")

")

")

Investment Thesis

Company Overview

Xcel Energy (NASDAQ:XEL), founded in 1909 with headquarters in Minneapolis, Minnesota, is an electricity and natural gas provider to eight states (portions of Colorado, Michigan, Minnesota, New Mexico, North Dakota, South Dakota, Texas and Wisconsin) through its utility subsidiaries (NSP-Minnesota, NSP-Wisconsin, PSCo and SPS), along with the transmission-only subsidiaries (WYCO and WGI). In addition, it also has three non-regulated subsidiaries, including Eloigne, Capital Services, Venture Holdings, Nicollet Project Holdings.

Strengths and Weaknesses

Xcel has three strategic priorities, two of which are mostly shared by other utility companies, such as “Enhance the Customer Experience” and “Keep Bills Low”. The one that has more unique cost-and-benefit curve to the company, “Lead the Clean Energy Transition”, is its biggest priority.

xel (xel)

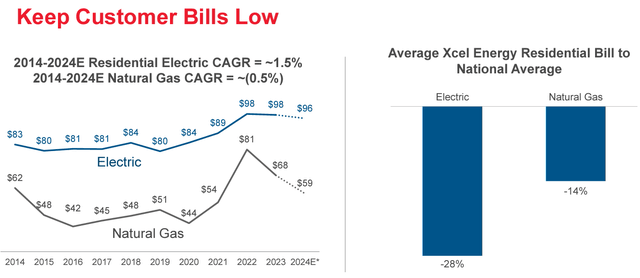

Translating these priorities into business development and growth, we will look into each priorities. Enhancing customer experience currently means installing smart electric meters for Xcel. These meters can provide near-real-time digital data to customers regarding their energy information and how to manage the use to lower the bills. Keeping bills low means keeping residential electric bill growth to 1.8% per year and natural gas bill to 1.1% per year for the past ten years.

xel (xel)

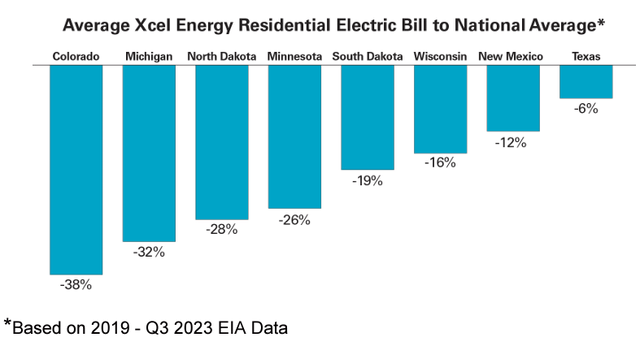

The results are evidently beneficial to its customers. The states it serves registered 6-38% lower in their residential electric bills to national average, but 7 out of 8 are lower by double digits. The lowest is in Colorado, registering a whopping 38% lower in electric bills.

xel (xel)

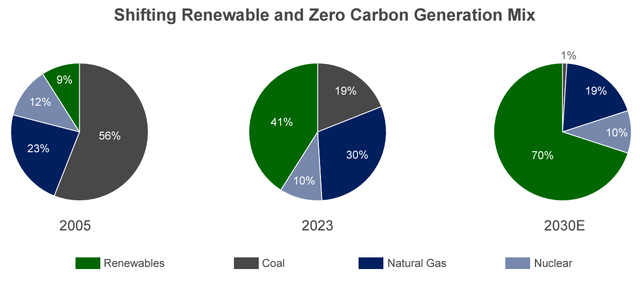

Since electric accounts for 70% and natural gas counts for 19% of its total energy mix, the weighted average of the annual inflation rate of the bills would be 1.47% on average.

xel (xel)

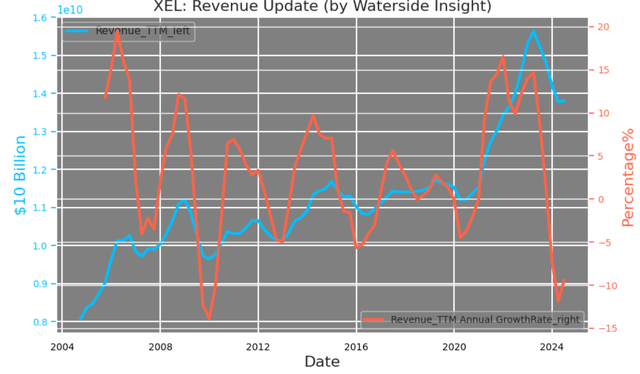

Without raising the bills for its customers, Xcel still managed to grow its revenue on average at 4-5% annually for the past ten years on a TTM basis, exceeding the annual rate that it raised the bill at on its customers. The growth rate has only come down recently when TTM revenue was at all-time high of $15-16 billion to now around $12 billion.

