")

")

")

")

")

Investment summary

My recommendation for Tapestry, Inc. (NYSE:TPR) is a hold rating. Given the uncertainties and visible overhangs around the stock, I expect the share price and valuation to be range-bound in the near term. While there have been some positive developments so far, there are still a lot of grounds for management to cover and show growth recovery before I am convinced that revenue is set to accelerate.

Business Overview

TPR is a designer and retailer of handbags, footwear, and accessories, and the key brands that it owns in its portfolio include Coach, Kate Spade, and Stuart Weitzman. By revenue, Coach is the largest revenue-contributing brand (76% of FY24 revenue), followed by Kate Spade (20%), and Stuart Weitzman (4%). Geography-wise, North America is TPR’s primary source of revenue (65%), followed by Greater China (15%), Other Asia (14%), and the rest of the world at 7%.

4Q24 results update

Released on 15th August, TPR revenue fell by 1.8% y/y on a reported basis but flat on a constant currency [CC] basis. Overall growth was dragged down by TPR’s direct-to-consumer [DTC] business, which was down by 2% y/y due to weakness in North America and Greater China. On the other hand, wholesale revenue saw solid growth of 14% y/y driven by strength in Europe and other parts of Asia. Splitting the performance by brand:

- Coach revenue was flattish on a reported basis but up 2% CC, driven by continued demand momentum and AUR (average unit revenue) growth;

- Kate Spade revenues fell by 6.3% on a reported basis and 5% CC;

- Stuart Weitzman was the worst performer, with a reported revenue decline of 19.2% (19% CC) due to weakness in North America and Greater China.

Despite the mediocre top-line performance, the highlight was TPR’s profitability. 4Q24 gross margin expanded significantly by ~250bps y/y, driven by operational efficiencies, freight cost tailwinds, and an easier FX environment. That said, because SG&A is growing by 3.3% y/y, it offsets the gross margin outperformance, resulting in an adj. EPS decline of ~3%.

Still cautious on revenue growth outlook

My overall take on the TPR topline performance outlook is a cautious one. As I discussed further below, I appreciate the strategic steps and pockets of momentum seen, but I don’t think these are sufficient to convince the market that growth will accelerate from here.

The immediate overhang on growth is the uncertain macro environment, which is putting pressure on discretionary spending. While management did try to make it sound positive in the call (refer to quote below), I believe the underlying message is the same, in that consumers are pulling back on their spending.

As we look at the consumer, we’re seeing consistency from what we’ve seen really in the last few quarters, and that’s a consumer that’s choiceful. 4Q24 earnings transcript

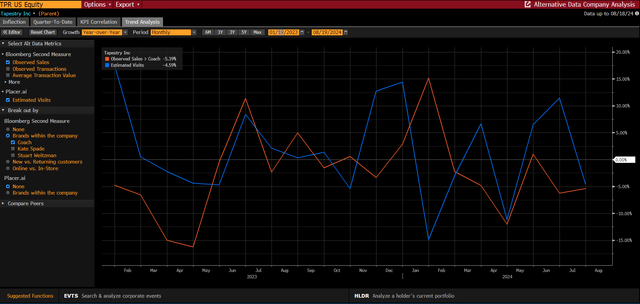

In order to “work around” this macro pressure, the key weapon that management chose to employ is innovating products that resonate with consumers. To be fair, this seems to be working for the Coach brand. As I stated above, Coach revenue grew 2% CC, which was in line with 3Q24, suggesting some form of stabilization (in a negative spending environment). Importantly, the growth was supported by incremental innovation, and management is seeing positive results from introducing select full-price products into 100 outlet locations. For the former, management efforts to pivot the brand to acquire a younger-generation crowd appear to be working very well, as they acquired over 1 million new customers in 4Q24, of which 60% were Millennials and Gen-Z. This is a solid development, as the younger generation consumer cohort is going to represent the largest mix of the US population. As for the latter point, it is important because it implies consumers are willing to pay more.

Bloomberg

Bloomberg

All of the above are very positive at face value, but I prefer to see more proof that these actions are being converted to growth acceleration. So far, based on Bloomberg’s alternative data measures, July sales seem to have softened, indicating that the strength from 4Q24 has not persisted into 1Q25. For reference, Bloomberg’s data has historically been quite accurate, so I would take this as a good indication of August’s performance so far.

