(NASDAQ:TITN)")

Thesis

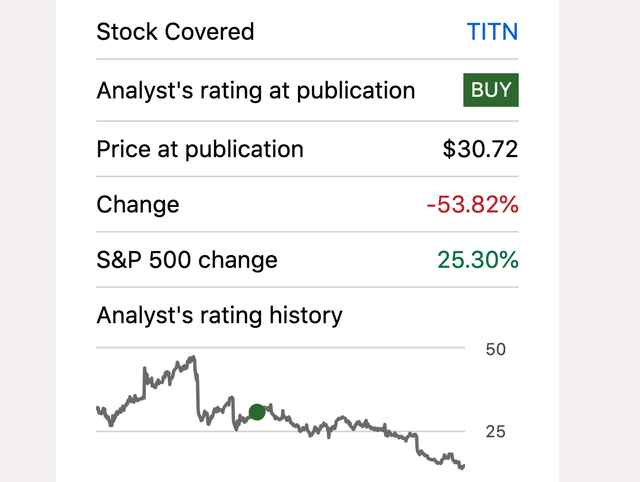

Since my write-up of Titan Machinery Inc. (NASDAQ:TITN) in July 2023 (“Titan Machinery: A Colossus Mispriced In The Agri-Construction Realm”), it’s been one of my worst (long-term without update) “Buy” calls to date, with a -54% change versus the S&P 500’s (SP500) 25% return during the same period.

Grassroots Trading TITN “buy-call” performance (Seeking Alpha)

At the time of my analysis, all the stars appeared to line up, from great earnings to data across the board pointing to undervaluation.

In all of my work, I tend to culminate with an explanation of the risks, no matter how wonderfully a stock is performing. There are always risks; this is the nature of the game. In Titan’s case, to paraphrase my own work, in the first quarter, the company saw a big jump in operating expenses by 26.8%. This was mainly because of expenses from buying new businesses and rising costs tied to their growing sales. I warned that, if these costs weren’t managed well, they could dent profits. I also pointed out that interest expense had risen considerably, which could put even more financial pressure on the company. And I observed that international sales had dropped slightly, citing the continuing war in Ukraine and currency fluctuations around the world. And, finally, I pointed out that Titan’s inventories increased, which could be risky if demand dries up or if they can’t get their hands on adequate supplies of the product that customers demand.

However, ultimately, I gave TITN a “Buy” rating because of Titan Machinery’s impressive growth record, its relatively depressed valuation vis-à-vis other firms in the sector, and its promising outlook over the next couple of years, despite some “manageable” risks. The company’s financial results over the (then) most recent quarters had suggested that it continued an upward run in its revenue and profitability. Its leverage ratio was high, and its operations carried some risk, but all in all, I saw a multitude of favorable factors: the latest financial condition and sector performance, coupled with a P/E ratio that suggested that the company was underpriced, proved to be a favorable investment for those who were not deterred by its 0.00% dividend yield.

Today, I’ll be catching up with the company to find out what’s been going on, and more importantly, why these risks had a much bigger impact than a handful of other analysts have also missed this past year. With Q2 earnings set to be announced later this week (8/29/2024), I’ll be covering most of the relevant data to get a clearer picture of what investors could expect moving forward.

About Titan Machinery

Titan Machinery was established in 1980 and currently maintains their headquarters in West Fargo, North Dakota. They are recognized domestically and globally as leaders in the agricultural and construction equipment markets.

Titan’s equipment aids food, fiber, feed grain, and renewable energy production while meeting home, garden, commercial, residential, and government property maintenance needs. Within their construction segment, their equipment mix includes heavy machinery for large projects as well as light industrial machines that help facilitate smaller residential construction tasks, road/highway construction tasks as well as energy/forestry operations.

Titan also goes beyond traditional sales models by renting equipment and offering ancillary services such as equipment transportation, farm data management products, GPS signal subscriptions and CNH Industrial Finance and Insurance products.

