")

")

Initial Takeaways From Q2 Report: GenesisX Submissions/Approval & MAGiC Making Progress

Heading into the Q2 earnings report, I was most concerned about the GenesisX submission timeline. Stereotaxis (NYSE:STXS) management originally projected the robot would be submitted to regulators in late 2022. That guidance was way too aggressive. Then, in mid to late 2023, the firm suggested the robot was nearly ready for regulatory submission, but the company wanted to wait until the MAGiC catheter was near approval to submit it because it needs the catheter to work. On the May 2024 call, management said GenesisX would get submitted to regulators in Q2; it projected European approval in the summer and US approval in late 2024.

Given the historic delays, I wasn’t enthused by the lack of a press release announcing the submissions in the summer. However, the company did in fact submit the robot to regulators in Q2. GenesisX received CE Mark in Europe and is on schedule for a late-2024 FDA approval in the US via a 510(k). I will detail why this is a game changing product later in this article.

The second-most important aspect of the Q2 report was the update on the MAGiC ablation catheter approval process. I expected the company to either say it was working on the third section (the last one) of the regulatory questions which would lead to an October approval or that it finished everything and was waiting for any final follow-ups which would lead to a late August approval. We got the former result. I know shareholders are losing patience with this process, but I wasn’t too concerned with a two-month difference either way.

Stereotaxis is continuing to work with the FDA on MAGiC. The most important update on this process was clarification that the company got the limit of 30 patients per hospital at the two feasibility study hospitals in Europe lifted. It was unclear on the May call if the firm was limited or continuing to enroll patients. As of the May call, I believed 60 total patients treated wouldn’t have been enough to get FDA approval. I based this assumption on the fact that 182 patients + 75 patients were treated in the Helios catheter clinical trials. Stereotaxis got Helios approved (but never sold it) 16 years ago. This was a correct assumption since Stereotaxis is continuing enrollment because it needs more data. Stereotaxis likely will have enough data for an approval in 1H 2025.

Furthermore, Stereotaxis’ management discussed how the firm is working on designing a post-approval trial in the US to expand the label following a narrower initial approval. The FDA wouldn’t be asking for a post-approval trial if the process was going poorly. It seems like the FDA is working flexibly with Stereotaxis to get MAGiC over the finish line. Stereotaxis is specifically working to add the correct patients in the European trial necessary to check all the requirements for an FDA approval. To be clear, there isn’t an exact number of patients needed for approval. It’s about getting the correct patients. This can take slightly more time than just treating all patients to get to a certain amount.

Review Of Q2 Existing Products & Cash Burn

Stereotaxis received no new orders for Genesis/Niobe since the last call. Management claimed they have late-stage interest in all three geographies. I’m surprised Chinese hospitals would be discussing buying a Niobe with Genesis near approval. However, you never know when Chinese regulators will finally approve Genesis & the Microport (OTCPK:MCRPF) catheter. I’ve been disappointed with the approval process in China.

Genesis would be getting more firm orders if MAGiC had been approved a couple years ago. Instead, the excitement from MAGiC will translate into GenesisX orders. That’s not a bad thing because GenesisX will be sold at a premium to Genesis and its production will scale easier. Overall, it’s disappointing to see the lack of Genesis orders, but most investors have moved their focus to GenesisX because it might take longer for a Genesis order made today to get installed than it will take for GenesisX to start installations next year due to construction delays Genesis has been facing since its initial approval.

Stereotaxis had $4.3 million in disposable, service, & accessory (recurring) revenue which was the same as last quarter. However, the firm only had $0.2 million in system sales which was down from $2.6 million in Q1. This made the quarter look worse than it was and increased the burn rate, but I’m not concerned with minor timeline shifts in Genesis installations. As of the August call, the firm had two Genesis systems in transit. Had those two systems made it to their locations six weeks earlier in Q2, the company would have had $3 million more in sales. Instead, the company hardly showed any system sales, meaning the backlog stayed at $15.3 million.

I think the impact to the balance sheet matters more to investors than the lack of sales growth in any specific quarter. In Q1, the firm had $6.1 million in adjusted operating costs and burned $2.3 million. Management said that would be the peak burn rate for the year, but since the firm had hardly any system sales in Q2, the burn rate actually increased to $3.1 million. Adjusted expenses technically rose to $6.8 million, but I will add back the $0.5 million reversal of an aged accrued regulatory fee. That means adjusted operating expenses rose $1.2 million sequentially.

Considering the regulatory submission expenses and legal expenses from the APT acquisition (1 time event), there’s nothing unusual here. Had the $3 million in Genesis system sales occurred in Q2, the burn rate would have been lower than $2.3 million as expected. Even though system gross margins were only 27% in Q1, which has been normal for the low volume sales rate Genesis has been at, I believe the burn rate for Q2 would have been much lower with the $3 million in Genesis sales due to the expenses to build the machine occurring in Q2 without the sales.