Bloomberg

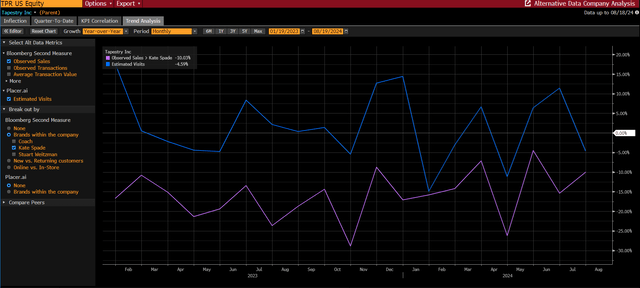

As for the Kate Spade brand, the performance has been horrible, and the hope here is that the new CEO (Eva Erdmann) can turn the tables around. On the positive side of things, the new CEO has a ton of experience handling major brands like Urban Decay, Lancome France, Yves Saint Laurent Beaute, and Christion Dior. The negative side of things (my worry) is that she appears to lack experience when it comes to handbags, which is what Kate Spade is known for. Given that she is still new to the role, I believe investors will continue to hold a cautious stance on how things will develop from here. Moreover, based on Bloomberg’s data, sales performance is still down by a sizeable percentage, so I think there are a lot of grounds for Eva to catch up.

Update on the CPRI acquisition

I believe another overhang on the stock is the Capri Holdings (CPRI) acquisition. My overall take from the 4Q24 update is a negative one, as it sends an even more uncertain outlook on synergies.

In the call, management mentioned that they are confident that the acquisition is an “exceptional strategic fit,” and they reiterated the guide that CPRI will be EPS accretive in year 1. However, I am starting to wonder if this is going to work out as well as management expects, given that CPRI FY24 results were absolutely horrible—EBIT margins were down ~620 bps y/y despite an 8% revenue decline, and this drove a substantial decline in FCF from historical levels of >$500 million to just $120 million. This suggests that there are a lot of things to be fixed, and given the internal problems TPR is facing with Kate Spade and Stuart Weitzman, I am unsure if TPR can execute well enough to reap all the expected synergies. I also point out to readers that management has subtly guided down their synergies expectations for year 1, as they previously noted “double-digit” EPS accretion vs. the current “EPS accretion in year 1.”

It’s important to highlight that we still expect Capri to generate double-digit EPS accretion on an adjusted basis and compelling ROIC. 1Q24 earnings transcript

“To this end, it’s important to highlight that we continue to expect Capri to generate double-digit EPS accretion on an adjusted basis and compelling ROIC.” 2Q24 earnings transcript

‘We believe the transaction will enhance our strong organic growth and TSR potential supported by double-digit EPS accretion on an adjusted basis, enhanced cash flow, more than $200 million of cost synergies, and compelling ROIC, accelerating benefits for our consumers, employees, partners, and shareholders for years to come.” 3Q24 earnings transcript

“Importantly, we expect EPS accretion on an adjusted basis in year one, enhanced cash flow, compelling ROIC and are firmly committed to achieving our stated leverage target in 24 months post-close.” 4Q24 earnings transcript

Valuation

My best guess on how the stock price and valuation will trend over the near term is range-bound.

From a historical perspective, TPR is trading at the bottom end of its trading range (9x to 17x) at 9x forward PE today, and I think this is fair given there are simply too many uncertainties and overhangs that make it hard to forecast with confidence how the business will perform.

From a relative perspective, compared to peers such as Prada S.P.A. (OTCPK:PRDSY), Levi Strauss & Co. (LEVI), Gildan Activewear (GIL), Hugo Boss (OTCPK:BOSSY), and PVH Corp. (PVH), I would think that TPR is trading at where it should be, given the low-single-digit growth outlook. For better reference, the average growth from these peers is expected to be in the mid-single digits, and they trade at an average of 12x forward PE. Given TPR’s low-single-digit growth outlook, which is similar to PVH Corp.’s (trades at ~9x), it makes sense for TPR to trade at where it is today (9x).

Conclusion

My view for TPR is a hold rating as 4Q24 performance is mixed, reflecting the ongoing macro challenges and uncertainties. While TPR has demonstrated resilience and made efforts to innovate and improve the fundamentals, I still think the near-term outlook remains uncertain. Given the visible overhangs and potential headwinds, I believe the stock’s valuation is likely to remain range-bound.

Read the full article here

")

")

")

")