Wall Street Rating

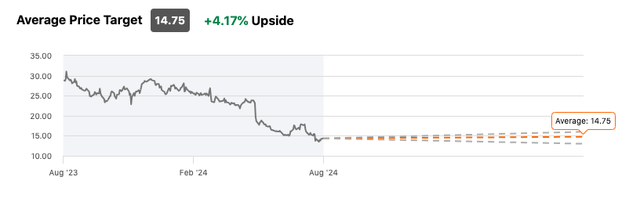

Wall Street consensus has the stock at an average “Hold” rating with a moderate expectation of gains based on the price target, with 4.4% upside potential price movement.

Seeking Alpha

Most recently, TITN got a downgrade to “Market Perform” from Northland Securities (08/20/2024), citing falling commodity prices and weaker-than-expected equipment sales.

Peer Performance

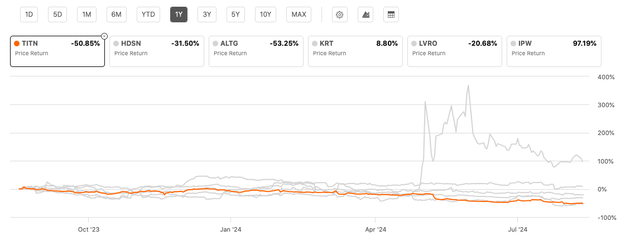

Compared to its peers in this space, you’ll notice losses across the board, with ALTG taking the lead as the biggest loser over 1Y, in stark contrast to IPW’s near 100% gain.

Seeking Alpha

Keep in mind, IPW is a low-priced stock with a market cap of only $50 million, whose IPO was in 2021.

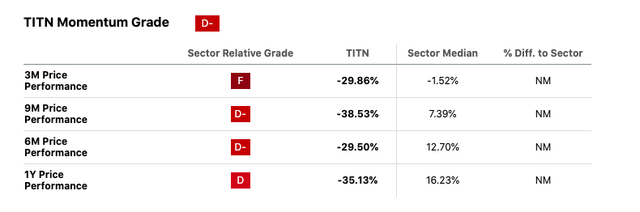

Seeking Alpha’s Warning

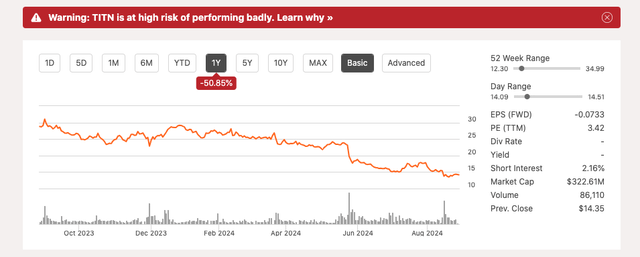

Every so often, subscribers will come across a “Warning” label on a stock’s summary page. Unfortunately, TITN has one of these “Scarlett” labels, and according to Seeking Alpha’s metrics, TITN is flashing warning signs that it might struggle ahead.

Seeking Alpha

The stock’s momentum is tanking, dropping almost 30% in the past three months, while the broader industrial sector barely dipped 1.5%.

Seeking Alpha

No recent boosts in earnings forecasts have added to the concern. Compared to its peers, TITN keeps getting poor grades across different time frames—three, six, nine months, and even a year. This led to a “Sell” rating from their stock evaluation system. Stocks with this rating usually underperform dramatically, typically losing around 20% annually compared to the market. According to Seeking Alpha’s Quant metrics, TITN is a risky bet.

Weak Guidance

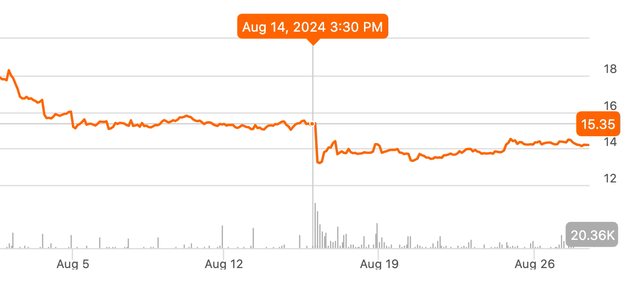

To make matters worse, Titan Machinery’s stock declined by 26.8% after the company announced (on August 14, 2024) disappointing expectations for its second-quarter earnings and revenue. The company said it expects to make about $634 million in revenue, which is lower than expected, mainly because sales of its equipment were weaker than anticipated. As a result, their adjusted earnings are forecasted to be $0.17 per share, this is far below the $0.60 per share analysts had predicted.

