")

")

")

")

")

Nearly two years ago, in October 2022, I wrote a bullish article about a waste management firm by the name of Republic Services, Inc. (NYSE:RSG). With a market capitalization as of this writing of $64.78 billion, the company is a behemoth in its market. Large companies in mature industries are often viewed in a negative or neutral light. This is because the perception is that upside for them is probably limited relative to what the broader market could achieve. At that time, I acknowledged that shares of the business were not value plays. Even so, for how high quality the business was, I believed that additional meaningful upside was on the table.

The decision to rate the company a ‘buy’ ended up being a good one. Since then, shares are up 59.2%. That’s comfortably higher than the 45.5% return achieved by the S&P 500 over the same window of time. The company has been lifted up thanks to strong revenue, profit, and cash flow growth. And even though shares have risen materially, they are trading at multiples that aren’t much different from back then. Given this, not to mention how shares are valued relative to comparable businesses, I do think that enough additional upside is on the table to keep the firm rated a ‘buy’ for now.

Trash is profitable

Republic Services

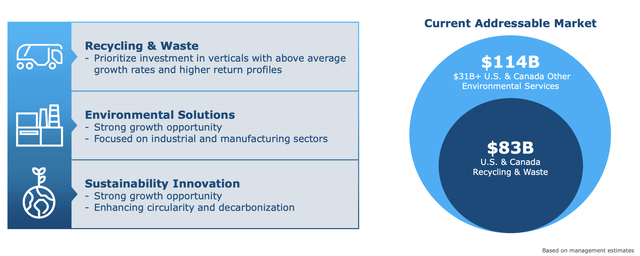

There’s a very good chance that you already know a decent amount about Republic Services. Even if you have not heard about the company’s stock, there is a good chance that you are one of its customers, or you know somebody who is. At the end of its 2023 fiscal year, the business had 364 collection operations, 246 transfer stations, 74 recycling centers, 207 active landfills, three treatment, recovery, and disposal facilities, 22 treatment, storage, and disposal facilities, 6 saltwater disposal wells, 12 deep injection wells, and a single polymer center. These are all located throughout the US and Canada. And it places the enterprise as a major leader in the $114 billion North American environmental services market.

Author – SEC EDGAR Data

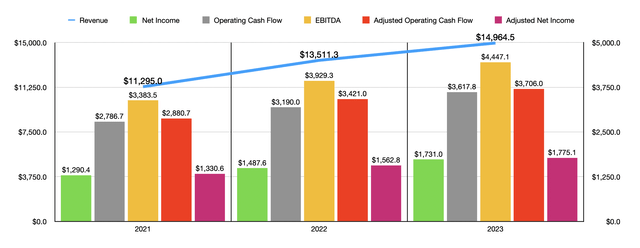

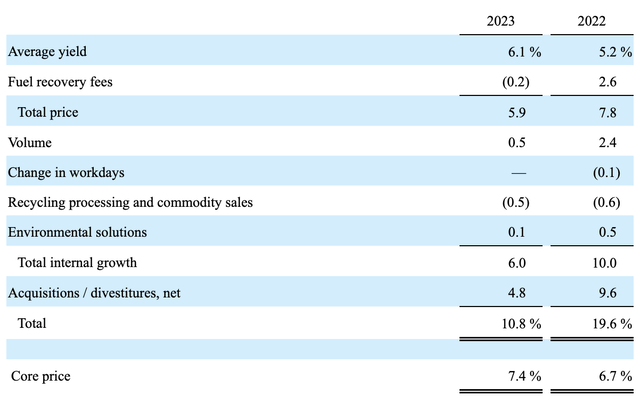

Even though this is a pretty mature market, it is one that is constantly growing with the population. That has reflected well in the firm’s top line results. Consider the past three fiscal years as an example. Between 2021 and 2023, revenue grew from $11.30 billion to $14.96 billion. From 2022 alone, revenue growth was an impressive 10.8%. Only a small portion of this growth was driven by increased volume. From 2021 to 2022, the company benefited from a 2.4% rise in volume. But last year, that growth was a more modest 0.5%. Total price increases have been far more significant. From 2021 to 2022, higher pricing contributed 7.8% to the firm’s top line. And from 2022 to 2023, the contribution was 5.9%.

