")

")

")

")

Portfolios based on quality measures remain a compelling investment thesis, as the macroeconomic outlook pointing to a slowdown warrants a more cautious approach. The Virtus Terranova U.S. Quality Momentum ETF (NYSEARCA:JOET) is among the funds offering exposure to high-quality companies, but with an additional tilt toward those stocks showing persistence in their performance.

This fund has struggled to keep up with the S&P 500 index and other ETFs that use quality as a core investment approach. In my view, this is primarily due to its equal-weighted allocation, which has resulted in underweight exposure to a few profitable, high-quality mega caps compared to the broader benchmark indexes and other quality ETFs.

Meanwhile, a shift in market sentiment favoring smaller capitalization companies is a real possibility, underscored by the coming easing cycle. This change is expected to benefit a fund like JOET, where a substantial portion of its holdings is comprised of mid-cap companies. Thus, investors who want to position their portfolio for this new environment may find this fund an opportunity to potentially outperform the broader market, while still investing in companies with above-average quality measures.

ETF Description & Highlights

JOET is an exchange-traded fund that aims to achieve long-term growth, investing in U.S. large-cap companies with high-quality fundamental characteristics and strong price performance.

This fund tracks the performance of the Terranova U.S. Quality Momentum index, which ranks the largest 500 U.S. companies according to momentum and quality scores. The momentum score measures each security’s tendency to show persistent relative performance based on the total return in the past twelve months. The quality score is designed to assess each company’s fundamentals according to three quality factors: return on equity, debt to equity, and sales growth rate.

The index methodology first selects the 250 securities with the highest momentum score, which are then ranked according to a composite score comprising the three quality factors. The 125 securities with the best composite score are selected for inclusion in the index, following an equal-weight allocation criteria, with quarterly reconstitution and rebalancing.

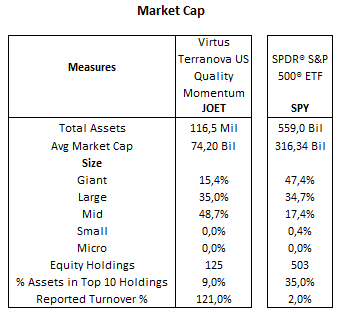

As of August 22, 2024, JOET is composed of 125 constituents, with 116 million in AUM and an average market cap of $74.22 billion. The allocation across market cap sizes is skewed to mid-caps, with nearly 49% of total assets, followed by 35% in large caps and only 15% in mega caps. This is in contrast with the market-cap weighted S&P 500 index, where mega caps represent 47%, large caps 35%, and mid-caps only 17%.

As an equal-weighted fund, JOET’s top holdings represent 9% of total assets and reflect those stocks with short-term outperformance following the last quarterly rebalance. Thus, exposures are relatively similar for each constituent, with the top holding, MercadoLibre, representing 0.93% of total assets, and other top holdings, such as Axon Enterprise, Palantir, Eli Lilly, AppLovin, Howmet Aerospace, Nu Holdings, Monolithic Power Systems, Meta Platforms and Uber, with allocations in the range of 0.88% to 0.93%.

Morningstar, consolidated by the author

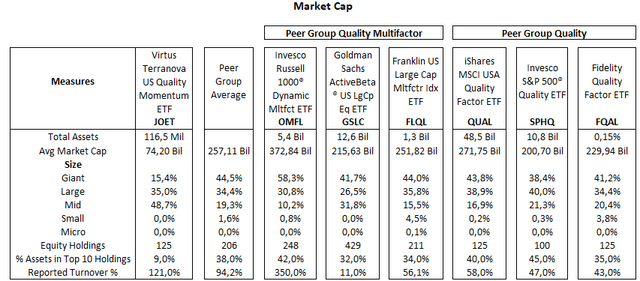

A comparison analysis for a fund like JOET is not straightforward, given an interesting but relatively unusual combination of two investment themes: quality and momentum. Therefore, a list of three multifactor ETFs was selected (OMFL, GSLC, and FLQL) in a first peer group subset, where quality and momentum are among the criteria used for selection and allocation weighting. The second subset includes three mid-large cap ETFs with an emphasis on quality that will be used as a benchmark to assess JOET’s portfolio and performance over time.

Morningstar, consolidated by the author

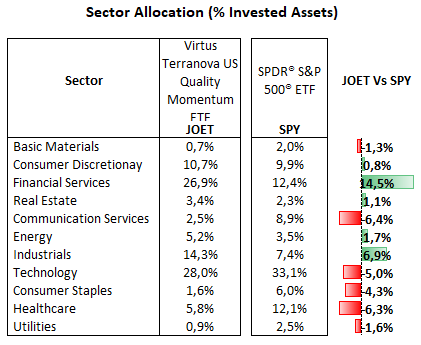

From a sector allocation perspective, JOET’s largest allocation is to the technology sector, with 28.0% of total equities, followed by financial services with 26.9%, industrials with 14.3%, consumer discretionary with 10.7%, healthcare with 5.8%, energy with 5.2%, real estate with 3.4%, communication services with 2.5%, utilities with 0.9%, consumer staples with 1.6%, and basic materials with 0.7%.

Compared to the S&P 500 index, represented in this analysis by the SPDR S&P 500 ETF (SPY), JOET has higher allocations to financial services (+14.5%) and industrials (+6.9%). The overweight allocation to financial services is due to its many holdings in property & casualty Insurance, consumer finance, and regional banks. Meanwhile, JOET has a selective approach to larger financial institutions. For instance, the fund has an allocation to JPMorgan but holds no shares in Bank of America, Wells Fargo, Goldman Sachs, and Citigroup. On the other hand, JOET’s positions in the industrial sector are relatively diversified across several areas, including construction, machinery, and aerospace & defense, but with no holdings in air freight & logistics, airlines, and some larger companies, such as GE, Union Pacific, and Honeywell.