xel (xel)

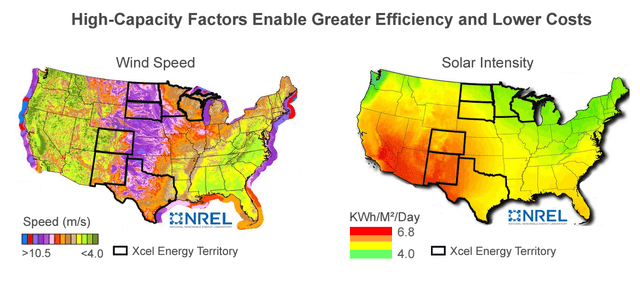

What drove this excessive growth on the top line? We turn our attention to its most important priorities, clean energy transition. Xcel Energy situated in an advantageous geological location for clean energy generation. The company serves to customers that are situated in areas overlapping regions with the highest wind speed and most solar intensity in the US. For example, North and South Dakota can have wind speed top 8-10.5 m/s while Colorado, New Mexico and Texas have solar intensity reaching 6.8 kW/m2 /day. Simply put, Xcel has the natural resources to generate clean energy efficiently, providing higher clean energy capacity factors with lower operating costs.

xel (xel)

Xcel has made numerous efforts in clean energy development, including the “Steel for Fuel” strategy that by taking advantage of the naturally high capacity factors in solar and wind combining with renewable tax credits to avoid higher fossil fuel costs.

xel (xel)