These coming Genesis installations are why the $3.1 million burn rate won’t continue in the next couple quarters. It’s worth understanding because it looks bad at first glance for the firm to burn more in Q2 than Q1 after management claimed Q1 would be the peak. Furthermore, the firm ended Q2 with $15.2 million in cash. A continued $3.1 million burn rate would force the company to issue shares in ~three quarters. However, the firm instead guided to end the year with $13 million which doesn’t even account for the potential profit boost from MAGiC. I’ll detail my cash burn projections later in this article. For now, understand the company didn’t recklessly spike expenses increasing the burn rate. Instead, two system sales came in ~six weeks late.

Detailed Look At GenesisX

Before, I get into the details of what makes the GenesisX system so important, I’ll mention I think Stereotaxis will do an intra-quarter press release when it gets FDA approval in Q4 (unlike the recent CE Mark announcement which was made in tandem with the Q2 report). That’s based on their 2020 presser for Genesis’ FDA approval. The argument against a presser is the robot still needs FDA approval of MAGiC before it can be sold. Between now and the launch next year, Stereotaxis will be working on X-Ray compatibility, preparing the manufacturing supply chain, developing installation & commercial processes, and demonstrating real world usage.

Since Stereotaxis wants to launch GenesisX at major conferences, I think it will launch the robot in Europe at the EHRA (European Heart Rhythm Association) conference in Austria which is from March 30th to April 1st. I expect it to launch the robot in the US at HRS (Heart Rhythm Society) which is from April 24th to the 27th. The only problem with a late April US launch would be if MAGiC isn’t approved by then.

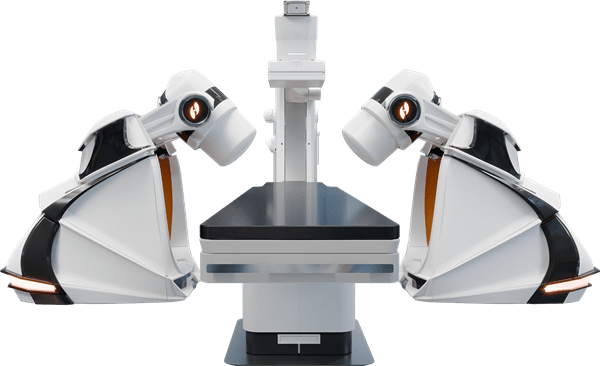

Now let’s look at the advancements in this new robot. I’ve been discussing the merits of the GenesisX for quite some time, but don’t let boredom make you forget the importance of this product. The entire benefit of magnetic robotics has been felt by a very small subset of patients and doctors in the entirety of Stereotaxis’ history (1% electrophysiology market share). GenesisX’s advancement in accessibility is a game changer. 95% of interested doctors never get a robot because of the installation time and cost associated with Genesis. GenesisX is smaller and lighter than the previous generation, while maintaining the same speed, responsiveness, and workflow.

Stereotaxis Press Release

The Genesis magnet alone weighs 640 pounds which was down from Niobe’s 764 pounds. The Genesis robot weighs about 7,000 pounds; if you add in the X-ray system, it weighs over 11,000 pounds. This is why the hospital floors needed reinforcement. Genesis also needs structural anchoring through the floor. We don’t know how much the GenesisX weighs, but we know the shipping containers will be cut in half from 12 to six large crates. Furthermore, GenesisX won’t need floor reinforcement nor will it need to be structurally anchored. This is why the GenesisX will be available for lease; hospitals can’t lease a permanent fixture like Genesis.

Stereotaxis

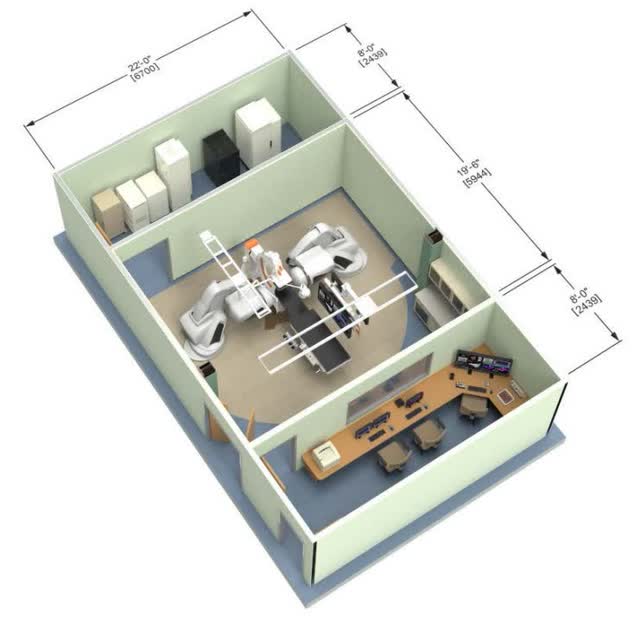

Besides floor reinforcement, Genesis requires a separate cabinet room as you can see at the top of the graphic above. GenesisX’s cabinet is 80% smaller which means it doesn’t require a dedicated room; it can be stored under a table in the operating room. Taking up less space is a huge money saver for hospitals. The construction required for wiring is also removed. Genesis needs a three-phase 480/400 volt AC 20 amp electrical panel. GenesisX requires a single fiber from each system to the cabinet and operates using standard 120/230 power outlets. GenesisX has a 96% reduction in the volume of cables from Genesis and 99% from Niobe.