TITN August 14 price drop (Seeking Alpha)

The company’s President and CEO, Bryan Knutson, explained that falling commodity prices, high-interest rates, and mixed growing conditions have hurt farmer confidence, leading to lower sales of agricultural equipment. Since the start of the year, prices for key crops have declined by another 10%-20%, further affecting their sales in the second quarter.

Titan Machinery Financial Strategy

Titan Machinery’s Q1 2025 saw total revenue jumping 10.4% to $628.7 million. Strategic acquisitions and a meager 1.1% bump in same-store sales backed up some of this growth. The agriculture segment delivered, with sales climbing 5.8% to $447.7 million and same-store sales in this segment rose 4.3%, even with the market facing some tough times.

A key highlight in the last quarter was the 29% jump in service revenue. Meanwhile, the company is pushing hard on customer care, especially in parts, service, and precision businesses, which offer some steadier growth. At that time, management incorrectly emphasized, and I’m paraphrasing here, that farmers’ strong finances, helped by solid land values, are expected to keep demand steady, even with a dip in net farm income. Evidently, as their most recent downward guidance suggested, they were mistaken.

US farmers will have a rocky ride in 2025, at least if the 2023 and 2024 experiences are any guide. If nothing changes, their income might take a dramatic hit, which would represent tremendous financial stress on farmers. In fact, farm income in 2024 is expected to be down about 25.5% from 2023 earnings. Essentially, many of the things plaguing agriculture right now will likely continue into 2025.

Key Factors:

Falling Crop Prices: Corn and soybean prices will continue to decline in 2024, and probably into 2025 as supply surpasses global demand and other economic factors. In short, farmers will have less cash.

Corn Futures (Finviz) Soybeans Futures (Finviz)

Higher Costs to Produce It: The costs to produce food—such as fertilizer, fuel, and labor—are increasing. As a result, farmers are losing money more quickly than they can make it by selling their crops.

Less Government Assistance: Recently, the government has stepped in with some financial assistance. But in 2024, the level of help is likely to be cut, and farmers are going to find themselves more vulnerable to the vagaries of the market and to bad weather.

Land Values: Farmland is getting more valuable, which helps farmers who own land stay stable, but it also makes it pricier for any new farmers or those looking to expand.

Rising Debt: Farmers are expected to rack up more debt in 2024. If their income keeps dropping, paying off that debt might get tough, leading to financial trouble.

What This Means for 2025:

Squeeze on Profits: As crop prices drop and costs rise, profits will be hard to come by in 2025. Smaller farms could close or be taken over by larger ones.

Need for Strategic Change: Farmers might have to become more efficient, shift crops, or invest in new technology to be competitive. Precision agriculture might be the key to reducing costs and enhancing operations.

Volatility in the Market: The global economy will remain volatile, subject to shifting trade policies and “climate change”, making it difficult to know what prices and incomes will look like in the future.

Basically, factors that are out of Titan’s control.

Meanwhile, Titan’s management said they’re working on a long-term plan to cut inventory down to healthier levels by FY 2026 (remember they’ll be announcing Q2 2025). This could boost their financials. So while they’re actively managing inventory to end the fiscal year at similar levels to where it began, they’re expecting bigger drops in FY ’26. This move aligns with industry demand and could help dodge extra costs like Floorplan (loans often secured against the inventory held “on the floor” of the dealership or store) interest. Plus, their approach to sales—offering interest waivers, extended warranties, and price adjustments—aims to move inventory while keeping an eye on long-term customer relationships and efficiency.

And finally, in construction, lower rental fleet use hit hard due to weather and market shifts, but management somehow expects things to pick up as the season goes on. They’re cutting down on construction equipment inventory, which is a good move.

