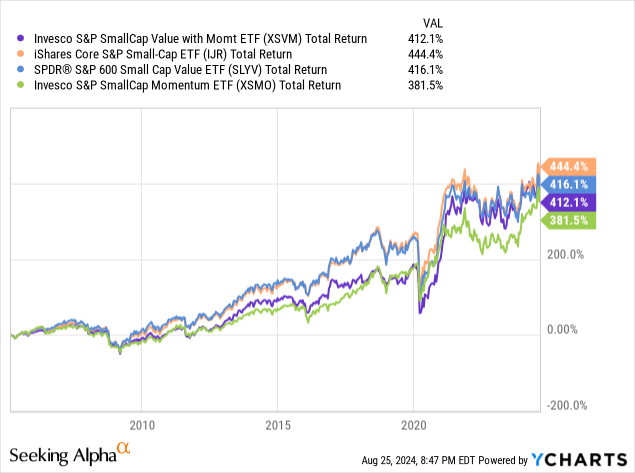

Since its inception, the fund returned 9.05% annually, which is unsurprisingly lower than the index’s 9.27%; the strategy implies high transaction costs because of the high turnover.

Now, it performed very similarly to other funds with fewer factors. The best-performing one since XSVM’s inception date was the iShares Core S&P Small-Cap (IJR), which is interesting considering its inclusion of only the size factor. XSVM has also delivered returns very similar to those of the SPDR S&P 600 Small Cap Value ETF (SLYV) even though the latter doesn’t include the momentum factor. Finally, the worst-performing fund was the Invesco S&P SmallCap Momentum ETF (XSMO) which excludes the value factor.

Notice, however, how XSMO underperformed IJR and SLYV by a much wider margin for a very long time before XSMO’s recovery after the COVID-19 panic. This actually creates a case for the ETF’s usefulness to traders; its recovery from its 2020 low to its 2022 high was far more spectacular than that of the broad market, although its recovery since the Fed started raising the Federal Funds rate is much more modest.

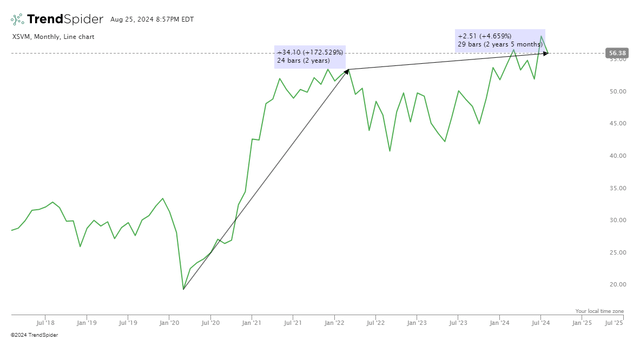

TrendSpider TrendSpider

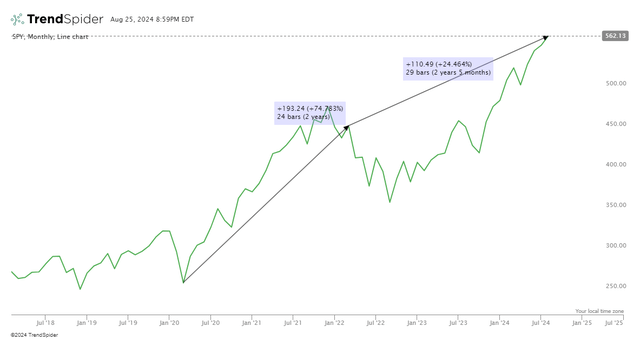

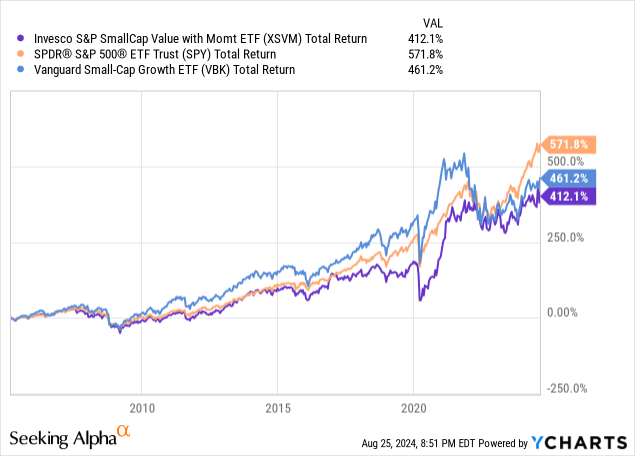

Of course, it underperformed the market in the long run and its growth counterpart by a wider margin than when compared to the other smart-beta funds:

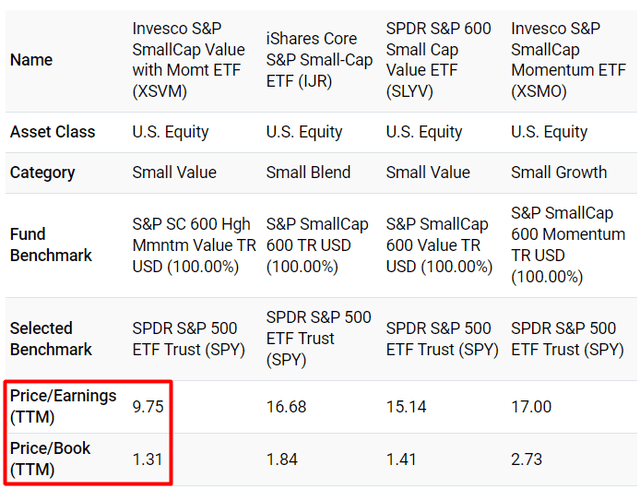

Interestingly, XSVM’s valuation is currently exceptional when compared to its peers’:

portfoliovisualizer.com

Now, during the last fiscal year, its portfolio turnover ratio was 86%, which is incredibly high but pretty consistent with a momentum ranking system. In any case, this supports the theory that momentum prevents value from realizing its full potential because undervalued stocks take time to recover, but changes in momentum may not give them a chance to do so in such a ranking system.

Last, its expense ratio of 0.36% is high but fair in the context of smart-beta products.

Risks

Regardless, the high turnover and fees could result in a widening tracking error, making this ETF inefficient in the long run. However, another risk that concerns me comes from blending together value and momentum. Long-term investors should understand that this may be the reason for its long-term underperformance and, therefore, a driver for potential long-term underperformance in the future which represents an opportunity risk.

Of course, funds like XSVM carry small-cap risk and this may be a factor in your overall performance depending on how you handle the likely larger drawdowns that come with such funds in market downturns.

Also, there is a concentration risk present here since the fund has allocated 29.3% to Financials and 25.53% to Consumer Cyclical.

Verdict

Despite the risks, the valuation is attractive, and I don’t believe that long-term investors would incur losses in the long term by selecting XSVM. However, in the presence of other smart-beta options for which the results are consistent with the idea that size and value are the predominant factors for excess returns and additional ones are most likely to be a drag, I see no reason why long-term investors should go with it. So, I am rating it a hold.

In this case, the momentum factor can function more like a coping mechanism because holding the most undervalued stocks in the small-cap universe is undeniably hard on an investor’s emotional health. But sticking to broad-market funds and foregoing smart-beta options altogether seems more rational to me.

What’s your opinion? Do you agree with this thesis or not? Let me know below, and thank you for reading.

Read the full article here