The installation of Genesis requires a complete shutdown of the electrophysiology lab for a few months which is a massive opportunity cost for the hospital. This over $1 million construction cost is due to magnetic field shielding needing to be installed in the walls to prevent the magnets from impacting machines in neighboring hospital rooms. This is all eliminated with GenesisX.

As you can see from the image below, the robot bends inside itself when it’s not in use. It is a self-shielding robot. It’s easy to come up with this concept because the required shielding in the walls was a huge impediment to adoption. However, implementing it is an amazing engineering feat. As a shareholder, I’m proud of the work Stereotaxis engineers have done. Since it doesn’t need construction, GenesisX will take a weekend to install. The opportunity cost of shutting down the EP lab has been eliminated. The robot will ship nearly fully assembled.

Stereotaxis Press Release

GenesisX will have much higher gross margins than Genesis because production will scale. There will be a higher sales base on the fixed overhead expense. Stereotaxis moved into its HQ two years ago to achieve higher system production rates. The facility can produce in the mid to high teens robots per year. There is line of sight to produce one per month with four going simultaneously. GenesisX is the same on both sides instead of mirrored like Genesis which increases production efficiency.

GenexisX’s price premium over Genesis was new information. It shows the company is confident it can sell the product and wants to take advantage of the economic surplus created by the removal of hospital construction costs. Besides leasing, Stereotaxis will offer the new robot as a placement with minimum disposable commitments. This can only be offered because Stereotaxis has its own ablation catheter (MAGiC). I think the firm will bundle additional interventional devices with GenesisX in the future, with the most obvious one being the mapping catheter I will discuss in a later section.

Originally, I purchased Stereotaxis stock as a small position because I believed the MAGiC catheter would transform the firm into a profitable razor razorblade business. I only made it a large position when I discovered the firm was working on a way to make its robot much more accessible. The 2nd part of the thesis has now been realized. We just need MAGiC to be approved over the next few months to realize the 1st part. The fact that they are occurring nearly simultaneously will make sales jump quicker (the stock will likely lead sales). The main issue with MAGiC being delayed has been the cash burn in the past couple years. I will discuss why I am confident the firm can get to profitability with its current balance sheet without issuing new shares in a later section.

APT Existing Products Expanded With Stereotaxis Salesforce In US

The Access Point Technologies (APT) acquisition closed in late July. Short-term results are already being seen. APT had no US sales team prior to the deal. Stereotaxis is utilizing its 20-person sales team to push APT’s high density diagnostic catheters (also called mapping catheters) to robot users. Electrophysiologists (EPs) using Stereotaxis robots still use manual mapping catheters just like EPs who do the entire procedure manually. This is an easy bundling of devices while we are still a year or more away from a robotically steered mapping catheter. I believe once Stereotaxis comes out with its robotic mapping catheter, it will be seen as an upgrade from the current APT manual mapping catheter. That will make future robotic mapping catheter sales much easier. In the future, Stereotaxis can make both its robotic mapping and ablation catheters a part of system placements with disposable minimums.

Over 12 EPs and hospitals have tried the APT catheters or started Value Analysis Committee (VAC) submissions to buy them. APT’s sales in July were 50% higher than the average month in 1H 2024 and all of 2023. There are two sides to this data point. On the one hand, a 50% increase compared to when APT didn’t have a sales team means it’s high growth on a very low base. On the other hand, Stereotaxis has only been promoting APT’s products for a couple months and it takes at least three months to get through VACs. I’ll take it for what it is; this is a nice small sign on top of anecdotal evidence of EP interest.

APT’s New Robotic Products: Mapping, PFA, and Guidecatheter

APT’s existing products have nothing to do with why Stereotaxis bought APT nor are they relevant to the long-term value of the deal. The strategic value is the shared development of the robotic mapping catheter, PFA catheter, and guidecatheter. Furthermore, when doctors have suggestions for improvements to the guidewire and guidecatheter, APT’s manufacturing and design capabilities will allow for quicker turnaround. The market is so focused on just getting MAGiC approved, it’s missing the potential of this brilliant acquisition. This was David Fischel’s best decision of his CEO tenure.