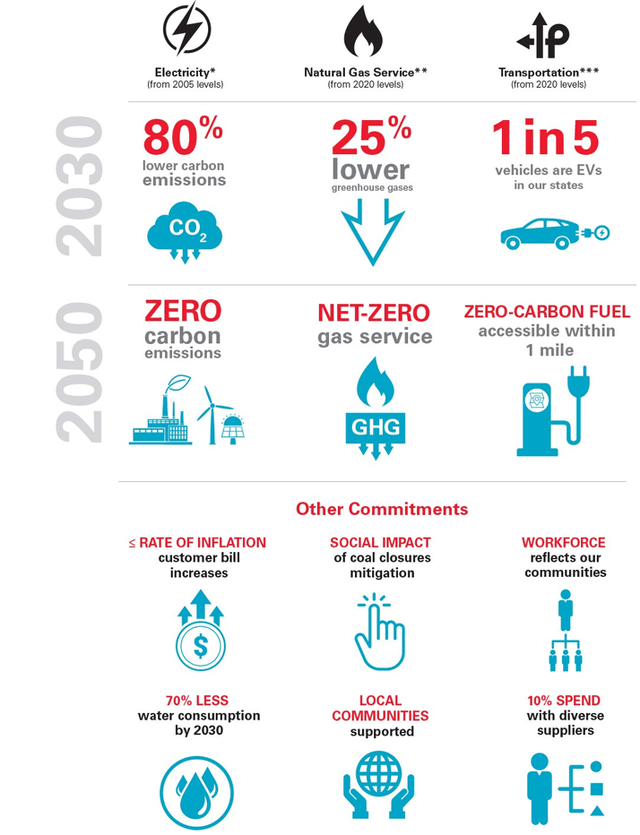

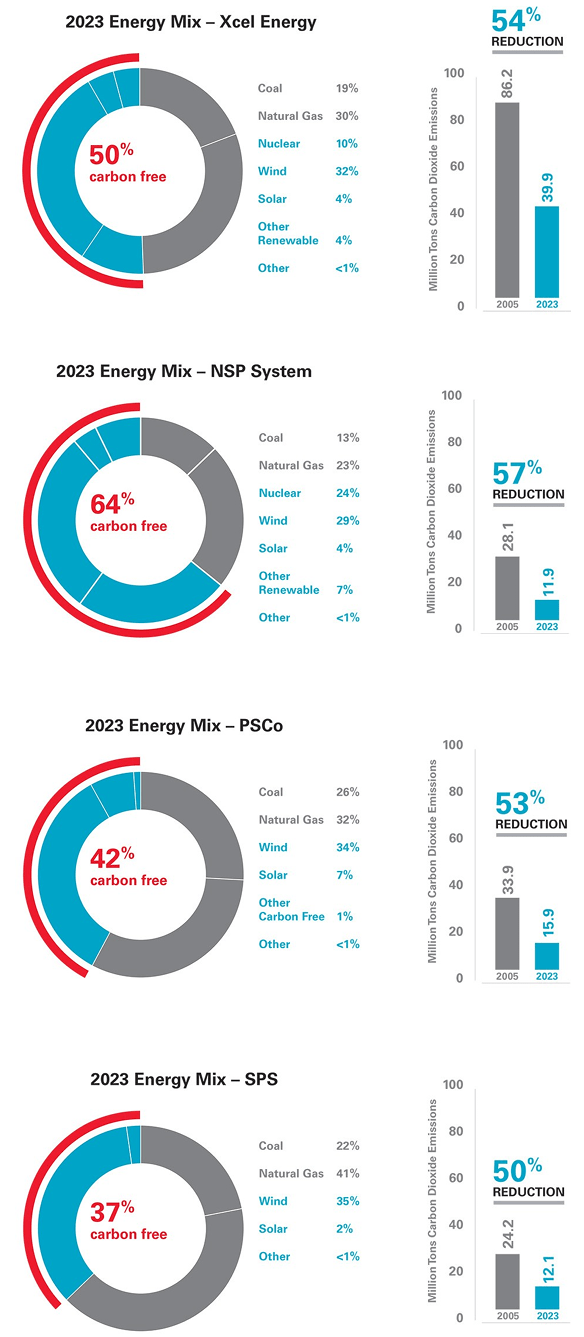

The past 16-17 years’ efforts resulted in over 50% carbon reduction during this period for Xcel and its subsidiaries. They have at least 37% and up to 64% of its energy mix is from clean energy sources. It has another 17 years to achieve its goal of 100% carbon free, but 80% of it will be achieved by 2030. Obviously, it will need a faster speed compared to the past 17 years to achieve that. Xcel currently has over 11,000 MW of wind capacity, and its solar is at a much smaller capacity. It plans to add 3650 MW of solar and wind combined in Colorado by 2028, and 5,000 to 10,000 new generation of solar and wind in SPS and 3,600 MW in NSP by 2030. In addition, it has approval of 700 MW of new solar at its Sherco facility in Minnesota. Tally up, will 17,950 to 22,950 MW of new solar and wind by 2030, more than doubling of what it has currently. The foundation seemed to have been laid for the to accelerate the transition.

xel (xel)

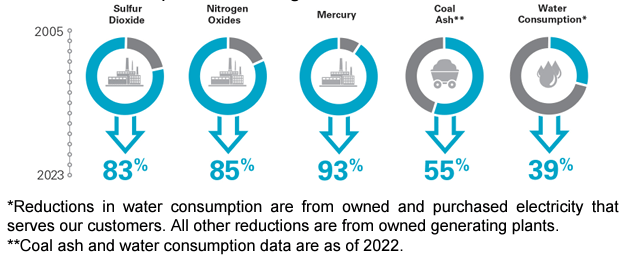

Xcel also has greatly reduced other emissions’ impact environmentally. From economic point of view, these are the reduced inputs that it has to pay for during energy generation implying improved efficiency, a win-win outcome.

xel (xel)

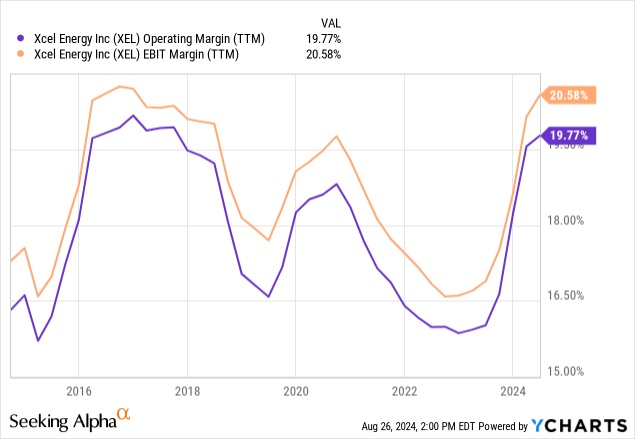

Xcel’s energy cost is included in its operating expenses, so its operating margin is representative of the overall efficiency of its income. Improving cost and expenses to its income only started in 2023, but it’s a trend that could expect to last due to the groundwork that has been done to improve efficiency from initiatives such as coal plant retirements, zero emission natural gas transportation and other cost reduction implementations. The declining revenue hasn’t dented the earnings, so in turn, even just keeping its earnings at a similar level is benefiting the net margin and EBITDA margin due to lower denominator in the factor.

Supposedly, one can say “with great resources, it comes with great responsibility”. The high natural solar power in Colorado and Texas also increasingly fanned wildfire in the region. For this year alone, Xcel is facing with north of $3 billion lawsuit for wildfire liabilities. It is inevitably that the company will need to take more pre-emptive measures to control the cost and risks. It filed a $1.9 billion Wildfire Mitigation Plan with the Colorado Public Utilities Commission, which could see the local residents’ bill rate increased by 9.56$ or $8.88 per month.

