")

I do not like most YieldMax investment products because they are often mis-marketed to income investors. Fundamentally, I believe there is a time and place for covered call strategies. Using them as a source of retirement income is not one of them because they’ll almost always lose principal value over time. Unlike traditional stocks and bonds, principal losses on call-option strategy ETFs will usually be permanent and reflected in permanent dividend declines. Thus, they’re both a terrible way to protect wealth and a poor way to earn a stable income.

When all dividends are reinvested (or at least maintained within one’s portfolio – not used as income), they can earn excess risk-adjusted returns in specific market conditions. Categorically, the YieldMax “fund of funds” YieldMax Universe Fund of Option Income ETFs (YMAX) is always a poor investment because it has compounded management fees and is inherently not designed for strategic call selling.

However, the YieldMax TSLA option “income” fund YieldMax TSLA Option Income Strategy ETF (NYSEARCA:TSLY) may have strategic value because Tesla, Inc. (TSLA) stock generally correlates less to the S&P 500 (SP500), typically around 0.15X to 0.35X using monthly returns. Selling options on a highly volatile asset with low market correlations has added potential to boost risk-adjusted portfolio returns.

Given TSLA’s abnormal volatility and low market correlation, I believe TSLY deserves closer inspection, so investors may understand how to use it to improve risk-adjusted portfolio returns strategically.

Quick Primer on How TSLY Works

Investors must realize TSLY’s strategy to understand its risks and rewards. Some may merely look at its distribution rate and assume it’s a cash-generating machine. In reality, nothing can be further from the truth. To say TSLY is an income strategy is akin to an insurance provider using your insurance premiums as personal income.

With TSLY, imagine you are selling home insurance on TSLA. You collect a nice premium on it, but if it loses value, you will cover those losses. As such, those premium payments should be saved to cover the inevitable bearish swings in TSLA. If those premium payments are used as personal income, bear markets for TSLA will result in portfolio losses. Because TSLY pays out a distribution of roughly all of its premium returns, it loses value over time.

In effect, TSLY sells calls 0-15% above the current TSLA price while owning a synthetic position in TSLA. A synthetic long position is made by buying a call option and selling a put at the same price. YieldMax does this in a manner that gives it ~100% exposure to TSLA. Typically, synthetic long positions can be used to gain abnormal leverage, but instead, YieldMax aims to keep its exposure at 1:1, investing the unused capital in income-earning short-term Treasuries. In my view, there are no benefits nor risks associated with its use of a synthetic long vs. an outright position, though it may use this strategy so that its traders can focus on the options market.

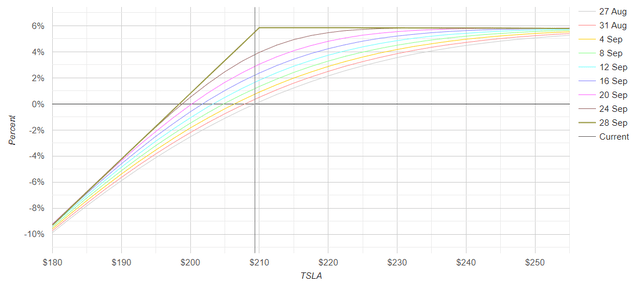

The fund currently owns a synthetic position on $210 strike price options at an October 18th expiry, though it owns some calls at $215, potentially made to give it slightly better appreciation potential. It sells August 30th call options at a $225 strike price. The premium returns on those options are very low since they’re close to expiration. To better understand the “typical” payoff of TSLY to TSLA, I will use the same October 18th synthetic long and assume it will roll its covered calls at the money ($210) for September 27th. Here is the payoff of that strategy over the next month:

TSLA one-month option payoff ATM covered call with synthetic long (OptionProfitCalculator)

Who wouldn’t want a 5.9% yield in just a month? That’s 70% in a year, or around 98% if we account for compounding. However, TSLY will generally not benefit from compounding because its dividend is bound to decline with its price.

