")

")

")

The following segment was excerpted from this fund letter.

Truxton Corp. (OTCPK:TRUX) is our tenth largest position. The company has a market cap of $180m and is a community bank located in Nashville, Tennessee.

When I was travelling throughout the southeastern U.S. a few years ago for due diligence on the community banks River Oaks Capital was buying ownership in (Citizens Bank, BankFirst, and M&F Bank), I kept hearing from experts in the community banking industry about the outstanding reputation of Truxton Bank.

Although I was sure their reputation was indeed stellar, I kept brushing it aside as I couldn’t get over the fact that Truxton was being valued at ~2x book value when the community banks we were buying ownership in were valued at ~0.5x book value.

Then earlier this year, I decided to finally reach out to Truxton’s management team to figure out why this bank had such an incredible reputation.

After a quick Zoom call with their CFO – Austin Branstetter – it started to click why they were so exceptional and I quickly got on a plane and headed to Nashville to meet the whole team.

As I sat down with CEO Tom Stumb, CFO Austin Branstetter and Vice Chairman Andy May, I realized what I had been missing about Truxton each time I glanced at their financials and filings over the years.

Truxton isn’t a bank – Truxton is a wealth management firm for high-net-worth individuals with a bank attached to it.

Truxton provides a one-stop shop for wealthy business owners – with a net worth between $25-$50m – and their families who are looking for: strategic wealth and tax planning, investment management, fiduciary assistance, as well as banking and capital advisory services.

Their CEO Tom Stumb put it best to me “we operate essentially as a multi-family office for 250+ families.”

Tom explained to me in detail how Truxton was started in 2004 when the late Don Thurmond alongside Tom, Andy, and a few other veteran wealth advisors – who are still on the board today – left the major US banks to start their own bank and wealth management firm.

Their goal was to run their company very differently than the banks from which they had come.

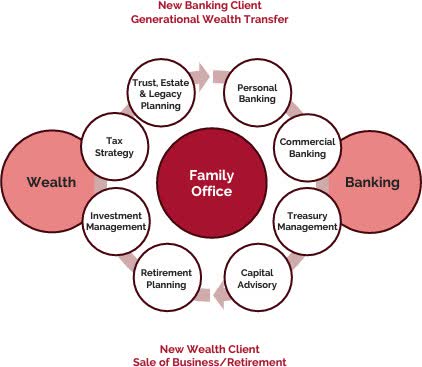

Tom explained to me that when the founding members worked as high-net-worth wealth advisors they recognized numerous glaring customer needs that were going unaddressed. In the chart below, Tom and his team illustrate the problem that was occurring for high-net-worth individuals and the simplified solution Truxton Bank provides for their customers.

At the major banks, each white circled service (tax strategy, trust, estate & legacy planning, personal banking, etc.) is individually “siloed” within various departments.

Which means at a major bank you can have one advisor for each of the white circled services – potentially up to 8+ advisors – that often do not even talk to each other.

Outside of their numerous advisors at major banks, high-net-worth individuals also often have to pay an accountant, lawyer, insurance agent and broker.

To make matters even worse, at the major banks the turnover rate of wealth advisors is extremely high.

So, by the time the high-net-worth individual has gotten to know one of their wealth advisors, they have often left for another job.

These are all the direct issues that Truxton has addressed.

Truxton hires extremely qualified and well-rounded wealth advisors alongside in-house CPAs and trust experts so that every white circle in the chart above can be handled for their clients by only one person.

Furthermore, many of the wealth advisors hired by Truxton in 2004 are still with them today, allowing them to develop a personalized relationship with each of their clients.

However, Truxton’s basic niche is simplifying the financial lives of business owners who are worth in the $25m-$50m range – especially those with estate and tax planning needs

(Tennessee is an advantageous state to have a trust as there are a lot of structuring levers you can pull for tax advantages).

As Tom summed up for me, “We don’t compete in the high volume, low margin side of wealth management, we partner with families that are serious about their money and appreciate a personalized relationship with an experienced person who will give them good advice”

In total, the clients who come to Truxton’s wealth management are simply tired of the headaches of high turnover at major US banks, the countless advisors needed to manage their money and the additional accountants, lawyers, insurance agents and brokers they pay an hourly rate to.

As Truxton’s tag line to a prospective client goes “why is it that you are the only person worried about your money?”

For their all-encompassing wealth management services, Truxton charges their clients a ~1% fee on their assets under management (“AUM”).

They currently have ~$2 billion in AUM amongst ~250 families – mostly business owners located either close to Nashville or with some connection to Nashville.

It’s evident their new approach to wealth management is working as very few customers have left Truxton’s wealth management once they have started using their services.

In fact, the original founder – Don Thurmond – and any other Truxton employees who use Truxton’s wealth management services pay the same fee as any of their other clients.

As Tom said to me ” If we aren’t willing to pay our rates, then why would anyone else be willing to pay our rates?”

Although the wealth management side of the Truxton business is the “wonderful” part of their “wonderful business,” their bank in itself is quite impressive.