Meanwhile, JOET is underweight in communication services (-6.4%), healthcare (-6.3%), technology (-5%), and consumer staples (-4.3%), driven by smaller positions in Alphabet, Meta, Apple, due to its equal-weighted composition, and selective approach to pharma, biotechnology industries and consumer staples in general.

Morningstar, consolidated by the author

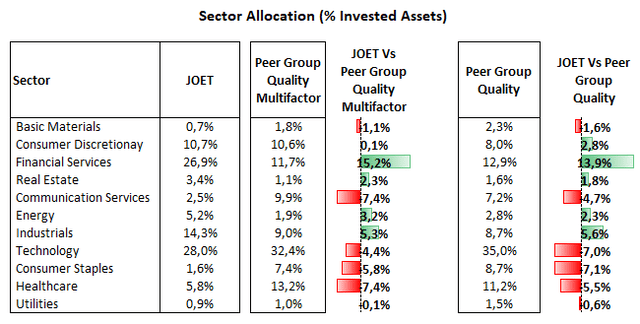

A comparison with quality multifactor ETFs and quality ETF peers shows a similar pattern, as JOET is also overweight in financial services and industrials, but underweight in communication services, healthcare, technology, and consumer staples.

Morningstar, consolidated by the author

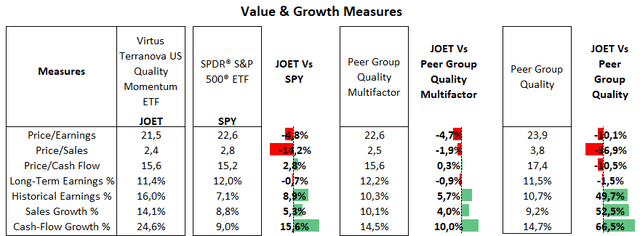

Profitability and Valuation Highlights

Looking at JOET’s holdings, it is noticeable a portfolio skewed toward high-margin industries, such as consumer finance, software, semiconductors, and away from segments like biotechnology, life sciences, where operations are generally in early stages, and struggling areas like air freight & logistics.

On the flip side, its equal-weighting allocation ends up leaving a small exposure to large and high-profit names, such as Microsoft, Apple, Nvidia, Alphabet, and Meta Platform, which combined represent nearly 26% of the S&P 500 index, but account for only 4% of JOET’s invested capital. The combination of these two elements leads to average profitability measures for the whole fund, such as EBITDA margin and return on equity, nearly ten percentage points below those of the S&P 500 index, according to my estimations.

Meanwhile, JOET’s price/earnings ratio of 21.5x is slightly lower compared to benchmarks, such as the S&P 500 index (22.6x) and both peer groups (22.6x for quality multifactor ETFs and 23.0x for quality ETFs). This is also driven by JOET’s smaller allocation to mega caps, which generally trade at premium price/earnings ratios, such as Microsoft (32.2x), Apple (33.8x), Nvidia (46.6x), Amazon (37.9x).

Morningstar, consolidated by the author

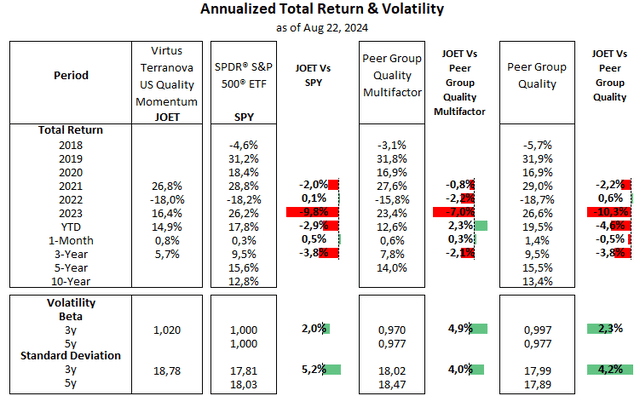

Underperformance In Sub-optimal Market Conditions For This Fund

JOET’s performance has generally been positive since its inception in late 2020, with annualized 5.7% returns over the past three years. However, this has not been enough to keep pace with the S&P 500 and other quality-focused ETFs. To be sure, both peer groups in this analysis are composed of funds primarily constituted by large and mega caps, as evidenced by their average market cap of $257 billion, while JOET’s market cap isa much lower $74 billion. This has caused funds with heavier exposure to smaller capitalization companies like JOET to struggle to compete with these larger cap ETFs during a market environment that has favored mega caps over other categories.

Morningstar, consolidated by the author

That said, while an equal-weighting approach is expected to reduce concentration risk and offer broader exposure to the equity market, it has also prevented a more targeted emphasis on best-performing, high-quality names like Microsoft, Nvidia, Apple, Meta, Visa, among others that are usually top holdings in so-called quality and multifactor ETFs. Therefore, it is fair to say this allocation profile has not been a clear advantage for this fund, at least in the recent past.

Looking ahead, I still believe that much of the earnings growth in the equity market should come from those large companies. Thus, I take a neutral stance on JOET at this time, as I find it would be unlikely that a fund with quite limited exposure to these companies could outperform the broader market in the foreseeable future.

In the longer term, as the economy reaccelerates again, underscored by lower rates and a healthy labor market, we will probably see a more constructive outlook for smaller capitalization companies and a much better setup for funds using strategies like JOET.

Read the full article here

")

")

")

")