Republic Services

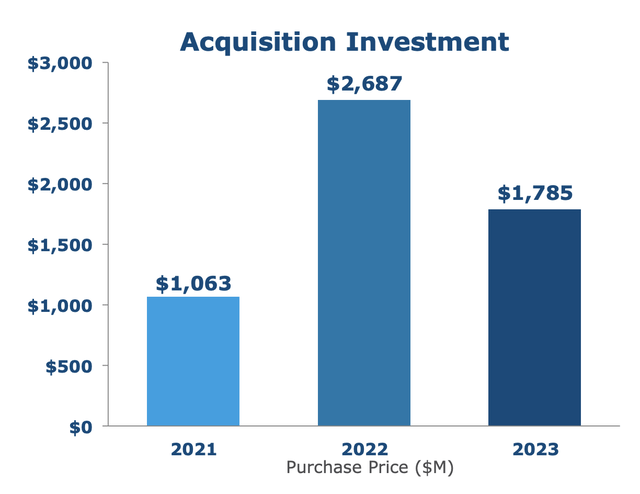

Even with these impressive results, we don’t get the kind of growth the company has achieved. There were some other smaller factors at play. But what really did the heavy lifting, in addition to pricing, has been acquisitions. In 2021, the business allocated $1.06 billion toward acquisitions. This was dwarfed by the $2.69 billion allocated toward them in 2022. And then, last year, the company allocated another $1.79 billion toward purchases. These activities have had a positive impact on the firm, pushing sales up by 9.6% in 2022, followed by another 4.8% last year.

Republic Services

On the bottom line, growth has also been very strong. From 2021 to 2023, net income for the business jumped from $1.29 billion to $1.73 billion. Other profitability metrics followed a very similar path. Adjusted net income expanded from $1.33 billion to $1.78 billion. Operating cash flow grew from $2.79 billion to $3.62 billion. If we adjust for changes in working capital, the rise was from $2.88 billion to $3.71 billion. And finally, EBITDA for the business shot up from $3.38 billion to $4.45 billion.

Author – SEC EDGAR Data

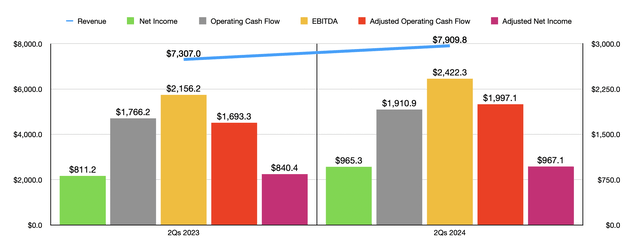

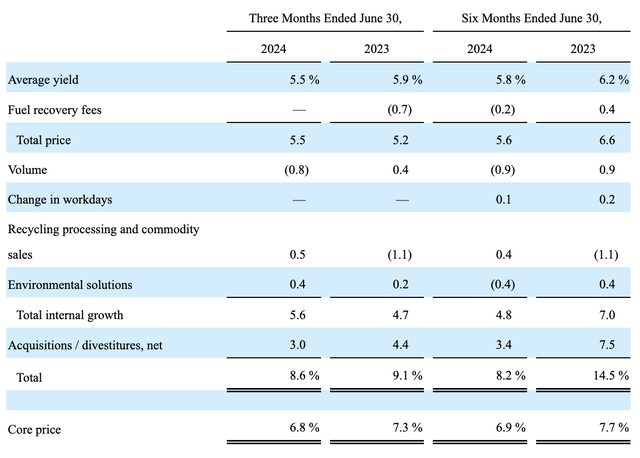

It’s not difficult to imagine growth continuing into the current fiscal year. And that is exactly what we saw. Total price increases for the first six months of this year added 5.6% to the firm’s top line growth. In this case, volume actually did decline, dipping by 0.9% because of a drop in large container collection revenue resulting from a decline in construction-related activities, and because the firm lost certain municipal contracts under the residential and small container lines of business. Acquisitions added another 3.4% to the firm’s top line year over year. All of this, combined, allowed revenue to jump from $7.31 billion last year to $7.91 billion this year.

Republic Services

As was the case for the last three fiscal years, profits and cash flows followed revenue higher. Net income for the business jumped from $811.2 million to $965.3 million, while adjusting net income expanded from $840.4 million to $967.1 million. Operating cash flow grew from $1.77 billion to $1.91 billion. On an adjusted basis, it expanded from $1.69 billion to just under $2 billion. And finally, EBITDA grew from $2.16 billion to $2.42 billion.