TITN’s Valuation

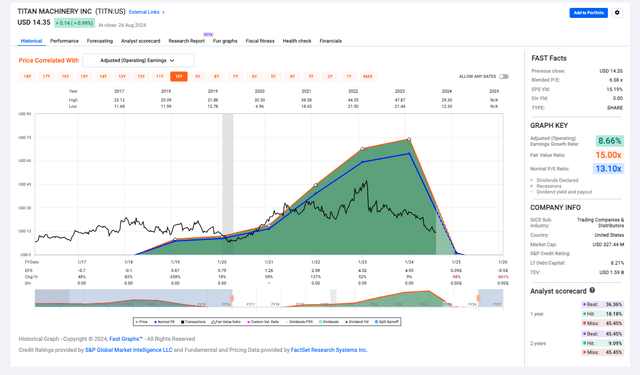

Once again, slightly over a year later and the data on Titan Machinery still looks undervalued…and solid. Even Seeking Alpha’s metrics back this up with an “A+” rating on valuation. At the time of my analysis, the stock was trading at $14.35, so with a (blended) P/E ratio of 6.58x, way below the fair value P/E of 15.00x suggests an undervalued narrative. With an EPS yield of 15.19%, it’s clear the stock is pulling in decent earnings for its price. Their earnings growth rate is 8.66%, not very high, but it’s steady, showing Titan Machinery is still growing its earnings even when the economy isn’t playing nice. Furthermore, the current P/E ratio compared to the normal 13.10x P/E shows this stock is pretty cheap right now. This could indicate that the market is overreacting to those aforementioned sector worries or has overestimated the risks.

Fast Graphs

Titan’s long-term debt to capital ratio is just 8.21%, their balance sheet looks solid, and they’re not relying on too much debt to get by. So, with a market cap of $327.44 million and a total enterprise value of $1.59 billion, they’re small but backed by a decent pile of assets. That’s a good safety net if things continue to go south.

Risks & Headwinds

To put it mildly, management, which should have had a finger on the pulse of the market, didn’t accomplish what they thought they would. This was mainly because farming wasn’t as strong, and interest rates went up. This made the start of their fiscal year slower than expected. As a consequence, profit margins dropped because they had to sell equipment for less money while managing their inventory. Now, for the remainder of the year, they’re expecting to make even less money from selling farming equipment, which could be the lowest they’ve seen in the past ten years.

The company’s expenses went up a lot, by almost 22%, to $99.2 million, mostly because they bought new businesses and paid higher salaries and benefits. This cut into their profits. As a result, the money they actually made dropped significantly, down to $9.4 million compared to $27 million the previous year. In the construction part of the business, sales at stores that have been open for at least a year dropped slightly by 0.7%. Over in Europe, sales fell even more, by 12.5%, which shows people aren’t buying as much there.

They also had to pay a lot more in interest, $9.5 million compared to $2.5 million last year, mainly because they had more inventory and needed money to finance the acquisitions. The construction part of the company also struggled to rent out its equipment as much as before. Usage dropped considerably due to bad weather, a late start to the construction season, and weaker demand in certain markets like housing and commercial buildings.

Finally, the company continues to work down its inventory into FY’26, which will increase pressure on margins. This could be a continuing issue for the company. Gross margins are already declining, and we don’t see that trend changing. The company continues to aggressively clear inventory, which is squeezing margins. Furthermore, the company’s price cuts to reduce inventory will put downward pressure on selling prices, which will further squeeze margins if the market doesn’t pick up.

TITN Rating

I would place a high-risk “Hold” rating on to Titan Machinery Inc. stock because I believe the current low price might already reflect all the bad news I just unraveled that the company has faced (and probably will face). Furthermore, the stock still looks cheap compared to others in the industry. Overall, Titan Machinery is financially stable with low debt, giving it some protection during these tough times. If the market has reacted too negatively, the stock’s current low price might not truly reflect its potential, so holding on could allow you to benefit if, or when, the company recovers.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here