It took Stereotaxis years to develop and get MAGiC through most regulatory processes. It needs APT to speed up the process for future interventional devices. Stereotaxis was working on a robotic mapping catheter with APT before the deal closed. Pairing robotics with a mapping catheter is going to bring all the same clinical benefits of precision, reach, stability, flexibility, and safety that it does with ablations. The workflow benefits will be apparent once Stereotaxis’ digital surgery product, Synchrony, is revealed. For now, it’s easy to imagine how another part of the process being done at the desk control center will be more efficient.

The mapping catheter’s design is complete. The company has begun its production run for formal regulatory testing. An approval is guided to come within a year. Stereotaxis has had problems with the manufacturing/design of its guidewire. I’m more confident in interventional timelines now that APT’s team is part of the firm. The mapping catheter will cost about $2k which means when it’s used with MAGiC, disposable sales per procedure will be 5-6 times what they are now.

This is the most important part of the acquisition in the intermediate term because mapping catheters are used in all procedures. It’s an obvious next step following the ablation catheter. Timelines are compressed; the mapping catheter will be approved relatively soon after MAGiC because the EU Notified Bodies asked Stereotaxis to do a human trial for MAGiC. This is creating a unique opportunity where the market is only focused on MAGiC and ignoring near-term follow-on products. Leaning into that point on regulatory approvals, the mapping catheter won’t have as difficult of a time getting approved as MAGiC because it’s not delivering care like the ablation catheter. This less stringent process is the same for the guidewire and guidecatheter which I will discuss later.

Stereotaxis is working on three potential pulsed field ablation (“PFA”) catheters. PFA is the new energy source that sits next to radiofrequency and cryo as options for EPs. PFA is in its early innings in the industry. Initial adoption has had little impact on the areas of the heart Stereotaxis robots have the most usage in. However, if Stereotaxis wants to take share long term and wants to give EPs all the options available, developing a PFA catheter will be important. PFA is far from being a risk for Stereotaxis. It’s actually an opportunity because robotics can address some of the clinical challenges with efficacy, durability, and safety PFA has faced. Even though PFA is the most hyped new technology in EP, the results haven’t been perfect.

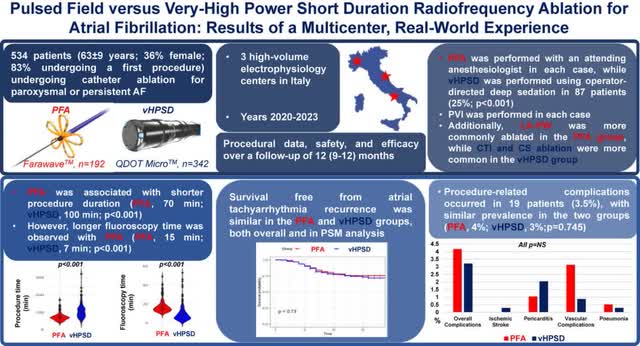

There was a disappointing PFA study in pulmonary vein isolation (PVI) which is one of the types of procedures where Stereotaxis excels. In a study of 1,184 patients that had a PVI done with a PFA catheter, 272 or 23% had an arrhythmia recurrence. 144 of these patients with a recurrence had a left atrial redo procedure. 71% of the pulmonary veins in these redo patients had durable isolation and 38% of patients had all veins durably isolated.

We also have a head-to-head study with the two latest technologies in EP which are very high-powered short duration (“vHPSD”) radiofrequency ablation (QDOT Micro) and PFA (Farawave) with 534 patients. As you can see below, the survival free results from atrial tachyarrhythmia recurrence were similar in both and they had similar procedure-related complications. The MAGiC radiofrequency ablation catheter can go up to 100 watts (vHPSD) with a very stable temperature tip. However, the initial approval label will only be for 50 watts. If the industry shifts towards high powered catheters, Stereotaxis is covered, but for now it’s a new technology that doesn’t have high usage which is why Stereotaxis isn’t going after it initially.

Heart Rhythm Journal

I’ve read mixed feelings on these new technologies from EPs and industry insiders. Dr. Christopher Woods claimed PFA’s high cost is “bilking the system.” Dr. Bilal Munir said,

“I don’t see any added advantage of PFA especially if you are a user of Qdot… PFA catheters at this point are insanely expensive as compared to radio-frequency ablation catheters with no added safety or efficacy advantage.”

However, Hardwin Mead (managing partner at Silicon Valley Cardiology) said,

“PFA is the most dramatic leap in EP since nonthoracotomy leads for ICDs. Clearly safer and quicker…we have not had any issues of pericarditis or post procedure pain which was not rare with RF.”

Bringing us back to Stereotaxis, it’s clear there is a growing list of options that can gain widespread appeal in the long term. There is much debate over which will gain market share, but Stereotaxis robots can work with both PFA and vHPSD technology. Furthermore, robots can be particularly useful with PFA which stands to be improved. If Stereotaxis’ PFA catheters show good results, the firm can benefit from PFA’s hype which is easier than creating its own (although I think GenesisX will create its own hype due to its accessibility and safety).