Republic Services

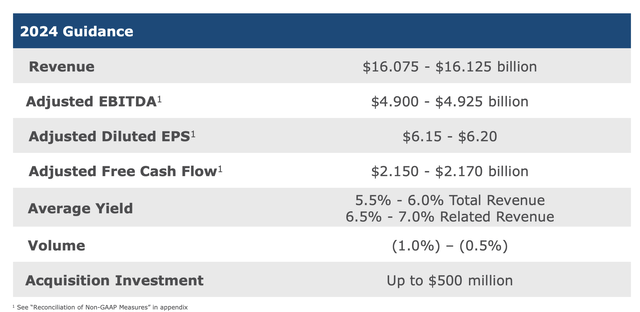

When it comes to the 2024 fiscal year in its entirety, management has provided some promising guidance. They expect revenue to come in at between $16.075 billion and $16.125 billion. Year over year, that would translate to an increase of 7.6%. They anticipate adjusted earnings per share of about $6.15 to $6.20. At the midpoint, that would be $1.95 billion. And they also see EBITDA coming in at between $4.90 billion and $4.925 billion. If we assume a similar growth rate when it comes to adjusted operating cash flow, we would expect a reading this year of $4.06 billion.

Author – SEC EDGAR Data

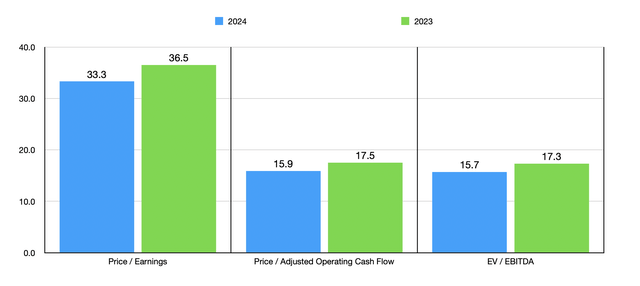

Using these estimates, as well as historical results from 2023, we can see how shares of the business are valued in the chart above. Relative to earnings, I would say that shares are quite pricey. But when it comes to the other profitability metrics, this is the range that I would typically consider to be fairly valued. However, considering the strong growth rate the company has seen in recent years, not to mention the quality and stability of the operations, I think a little leeway in valuation is appropriate.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Republic Services | 33.3 | 15.9 | 15.7 |

| Waste Management, Inc. (WM) | 33.4 | 16.4 | 17.0 |

| Waste Connections, Inc. (WCN) | 55.8 | 21.8 | 22.7 |

| GFL Environmental Inc. (GFL) | 1,194.8 | 19.1 | 25.3 |

Paying a premium for a high-quality business is never a bad idea so long as the premium is not all that high. And what’s really great about this is that, relative to similar firms, shares are actually trading at a discount. In the table above, you can see how the stock is priced against three similar enterprises. Using each of the three valuation metrics, I calculated that Republic Services is actually the cheapest across the board.

Author – SEC EDGAR Data

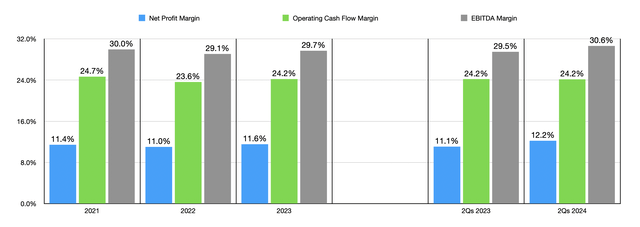

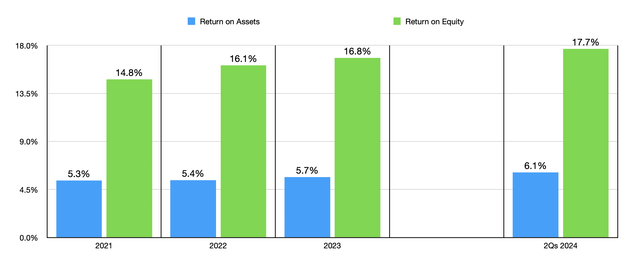

Valuation aside, there are some other data points that I think justify a ‘buy’ rating for the business. For starters, management has done exceptionally well in recent years maintaining profit margins. In the chart above, you can see the net profit margin, the operating cash flow margin, and the EBITDA margin of the business for the 2021 through 2023 fiscal years, as well as for the first half of this year compared to the first half of last year. Margins have been remarkably consistent. At the same time, as the chart below illustrates, the firm has actually seen some expansion when it comes to other important metrics. Over the last three years, the business has grown its return on assets and its return on equity. This shows that management is getting even better at extracting value from the assets and net assets of the enterprise.

