")

Performance Assessment

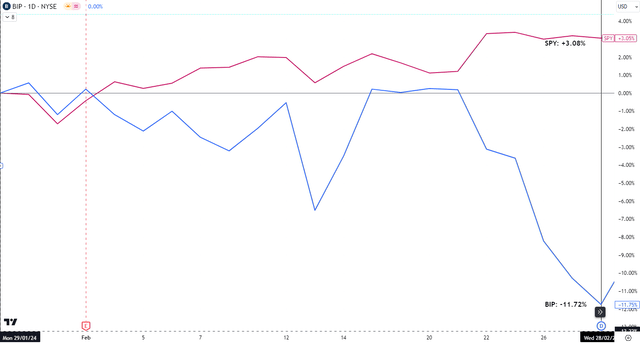

I initially had a bullish stance in my last article on Brookfield Infrastructure Partners (NYSE:BIP). Since then, the stock has lagged the S&P 500 on a total shareholder return basis:

Performance since Author’s Last Article on BIP (Seeking Alpha, Author’s Last Article on BIP)

However, in reality, the actual performance is worse as I had changed my rating at the end of February 2024 to a ‘Neutral/Hold’ due to expected delays in the payout period of major investments (discussed later below). Since my last article’s publication on January 29, 2024 till the change in stance date, the SPY generated +3.08% vs BIP’s -11.72%:

BIP vs SPY Performance (TradingView, Author’s Analysis)

Thesis

3 quarters later, I have still lost my enthusiasm for Brookfield Infrastructure Partners, as I note the following:

- Capital deployments are growing well

- But delayed Intel project postpones realization of returns

- Valuations are near trough levels

- Relative technicals signal caution

Capital deployments are growing well

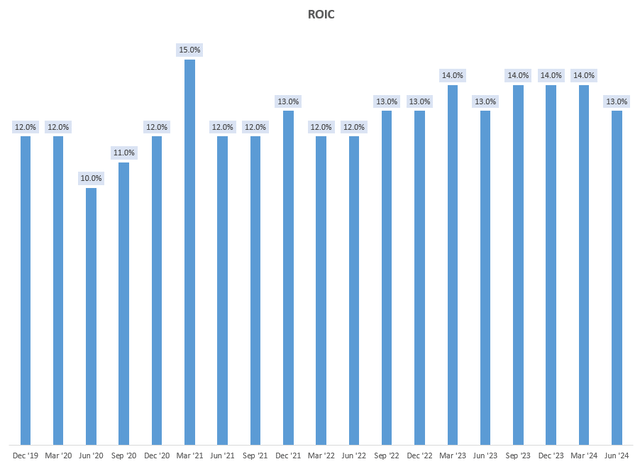

BIP is an investments business. The 2 key things that matter most for how it makes money in the future is the growth in the amount of capital managed and the returns generated on that capital.

The returns on invested capital (ROIC) are generally steady at 12-14% (12-15% is their target IRR):

ROIC (Company Filings, Author’s Analysis)

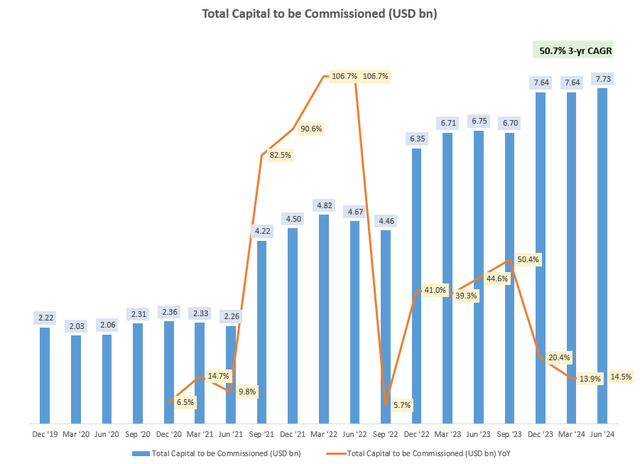

Hence, the focus is on future capital put to work, called capital to be commissioned. This is growing very well in step-jumps at a 50.7% 3-yr CAGR:

Total Capital to be Commissioned (USD bn) (Company Filings, Author’s Analysis)

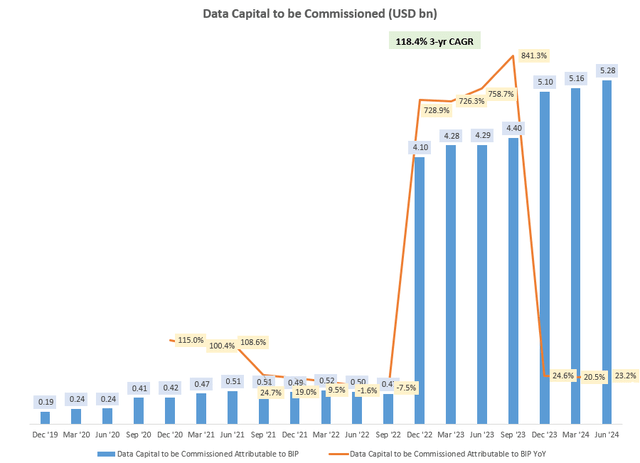

Out of the overall $7.73 billion of capital to be commissioned as of Q2 FY24, the Data segment is responsible for $5.28 billion of that, corresponding to a 68% mix:

Data Capital to be Commissioned (USD bn) (Company Filings, Author’s Analysis)

The strong growth in data centers in response to burgeoning AI investments is what is driving most of this growth.