Stereotaxis is working its own PFA catheter based on MAGiC and two more in collaboration with other firms. The company owned PFA catheter was acquired in the APT deal and was advanced with Mayo Clinic. I discussed this in my last article. The company has been doing preclinical studies recently. It will be doing human studies for two of these opportunities in the next 6-12 months.

David Fischel (CEO of Stereotaxis) believes 1 of these PFA catheters could be commercially available in Europe as early as next year. I think that’s optimistic because it is taking ~8 months to get MAGiC approved. The exact timing isn’t as important as it is for Stereotaxis to have an answer to a growing trend that could gain significant market share over the next few years. Not having a PFA catheter at the GenesisX launch won’t be detrimental to the robot’s initial success, but it will be important to expand the energy source options for EPs over the next few years.

Finally, the APT team has been collaborating with Stereotaxis to create a guidecatheter which is the device along with the guidewire that will expand the robotic platform’s usage outside of EP. APT helped Stereotaxis come up with prototypes and iterate on them quicker. Current guidance is for both to be submitted to regulators in the next six months. As a reminder, the five potential new indications are the following: ischemic & hemorrhagic stroke, tumor embolization, peripheral artery disease, coronary angioplasty, and abdominal aortic aneurysm. If Stereotaxis can push into these indications over the next few years, it will be able to maintain the high sales growth rates it is projected by analysts to have in 2025 and 2026 (55.7% & 62.5%) in further out years.

Updated Summary Of Timelines (Stock Catalysts)

The image below shows my updated expected timelines for new product regulatory submissions, approvals, launches, and innovation day presentations. In some cases, my projections are more conservative than management targets. I am learning from past aggressiveness to increase my accuracy. If projections are fair, some events will occur earlier than expected and some will occur later than expected. If all are occurring later than expected, I am being too optimistic. With that being said, now might not be the correct time to be more conservative because APT will help with interventional devices and the company is in the late innings of its innovation plan.

I needed to address this small philosophical change to avoid confusion because many timelines are a further out than my prior article even though nothing besides the guidewire was delayed on the August call. The guidewire was projected to be submitted to regulators in six months which equates to early-2025 which is further off than prior guidance of late-2024.

Author’s Projections

Not all of these events will be major stock catalysts. I suspect approvals and subsequent sales generated from these new products will be the most impactful for the stock. However, forecasting short term stock performance isn’t the main goal of this list. Instead, it is to mark and organize each milestone to follow the company through the completion of its innovation plan. Investors in mature companies look at sales, margins, and profitability goals. We have the milestones I listed which will eventually lead us to following those traditional financial metrics.

I’ve gotten more negative on the possibility of near-term approvals in China. David guided for a Genesis approval this summer on the May call. Technically, the summer isn’t over, but it’s looking unlikely. David didn’t update his target on the August call (he just said it was a busy quarter). Since the situation is uncertain, I tried to be as conservative as reasonably possible.

As I previously mentioned, the mapping catheter, guidecatheter, and guidewire will all be easier to get approved than MAGiC because they aren’t devices that deliver care. However, the firm’s recent experience with regulators has made me a little more conservative than management. If you were to read all the new processes required to achieve European approval under the MDR (medical device regulation) regulatory regime, you would be conservative too. It’s very complex; timelines aren’t always in medical device firms’ control nor are they always predictable.

The most important milestone on this list is the CE Mark for MAGiC. The company has gotten through both the regulators’ clinical and technical questions. Last time around, the clinical questions stopped the approval because the Notified Bodies (EU regulators) required a human trial. With the feasibility study in hand, the company surpassed that portion. The only part left is the microbiology questions. I think if the firm received the questions in the few days following the August call and submits the answers a few weeks later, it will get approval in mid to late September if there are no follow up questions. If there are a couple minor follow ups, I expect MAGiC to get CE Mark in mid to late October.

I didn’t include the tender process in this list of timelines, but it’s not insignificant. A few countries in Europe have administrative processes following CE Mark before full commercial use of MAGiC is allowed. Specifically, Stereotaxis has 35 accounts in Europe and 13 will require a tender. There are four robots in France, five in Finland, two in Sweden, one in Denmark, and one in Norway. This tender process will take about six months post CE Mark. These countries have annual submission opportunities for their tenders. I’m hopeful most are early in the year which would be a few months after MAGiC gets the CE Mark. If GenesisX goes on sale in March in Europe and the tenders don’t allow for MAGiC to be used until later in the year, Stereotaxis will probably start initial system sales in nations that don’t require a tender.