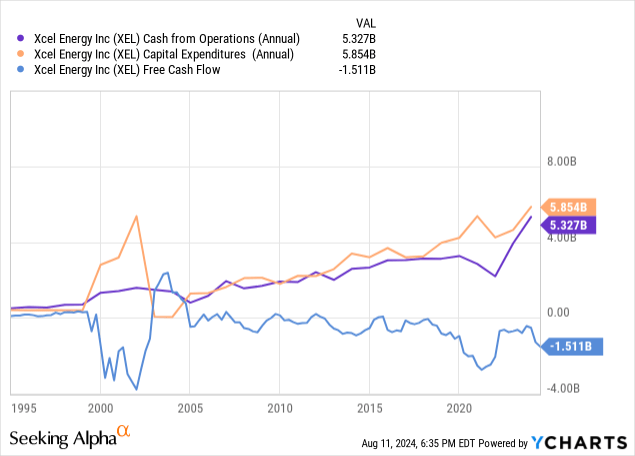

Xcel Energy has a free cash flow problem that seemed to be getting better over a year ago, but now back to a trench. From 2018-2021, not only its operating cash flow was declining, its CapEx spending was significantly ramped up. As a result, the free cash flow was pushed to its lowest level since 2002. But about a year ago, its operating cash flow started to pick up and the free cash flow seemed to be catching a break, until falling fast again since early this year. This period is what we discussed earlier the clean energy investment period started about 16 years ago, and the CapEx spending pattern will continue at least until 2030 due to its zero carbon goal of 80% reduction by 2030. In addition, if the wildfire spending plan goes through, it will add to the CapEx spending as well. Xcel’s free cash flow pressure may not be eased any time soon. The only way to ease the pressure is to work with local governments to lay out the task at hand and plan ahead, including capital and infrastructure support, in order to make the necessary changes to mitigate the risks.

Clean energy has provided Xcel with a lower cost energy source, and in turn, it was able to cut down the bill for its customers. Moreover, the lower emission initiatives have improved its efficiency in expenses and costs overall. But the work is not done. The company will need to keep up the CapEx spending to reach its goal of 80% reduction by 2030 and beyond. And frankly, to upgrade a lot of aging infrastructure related to wildfire mitigation has only started and with a long way to go. It is on the right path with natural advantage. The truth is there is no other way that is more efficient and workable than the one it is taking currently in order to maintain a long-term growth without raising the bill.

Financial Overview & Valuation

xel (xel)

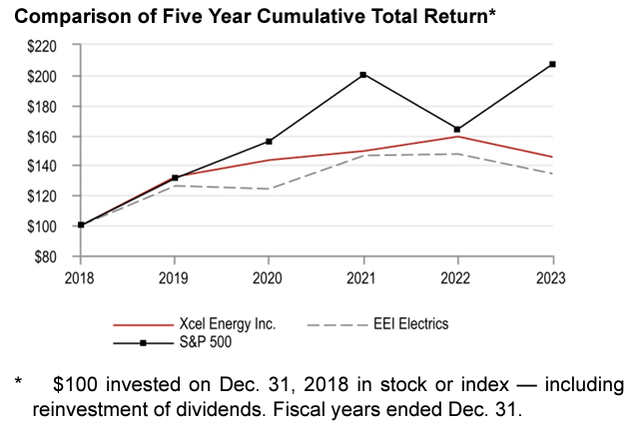

Xcel Energy’s stock price has fallen recently, receding the highs around $76 it reached in August 2022 by almost 20%. The company’s stock has been trailing the broader market in total return but has been leading its peers of EEI Electrics in the past five years. This is not surprising since the broader market is much more dominated by the tech stocks, and utilities are not expected to outrun the broader market during a bull run. It did, however, provide resiliency when the S&P 500 fell in 2022. Its stock’s five-year total return of almost 40% doesn’t hurt either. Although its total return has dipped since 2022, it is still about 10% higher than in 2019.

xel (xel)

Conclusion

Xcel has strong growth following its strategic initiatives that focus on serving the local community, customers while taking advantage of its natural resources. It is on a right path, and perhaps the only path that could deliver long-term growth, to achieve its zero-carbon emission goal by 2050. We think its free cash flow could still be under pressure for the next year or so, but it is already reaping the benefits of its infrastructure build-up in the past decades or so. Depending on an investor’s portfolio construction, Xcel Energy could provide a cushion to broader market volatility while providing a steady return. We recommend a buy at this level for a long-term holding.

Read the full article here

")

")