But delayed Intel project postpones realization of returns

In the Data Transmission & Distribution segment, BIP has a partnership with Intel (INTC) to invest $3.9 billion in the building of 2 semiconductor foundries in the United States. $980 million has already been spent till date, leaving $2.9 billion of capital spend left to be deployed. That amounts to 55% of total data capital to be commissioned and 38% of total capital to be commissioned; in other words, a large chunk of capital to be deployed is concentrated on this commitment with Intel. In terms of the economics of this deal, certain Wall St analysts have noted concerns about a lower return and longer payout period for this deal:

…relatively low return out of that [Intel] deal. And then, especially, just the multi-year, or just the lag between capital out the door before it shows up in cash flow

– Robert Kwan, RBC Capital Markets in the Q2 FY24 earnings call

Brookfield Infrastructure Partners’ management assured investors that the Intel deal would be high-yielding, but admitted that the payout period could be at least 2 years longer:

I think in the Intel transaction, in the end, we’re going to find that it’s going to be a very high returning opportunity. The situation today, though, is we still have a couple years to wait before we truly see the benefits…

– CEO Samuel Pollock in the Q2 FY24 earnings call

I believe management is referring to an additional 2-year wait based on news in February 2024 that Intel’s plan for building 2 new fabs in Ohio with an initial timeline for starting chip manufacturing in 2025 has been pushed out 2-3 whole years to 2027-2028.

Given Intel’s terrible track record in overpromising and underdelivering, I believe there are further risks to an extended timeline here, which would not pose well for BIP stock. Hence, it is logical that the status of Intel’s semiconductor foundry construction in the US is a key monitorable to track for the overall thesis.

Valuations are near trough levels

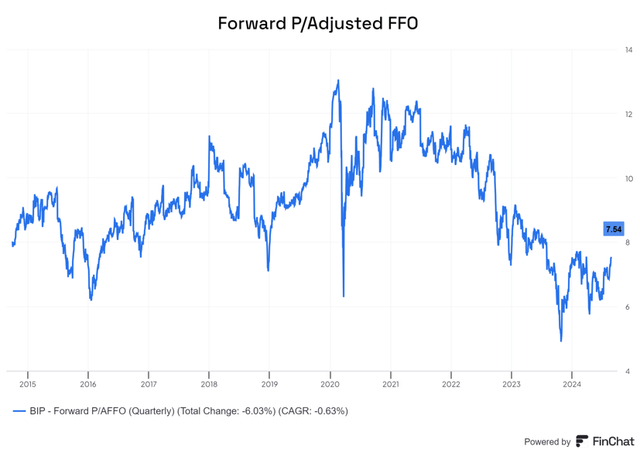

BIP 1-yr fwd P/AFFO (FinChat)

At 7.54x, BIP is still trading near decadal lows in terms of a 1-yr fwd P/AFFO valuation multiple. Given the broadly positive fundamental outlook in capital deployment opportunities (despite the lags), I believe this leads to a favorable valuation scenario.

Relative technicals signal caution

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do. All my charts reflect total shareholder return as they are adjusted for dividends/distributions.

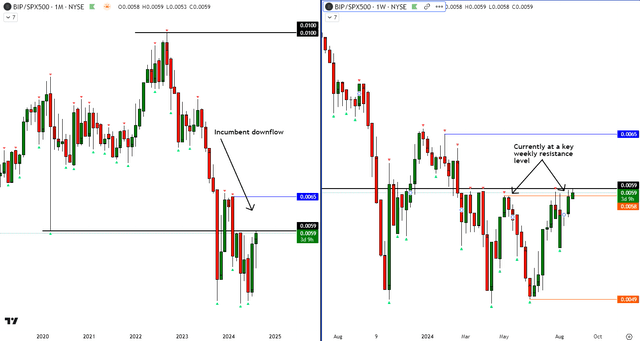

Relative Read of BIP vs SPX500

BIP vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

On the relative read of BIP vs the S&P 500 (SPY) (SPX), the ratio prices are coming in from an incumbent downflow, which has slowed down since late 2023. Currently, the prices are close to a key weekly resistance level. Hence, I believe there is downside to sideways risk in the stock vs the S&P 500, limiting the potential for positive active returns.

Takeaway & Positioning

I believe Brookfield Infrastructure Partners is positioned well to grow capital deployments, upon which it earns solid returns of 12-14%. However, there are some headwinds and downside risks in the form of 2-3 year project delays in its partnership with Intel to build out 2 fabs in the United States. The magnitude of these projects is significant as it amounts to a total of 38% of incremental capital to be commissioned. And given Intel’s poor execution track record, I recognize the risk for further postponements that would drag out the payout period even further.

On the valuations side, however, things look a bit more positive as BIP is trading near a decadal low 1-yr fwd P/AFFO multiple. But to counter this, the relative technicals vs the S&P 500 highlight reasons to be cautious as the ratio prices are currently near a key weekly resistance level.

Rating: ‘Neutral/Hold’

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence. I also have a net long position in the security in my personal portfolio.

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")