Besides the four catalysts I have listed in the remainder of the year, there’s also a randomized prospective ischemic ventricular tachycardia (“VT”) study comparing robotic and manual ablation with 180 patients coming out. This is the largest randomized prospective study for VT in all of EP. I’ve been waiting for a couple years for this study to come out. It took a long time to enroll (and never finished) because robotic users didn’t want to go back to manual just for a study. The study isn’t as exciting as it would have been two years ago because it doesn’t include the use of MAGiC which will undoubtedly improve patient outcomes. However, it will be nice to see any improvements in patient care when EPs use robotics. This study will likely be published in the next few months.

Near Term Sales Projections & Intermediate Term Outline

For the first time since I’ve been following Stereotaxis, David put out extremely beatable guidance. I often tell him to under promise and overdeliver when we communicate. He should know this as a former medical device analyst/investor for his parents’ fund DAFNA Capital. Specifically, management guided for at least $14 million in sales in the second half of 2024 without including sales from APT or MAGiC. There were the two Genesis systems in transit I already mentioned plus another system about to be shipped a few days after the call. That’s $4.5 million in sales. Then you add in the $4.3 million in recurring revenue per quarter. That adds up to $13.1 million second half in sales. Furthermore, there are two systems scheduled to ship in Q4. The hospital receiving one of those systems is contractually required by a tender to get it in Q4.

That means it’s almost a lock that the company does $14.6 million in 2nd half sales and it’s fairly likely that it does $16.1 million. Current estimates are for $7.1 million in Q3 and $8.1 million in Q4 which adds up to $15.2 million. I expect Q3 to have higher system sales than Q4, but the important part here is David got analysts not to include MAGiC or the APT acquisition into sales estimates. A MAGiC approval in October or earlier will either cause estimates to increase or a beat in Q4. As I mentioned, there are 35 hospitals with robots in Europe and 13 require a tender. I’ll model two months of MAGiC selling to 22 hospitals in Q4.

I think the firm can get $1.1 million in +80% gross margin sales from MAGiC in Q4 if 10,000 procedures are done annually, 22% of those procedures are done in the nations that don’t require tenders, the catheter costs $3k, and the approval occurs in October, leading to sales starting in November. With the same assumptions except a full quarter to work with, there will be $1.65 million in Q1 catheter sales. I think the number of procedures per robot will increase in the intermediate term because MAGiC is so much better than the 20-year-old J&J catheter design and the firm will hire 1 sales rep per account to better manage each practice. If sales reps show EPs different use cases, it can increase procedure volume.

However, I won’t model an increase in usage right away. It might take several quarters to play out. When the firm gets the national tenders and the FDA approval of MAGiC later in the year, it will have ~$28 million in high margin annualized revenues (excluding China). As I mentioned, David didn’t include sales from APT in his guidance. Q3 will include two months of the acquisition. At a $5 million sales annual run rate, that’s about $833k in Q3 and $1.25 million in Q4. Therefore, MAGiC and APT give us an additional ~$3.2 million in second half sales. Stereotaxis can reasonably do $19.3 million in second half sales if that scheduled Genesis install that’s not required to be received in Q4 doesn’t get delayed.

Looking to the intermediate term future (2026), three installs of GenesisX per quarter would deliver $4.8 million ($19.2 million annualized) in sales if GenesisX sells at a slight premium to Genesis. Without the mapping catheter, China expansion, guidewire & guidecather, PFA catheter, higher procedures per robot, or Synchrony and SynX, Stereotaxis could get to $69.4 million in sales in 2026 ($28 million from MAGiC + $19.2 million from GenesisX + $17.2 million from existing recurring sales + $5 million from APT). In other words, there are eight shots on goal to get higher than $69.4 million in sales in 2026. Current estimates are for $67.1 million. Beating 2026 estimates would be an impressive achievement considering estimates call for 55.7% sales growth in 2025 and 62.5% growth in 2026.

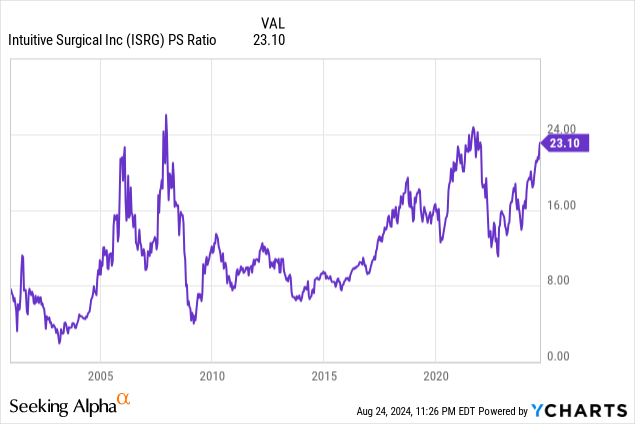

I believe if Stereotaxis is projected to profitably grow sales +20% per year in the subsequent five years, the stock will trade at 20 times 2026 sales in ~two years. It can grow at that rate by growing its install base which increases recurring interventional sales. Investors love high margin recurring sales from businesses with a high switching costs and high barriers to entry. Once EPs are trained on the robot, they won’t want to switch. Furthermore, it would take billions of dollars to create another robotic platform. There’s a reason why none exist in the EP/endovascular space yet. 20x is a conservative multiple because Intuitive Surgical (ISRG) trades at 23x sales while only being projected to grow sales ~16% in the next couple years. Twenty times $69.4 million gives you about a $1.4 billion market cap.