Author – SEC EDGAR Data

Back when I was in college, which was over a decade ago, the conventional value investing wisdom was that a company with a return on equity of 20% or more often represented a stellar prospect. And while Republic Services isn’t there just yet, it is approaching that territory. In the chart above, you can see how the return on assets and return on equity of our candidates stack up against the same three companies that I compared it to. In both cases, it is superior to two of the three firms. The clear winner in this space is Waste Management, which I have also been bullish on.

Author – SEC EDGAR Data

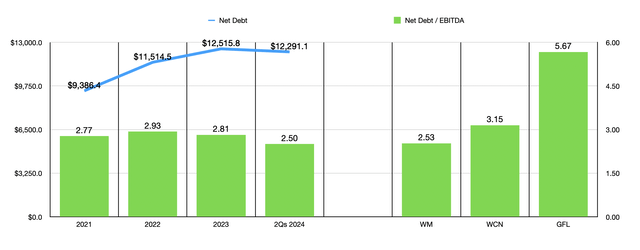

Another important thing to take into consideration is overall capital management. I already stated earlier in this article that the company has a track record of making meaningful acquisitions. This can result in increased leverage that can make a company riskier. The good news is that this doesn’t appear to be the case. The net leverage ratio of the company did grow from 2.77 in 2021 to 2.93 in 2022. But since then, leverage has been on the decline. If we use the most recent net debt figures and the midpoint of guidance expected for EBITDA for this year, Republic Services has a net leverage ratio of 2.50. As you can see in the chart above, this is lower than what we get from looking at any of the three comparable firms discussed in this article.

Author – SEC EDGAR Data

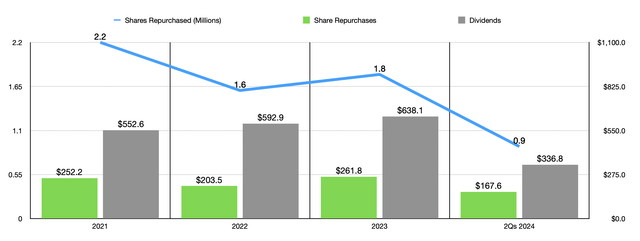

Speaking of capital management, management has achieved this debt reduction and its impressive growth record while simultaneously rewarding shareholders. Over the last three completed fiscal years, the firm has repurchased 5.6 million shares for a combined $717.5 million. This is in addition to allocating $1.79 billion toward dividends. For the first six months of this year, the company repurchased another 0.9 million shares for $167.6 million. They achieved this while also putting $336.8 million toward dividends. In all likelihood, this trend will continue for the foreseeable future.

Republic Services

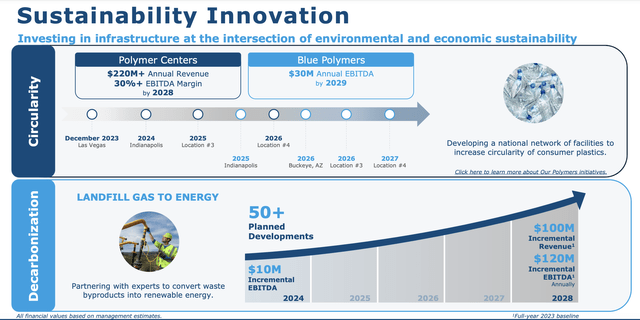

One last thing that I would like to touch on is the fact that, even though this is, in general, a mature space, there are growth opportunities that management is focused on. It is especially interested in expanding its environmental solutions operations. And some of this investment is focused on sustainable innovation. As an example, the company hopes to grow its polymer centers operations to more than $220 million in revenue and to more than $66 million of EBITDA by 2028. When it comes to Blue Polymers alone, it expects to achieve $30 million worth of EBITDA annually by 2029. The company is also investing heavily in decarbonization activities. Its landfill gas-to-energy strategy should generate $10 million worth of incremental EBITDA this year. But with more than 50 different developments planned over the next few years, the company hopes to grow this substantially by 2028, achieving $120 million worth of incremental EBITDA by that time.

Takeaway

All things considered, I would classify Republic Services as a high quality business. It’s certainly not a value prospect. But the premium for the quality received is, in my view, quite small. It is a solid firm that is achieving attractive growth, improvements in asset quality, and reduced leverage, all while continuing to allocate ever larger payments back to shareholders. Add all of this together, and I have no problem keeping the company rated a ‘buy’ for now.

Read the full article here

")

")

")

")