Most notable, since starting the bank 20 years ago, they have never written off a single loan!

This partially may be because they lend to high-net-worth individuals in Nashville – a city that has been rapidly growing for the past 10-15 years with real estate values doubling in the past 6-7 years – but nonetheless it is a testament to how conservative their underwriting is (especially considering those 20 years include the 08-09 financial crisis).

Truxton Bank is exceptionally unique in that it only has one branch with a massive $800+m in deposits – some community banks only have $30m-$50m per branch.

This keeps their fixed costs on the banking side very low which is demonstrated by their impressive ~50% efficiency ratio – which measures a bank’s ability to generate revenue above their operating expenses (50% of their net interest income and non-interest income becomes profit).

A vast majority of their banking loans are distinct types of real estate loans throughout the Nashville area. They predominately underwrite unique, conservative loans to high-net-worth individuals – ~40% residential real estate, ~30% commercial real estate, and ~30% consumer/other loans.

To better understand how conservatively Tom and his team lend out money I will paraphrase what they told me, ‘a typical banking lender would look at the current situation – alluding to the growth in the Nashville real estate market – and go out and raise another $20m of equity to do $30-$40+m in loans but we aren’t going to change the way we operate. We know a correction is coming at some point. We don’t know when but it will happen and we don’t feel comfortable lending out a ton right now.’

As our discussion furthered on, I realized Tom and his team are the type of people you would want to see in the cockpit as you’re boarding an airplane. They are conservative, cautious, practical, and able to navigate tough climates.

When trying to ascribe a fair value to Truxton the first detail that needs to be mentioned is Truxton went public in 2004 where they raised $20m from mostly employees and Nashville natives – they have not raised any equity since.

Since 2004, Truxton has returned over $15+m in dividends to their investors while growing earnings to $19-$20m per year.

Most of the current investors in Truxton are people who invested in 2004. It is a very stable, long-term minded shareholder base.

Of Truxton’s $19-$20m per year in free cash flow to equity, 50% comes from the wealth management side of the business and 50% comes from the bank.

The banking side of the business has a book value of ~$90m and generates $9-10m of free cash flow to equity – a respectable 10% return on equity.

However, you can see why investors ignore Truxton when they view it as a bank with a $90m book value trading at $180m market cap – 2x book value appears to be very high for a community bank.

Even if you look at Truxton’s market cap of $180m, $19-$20m of free cash flow to equity – a 10-11% free cash flow yield (9-10 P/E ratio) – doesn’t look overly exciting until you dig a bit further.

Once you meet Tom and his team, you realize that not only is there a wonderful business hidden within a bank but it is quite undervalued as well!

First off, if you look at Truxton’s return on equity, it has grown from ~10% a decade ago to ~20% today.

This is largely due to the growth in their wealth management business – from well under $500m AUM to $2 billion AUM – which generates 30+% returns on equity.

After getting to know management, the upside of Truxton becomes very apparent as they are laser focused on growing their high return on investment wealth management business.

Additionally, very little capital is required to grow the wealth management business, there are no regulations on how much you can grow (as there is in banking), and the revenue generated is stickier – very few customers have left Truxton’s wealth management once they have started.

The only growth constraint they are facing right now on the wealth management side is recruiting the rare wealth advisor that fits into their low turnover culture while also having an expertise in a variety of wealth management advisory roles.

Of course, the wealth management revenue to a certain degree fluctuates depending on how the stock market is doing but even if they are only able to grow free cash flow from increasing AUM by 10% per year (solely through bringing on new customers not via a change in the market value of existing AUM), Truxton will reach $30+m of free cash flow in 3-5 years – a 16+% free cash flow yield (6-7 P/E ratio).

However, as you talk with management they make it quite clear that the wealth management side of the company has the potential for growth well beyond 10% per year.

They have even recently upgraded their Nashville office to accommodate for their anticipated growth.

Additionally, their wealth management business started by just managing business owners and their family’s money within the Nashville area and has since grown by word of mouth – their high-net-worth clients go out to dinner with other high-net-worth individuals and recommend Truxton Bank.

Now, word of mouth is starting to rapidly spread to other states as they have had to open a small advisory office in Georgia and may need to open ones in Florida and Texas in the future.

Remember not only does the growing wealth management side of the business require very little capital, but it also generates 30+% returns on equity.

In 2023, Truxton returned slightly less than 50% of their free cash flow to equity to shareholders via dividends and share buybacks.

However, with Truxton Bank being so well capitalized and the bank’s lending continuing to slow down – ~5% year over year lending growth in 2023- a scenario where they distribute all of their free cash flow to equity to shareholders each year via dividends and share buybacks – 10+% yield – while continuing to consistently grow assets under management is achievable.

The future scalability of the wealth management business without any required capital is what is unappreciated about Truxton’s story!

We are very lucky to have Tom and his team – who own 33% of the bank- allocating and protecting our capital for us. River Oaks Capital plans on being owners of Truxton Bank for years to come.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")