TSLY is Doomed To Decay Toward Zero

TSLA call options are very lucrative, giving TSLY a distribution rate of 84%. However, based on the SEC metric, that should not be confused with its actual dividend yield of 4.25%. Call option premiums are not dividends; they are distributions of capital. Treating them as income (using them for spending money) will result in permanent capital losses because those premiums offset the fact that TSLY has a capped upside but will face losses nearly equal to TSLA. This is why all call option ETFs will decline over time, even in bull markets. However, they may generate similar or superior risk-adjusted returns if all distributions are reinvested.

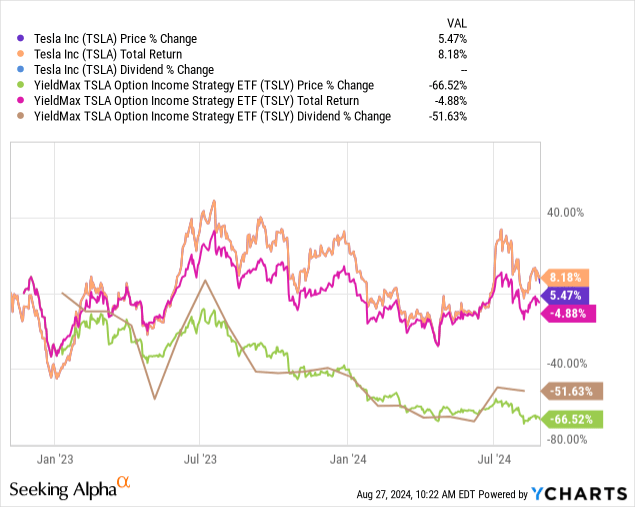

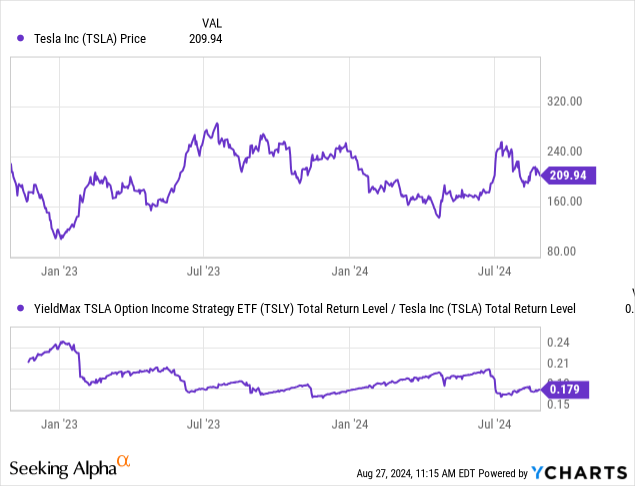

The performance of the “TSLY reinvested dividends” strategy can be seen in the total returns of TSLY. Interestingly, TSLY’s total return equals TSLA’s, with slightly lower returns and overall volatility. However, the price of TSLY has consistently fallen, being flat in bull markets but about equally negative in downturns. Crucially, TSLY’s “dividend” (really a distribution) has fallen linearly to its share price, as expected. See below:

There are two key reasons TSLY is not an income strategy. One, it can only be a stable investment if all distributions are reinvested. Two, its distribution will decline with its share price because a lower share price means less capital invested into call options. That juxtaposes traditional income investments, such as bonds and high-dividend stocks, where we can generally expect payments to be unchanging outside significant changes in corporate cash flows. Stocks and bonds rise and fall, but unlike TSLY, they are not doomed for permanent losses. TSLY will decay over time, not as a matter of speculation on TSLA, but as a mathematical fact based on its strategy.

When TSLY Works Best

If we assume market efficiency, which, in my view, is true for options, there is no inherent risk-adjusted benefit of selling calls. Covered calls give lower overall volatility at the cost of typically lower total returns (returns assuming distribution reinvestment). This stems from covered calls limiting appreciation, but the premiums offset downside volatility, mainly when implied volatility levels are high. Over the past year, TSLA has had a one-year standard deviation of monthly returns of around 15.5% compared to ~10.5% for TSLY. Its total returns over the past year are -13.5%, compared to TSLA at -10.6%.