Near Term Cash Runway (Breakeven Timeline)

I think APT was operating near breakeven before it was bought by Stereotaxis because it had about $5 million in 80% gross margin sales with around 20 employees. If Stereotaxis’ sales team squeezes more juice from APT’s products in the US in the final five months of 2024, it will have a modestly positive impact on free cash flow. Therefore, I’ll ignore the increases in costs and sales due to APT in this cash runway analysis.

If Stereotaxis installs the three robots it said were in transit/about to ship in Q3, that’s about $8.8 million in overall ex-APT sales. Considering that the majority of the expenses necessary to build those robots were already incurred in Q2, I can see the company nearly breaking even for the quarter (less than $1 million burn). If the firm sells two Genesis systems in Q4 and has $1.1 million in high gross margin MAGiC sales, that’s $8.4 million in ex-APT sales. Therefore, I can see it operating near breakeven again (less than $1 million burn) in Q4.

Remember, the firm burned $2.3 million in Q1 and $3.1 million in Q2 while installing the equivalent sales of about two systems in the entire first half. Five system installs in the second half changes the math. System gross margins have been so low because of the high fixed overhead on a low sales base, not expensive materials and labor (marginal costs). The firm had $6.1 million in adjusted operating expenses in Q1 and $7.3 million in adjusted expenses (my adjustment + company adjustment) in Q2 due to legal expenses from the merger and regulatory submission expenses from GenesisX. I expect adjusted expenses excluding APT to be ~$18 million in the second half ($800k burn). This analysis explains why David guided for $2.2 million in cash burned in 2H 2024 (year end $13 million in cash) excluding MAGiC. Including MAGiC gets his cash burn to about $1.7 million. He’s slightly more conservative than my target.

Q1 will be interesting because it will be the only full quarter where we get to look at the free cash flow of the business including MAGiC prior to GenesisX’s launch. Of course, we won’t have the European nations that require a tender or the US. Hypothetically, if the firm has the exact same financials as Q1 2024 in Q1 2025 with MAGiC added in, it should burn about $800k less. That would cut the burn rate to $1.5 million. This shows if the company received the CE Mark 1.5 years ago, it would have been operating near breakeven (including tender nations) in recent quarters. If MAGiC is approved in April in the US, even without multiple Genesis installations per quarter, the firm will be operating very close to breakeven (less than $500k quarterly burn rate) starting in Q2 excluding GenesisX.

I don’t think investors are that worried about the company running out of money in the next three quarters prior to the launch of GenesisX. I think they are more concerned about the company heading into the launch with somewhere around $12 million in cash because they worry the launch will catalyze much more spending on a salesforce. I’ve never expected the firm to hire a large salesforce right away to sell this new system because that’s not David’s mentality. He learned from Niobe’s initial flop where a lot of systems were sold quickly without a focus on the long-term success of the EP (successful practices).

GenesisX won’t have the technical limitations Niobe had 15-20 years ago, but it still makes sense to gradually build excitement and successful placements, allowing adoption to snowball. It’s not going to require much hiring to sell the first few systems because of the initial excitement generated by an entirely new accessible robot. Instead, the firm will unleash the potential of its existing salesforce which has been dealing with the limitations of Genesis for the past few years. The firm’s HQ already has the ability to build 1 system per month. I think Stereotaxis will gradually hire employees to build systems and sell them as demand comes in. It can reinvest the profits from MAGiC following the tenders and FDA approval into scaling GenesisX. Remember, GenesisX is easier to build than Genesis because it is the same on each side.

On the Q2 call, David said,

“We have no intention of diluting shareholders at current valuation levels, and will be thoughtful in how we manage our financial position and protect shareholder value.”

I believe him because his father, Nathan Fischel, owns 16.82% of the company and his parents’ fund, DAFNA Capital Management, owns 16.66% of the company. David only takes a $60k cash salary and has limited spending to what is necessary for the innovation plan over his tenure because he doesn’t want unnecessary dilution. If the firm needs to raise $10 million for continuing operations to get to FDA approval of MAGiC, there wouldn’t be much dilution (4.4 million shares at current price). However, spiking the burn rate for years to hire a large salesforce to sell systems would create massive dilution. That type of dilution isn’t in the cards; it’s not the strategy.

