")

")

")

I am selling my Baidu (NASDAQ:BIDU) (OTC:BAIDF) shares following the company’s Q2 earnings print. Although Baidu delivered a solid quarter during the 3 months ending June, I am increasingly doubtful about management’s ability, or willingness, to deliver shareholder value. In fact, in an analysis that I share in this research note, I highlight that Baidu is paying out (approx. $1 billion) less than 35% of its earnings to shareholders, compared to 115% for Alibaba (BABA). Moreover, considering dilutions through stock-based compensation, Baidu’s net payout to investor drops to 0. Such a non-existent payout is shocking, in my opinion, as I point to approximately $20.9 billion of cash on hand and a market cap of merely $30 billion.

I downgrade Baidu shares to “Sell”. I will maintain my bearish rating on Baidu until I see a significant change in shareholder payouts. Investors beware.

For context, Baidu stock has grossly underperformed the broad equity market in 2024, inflicting investors a YTD loss of 28% compared to a gain of 18% for the S&P 500 (SP500)

Seeking Alpha

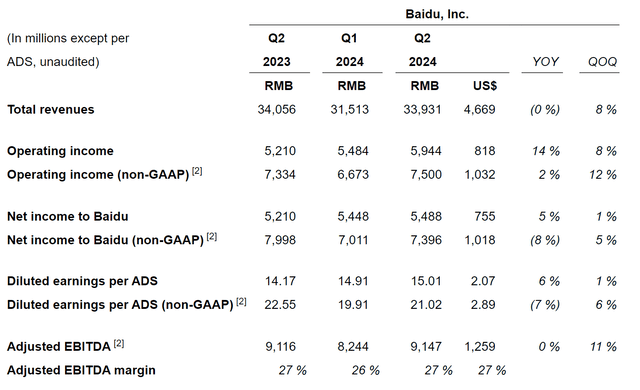

Baidu’s Q2 Results Are Solid …

Baidu reported its results for Q2 2024, delivering a performance that was broadly in line with expectations. During the period from April to June, Baidu generated total revenues of RMB 33.9 billion, remaining flat YoY, but in line with both the company’s own guidance and consensus estimates. The Baidu Core segment contributed RMB 26.7 billion in revenue, reflecting a modest 1% YoY growth, also in line with expectations. Within Baidu Core, marketing revenue declined by 2% YoY to RMB 19.2 billion, while non-marketing revenue grew by 10% YoY to RMB 7.5 billion, driven primarily by strong performance in the AI cloud sector. The performance of Baidu’s streaming subsidiary, iQIYI, was quite weak, with total revenue declining by 5% YoY to RMB 7.4 billion.

Profitability metrics were overall supportive. Notably, Baidu’s non-GAAP operating profit for the Core segment reached RMB 7.5 billion, up 8% YoY, and surpassing consensus estimate by RMB 550 million, according to data collected by Refinitv. This improvement was largely due to lower selling, general, and administrative expenses, which resulted in a non-GAAP operating margin of 26.2%, up 1.6 percentage points YoY. Overall, it is fair to say that Baidu’s cost control measures helped cushion the impact of a challenging advertising environment.

Baidu Q2 results

… But Another Payout Disappointment

In my opinion, Baidu’s Q2 solid earnings print was overshadowed by another quarter of disappointing shareholder payouts. During the period spanning April through June, Baidu returned $318 million to shareholders through repurchases. Deducting $208 million of share-based compensation expenses, the net investor payout was only $110 million. Remember, Baidu does not pay any dividends, so buybacks are all investors get. On an annualized basis, Baidu’s Q2 buyback would imply an equity yield of only about 1.3% for the year, which is well below the equity yield of Chinese and U.S. tech peers.

Notably, the argument that Baidu needs cash for growth does not appear reasonable because Baidu is barely growing. For the TTM ending June 2024, revenue was $11.2 billion vs. $10.8 billion the TTM ending June 2023 (up only 3.7% YoY).

Payout Policy Flashes A Warning Signal

To highlight Baidu’s ridiculous investor payout policy, I prepared an analysis that compares Baidu’s payouts to the company’s earnings and cash on hand: For the trailing twelve months ending June 2024, Baidu’s operating income (EBIT) was $2.9 billion, while shareholder payouts totalled $0.97 billion. This is a payout ratio of about 33%. However, considering dilutions through stock-based compensation, Baidu’s net payout to investors drops close to 0.

In my view, Baidu’s non-existent payout is inexcusable. Investors should consider that the Chinese tech giant sits on about $20.7 billion of cash, while the company’s market cap is valued at only $20 billion. At these levels, leveraging the cash on hand for buybacks would be the only reasonable option, in my opinion. The fact that Baidu is not leveraging this option should be a big warning signal to investors about management’s willingness to act in a shareholder friendly manner.

Most Chinese tech peers have stepped up their shareholder payout over the last few quarters. In fact, Alibaba’s payouts as a percentage of operating earnings are now >100%. The respective metric for JD, NetEase and Tencent is 74%, 55% and 58%.

Company Financials; Refinitiv; Author Analysis

Suspend Valuation On Fundamentals

I previously valued Baidu ADR shares at about $180. However, my mistake in valuing Baidu was based on my decision to calculate a target price based on earnings. As Baidu is not paying out earnings to shareholders, I don’t feel valuing Baidu based on earnings is adequate. Moreover, I dislike valuing Baidu based on book value, as Baidu does not show intention to distribute book value/ cash on balance sheet either. Accordingly, I suspend my valuation analysis for Baidu based on fundamentals, until Baidu shows intention to distribute value to shareholders (either based on earnings, or cash on hand). In the meantime, I propose a relative valuation framework that looks at investing in stocks that offer a higher investor payout yield — a metric where Baidu grossly underperforms Chinese and U.S. tech peers.

Investor Takeaway

I am divesting my Baidu position following the company’s Q2 earnings report. While Baidu posted a solid performance for the three months ending in June, I am growing increasingly skeptical of management’s commitment, or ability, to generate shareholder value. In this article, I point out that Baidu is returning approximately $1 billion to shareholders – less than 35% of its operating earnings – compared to Alibaba’s payout of >100%. When factoring in the dilutive impact of stock-based compensation, Baidu’s net payout to investors effectively drops to zero. This lack of meaningful shareholder returns is particularly alarming, given Baidu’s substantial cash reserves of around $20.9 billion against a market cap of just $30 billion.

I am downgrading Baidu shares to a “Sell.” I will maintain this bearish outlook until there is a significant shift in Baidu’s approach to shareholder payouts.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")