Historically, TSLY underperforms TSLA during appreciation periods because it has capped upside and outperforms during other periods. See below:

The ideal for TSLY is high perceptions of volatility, which drive premiums, but low realized volatility. Common examples include before earnings releases. However, implied volatility (or option premium) levels will most often be reasonably elevated for significant implied moves following a significant earnings release.

In my view, it is best to buy TSLY when one expects little price changes. With TSLA, implied volatility will almost always be high because TSLA has high historical volatility. However, if we look at periods such as mid-March to mid-June of this year when TSLA was abnormally quiet, we see excess returns for TSLY. TSLY had a total return of 15% over that period compared to TSLA at 8.8%. TSLY also had lower volatility of returns, signifying the benefits of call options during neutral market conditions.

The best conditions are when one expects a flat market immediately following significant declines. Option premiums, or implied volatility levels, frequently rise to extreme highs during sharp downturns as investors race for hedges or those selling naked put options race to close or are margin-called. That likely occurred during the early August market correction, which saw the S&P VIX Index (VIX) briefly rise to 65%. Thus, TSLY may have added value during a market panic, particularly if one honestly believes that the panic will be short-lived.

TSLA’s current implied volatility level is 47%, meaning its options are priced, so investors expect a 47% price at one standard deviation over the coming year. That is akin to saying that the market believes TSLA will most likely remain at +/- 47% of its current price over the next year, which aligns with its historically normal level. That implied volatility level is at the 42nd percentile of TSLA’s IV range, meaning it is slightly low compared to its historical norm. In other words, TSLY’s premiums should be slightly below normal, giving it marginally worse risk-adjusted returns.

In my view, investors are likely best off buying TSLY under two conditions. One, they believe TSLA is either undervalued or fairly valued. Two, the implied volatility level is above the 75% percentile, usually after a sell-off or before a key earnings announcement. That IV level will cause TSLY’s distributions to be abnormally high, giving it potentially better returns. The second condition is not satisfied today. I think TSLA is also egregiously overvalued, though my view is subjective, and I’m sure many readers will disagree.

The Bottom Line – TSLA is Overvalued

I am bearish on TSLY because its implied volatility level is too low to match my expected volatility on TSLA. I expect TSLA will face significant volatility over the coming year due to concerns regarding its valuation and a continued growth slowdown. TSLA’s price-to-sales is 7.6X compared to Toyota Motor Corporation’s (TM) at 0.8X. Toyota is a much larger company than Tesla in terms of revenue, as are the next seven largest publically traded car companies. Despite that, Tesla’s market capitalization is just above the combined market capitalization of the other seven.

Such an extreme valuation gap can only be justified by superior revenue and income growth expectations. Tesla’s sales are about flat YoY, while its EBITDA is down 27%. It is also expected to see its EPS decline by 7% on a forward basis, while Toyota and most of its peers are expected to see their income grow, likely as they expand further into the EV market.

In the past, TSLA’s valuation premium was justified by its superior growth and first-mover advantage in the EV space. Today, I’d argue its competitors may have an edge in electric vehicles because their greater size gives them larger capacity for vertical integration. Further, although I have little issue with CEO Elon Musk’s outside activities, the same cannot be said for most would-be EV buyers, who are more often liberal. Recent surveys suggest that 77% of Republicans are not interested in buying an EV car this year, while its position in corporate brand recognition has collapsed. Given more non-Tesla EV options, I imagine this will result in worse sales declines in 2025 compared to peers. Thus, I believe TSLA is not only overvalued, but immediate bearish catalysts are facing its growth and profitability. Therefore, I have opened a short position in TSLA.

YieldMax does have a bearish alternative to TSLY called YieldMax Short TSLA Option Income Strategy ETF (CRSH), which sells covered puts. In my view, it is most likely that TSLA will face significant declines immediately following its earnings instead of slow-drawn-out declines. Thus, I believe an outright short is likely the best move, though CRSH may be suitable for those who are not immediately bearish but instead believe TSLA is unlikely to rise. Theoretically, investors could buy CRSH and TSLY to create a short “straddle” option strategy, which would perform very well in a flat market. In my view, that would not be a good approach today because I believe TSLA’s risks are high while its implied volatility is slightly low.

Read the full article here