Share Count & Stock Based Compensation ($9.3 2026 price target)

There are two very common misunderstandings about Stereotaxis’ financials from people who take a cursory glance at the company. One is worse than it looks and the other is better than it looks. Firstly, Stereotaxis has 133.4 million shares outstanding not the 84.6 million shown on most financial websites. That’s because it has 48.9 million in equivalent series A preferred shares. These preferred shares have a right to 6% more common shares each year on a base of 35 million equivalent shares (6% interest on 35 million shares). This was part of the firm’s September 2016 recapitalization deal (debt paid off). This means the number of common shares increases by about 2.1 million per year. However, about 9.6% of the series A preferred shares aren’t owned anymore, so it’s closer to 1.9 million more shares per year.

In Q2, the 1.5 million issued shares to APT weren’t included because the deal hadn’t closed. Therefore, we can say there really are 134.9 million shares outstanding. There could be as much as 4.6 million more shares issued to APT in the next five years if it meets all its sales and regulatory targets. If we assume Stereotaxis has 150 million shares outstanding in 2026 (includes David hitting his $1 billion SBC award & 2 million shares issued to APT) when my $1.4 billion market cap target is hit, my price target is about $9.30. The current share price is $2.29.

I believe MAGiC getting the CE Mark this fall will unlock a stock rally because investors will project a world where it completes the tenders and gets FDA approval, allowing it to reach breakeven. Furthermore, investors will start pricing in sales from GenesisX because it needs MAGiC to be sold.

On the positive side, the CEO stock-based compensation amounts shown in the quarterly press releases aren’t exactly true. They are due to an accounting quirk. David Fischel isn’t getting millions of dollars worth of shares in 2024 despite what is shown. Specifically, David’s 2021 compensation package gives him about 1% of the company per $500 million market cap tranche from $1 billion to $5.5 billion. The first milestone ($1 billion market cap) is about 0.77% of the firm and the second ($1.5 billion market cap) is about 1.15%. With 134.9 million shares outstanding, a $1 billion and $1.5 billion market cap equate to $7.4 and $11.1 share prices.

I understand investors being angry with large stock awards while the stock languishes near $2 and timelines haven’t been hit. They will be satisfied to learn he hasn’t gotten any of his award yet. The market cap needs to stay above each threshold for three months for him to be awarded shares. Then his shares vest gradually through 2030 (shows a long-term commitment to the company). If the market cap never gets to $1 billion by 2030, he only gets his $60k annual salary. The reason the CEO’s stock-based compensation shows up in reports like this can be found in the 10-K (page 57). It says the following:

“Recognition of stock-based compensation expense of all the tranches commenced on February 23, 2021, the date of grant, as the probability of meeting the ten market capitalization milestones is not considered in determining the timing of expense recognition [emphasis added]. The expense will be recognized on an accelerated basis through 2030.”

You can argue, it’s not probable that Stereotaxis will get to a $5.5 billion market cap by 2030 based on the past few years of trading, but that has nothing to due with how the expense shows up. The SBC accounting expense is going higher in future quarters regardless of whether progress is made towards market cap thresholds being hit.

Updated Review Of Risks

I’m no longer worried about whether the MAGiC feasibility study will need a lot more patients or that the FDA will require American data because the European trial has been accepting new patients and the FDA already is working with Stereotaxis to plan for a post-approval trial in America. I’m reasonably confident an FDA approval will occur no later than Q2 of next year.

The most obvious risk for Stereotaxis is how it manages everything going on simultaneously. They have to execute on regulatory submissions/approvals, scaling production, and driving system demand. A lot of innovation plan milestones will be hit in the next ~15 months. The company needs to work with regulators to get MAGiC & GenesisX fully approved while juggling the submissions of Synchrony, the guidewire, the guidecather, the mapping catheter, and the PFA catheter.

Furthermore, the company has to grow its workforce which it hasn’t had to do at all in the past few years. Scaling production and hiring a salesforce won’t be easy even if there won’t be massive hiring all at once at the GenesisX launch. Finally, the firm needs to make sure the early GenesisX installations lead to successful EP practices. I know David is extremely focused on this and will have more reps working with EPs. However, following through on the plan won’t be simple because most GenesisX adoptions will be by EPs with no prior experience with robotics.

Getting GenesisX to be used in new indications will take some convincing. Robotics will expand what is possible in the endovascular field. Early adopters will need to help the company provide evidence of procedure outcomes. Studies will be done to support further adoption. I like the setup because the firm is going after five large indications. It can support whichever one finds the earliest footing similar to how Intuitive Surgical got started. APT will iterate on guidewire and guidecatheter versions to help drive these new indications forward.

Finally, I think China isn’t in a great place economically and regulation-wise. I have no visibility into when Genesis and the Microport catheter will be approved even though the firms have been waiting for ~20 months. At this point, both getting approved and generating accelerating sales growth by Q2 2025 would be an upside surprise. This is a big shift from when I expected Genesis to get approved in Q1 of this year.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")