")

")

")

In September 2022, I marked Embraer a stock a buy and that buy rating has paid off extremely well with a nearly 220% increase in Embraer stock prices compared to a 38.5% gain for the broader markets. Since my strong buy rating in February of this year, the stock has gained 84% and now actually exceeds my price target. In this report, I will discuss the most recent results, assess the risks and opportunities and update my price target and rating.

Why Our Embraer Analysis Matters To You As An Investor?

Embraer is one of over 100 many names that I cover which benefit from a thorough qualitative and quantitative analytical process. With that analytical rigor, we analyze each and every company in our coverage portfolio and instead of comparing names, we developed an analytical model that uses a wide array of input variables to provide every name with a valuation and multi-year stock price target cadence based on an EV/EBITDA valuation against the company’s median EV/EBITDA multiple and the peer group multiple. Apart from a multi-year price target based on these multiples, we also score each stock with a rating system that includes a combination of earnings growth, historical performance against the broader markets, and expected upside of stocks against the long-term historical index growth rate of stock markets. By doing so, the names in our coverage benefit from a unified approach towards determining ratings and calculating stock price targets, and we don’t have to compare all 100 names in our portfolio to figure out which name is more attractive.

Embraer Faces Aerospace Supply Chain Challenges But Results Propped Up By Non-Recurring Tailwinds

Embraer

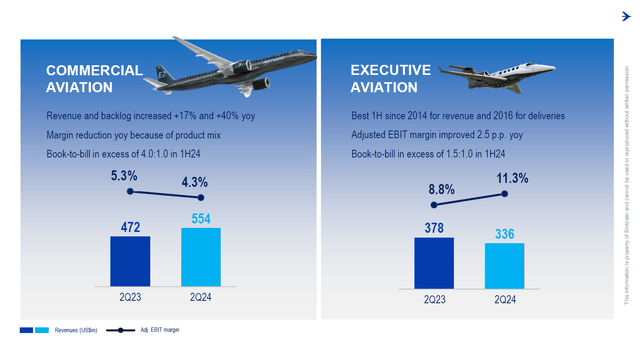

Embraer Executive Aviation deliveries came down by three units to 27 units, and I would attribute to continued challenges in the aerospace supply chain. However, sequentially the number of deliveries grew 50% and that could be seen that on a sequential basis, there is some improvement in the aerospace supply chain health. The reality for many aerospace companies is that the delivery profile remains backloaded which delays a lot of revenue, EBIT and cash flow generation into the second half of the year. Revenues declined to $336 million, but margins improved from 8.8% to 11.3%. When we consider the supply chain challenges, seeing margin improvement might be somewhat counterintuitive, but the margin improvement was mostly driven by lower selling and administrative expenses. Furthermore, the company is still aligned for a significant step-up in delivery in the second half of the year and the productivity gains underpinning that higher delivery profile are partially reflected in the first half of the year as well. With a book-to-bill of 1.5 and the best H1 2024 revenues since 2014, we see a strong backdrop despite the lower delivery volumes for the quarter.

While the business jet segment is facing some delivery pressures, the commercial aviation saw its deliveries improve by two units, however also for this segment we see that the guidance indicates that the delivery profile is backloaded. Revenues climbed 17% to $554 million, but EBIT margins contracted from 5.3% to 4.3% as the product mix was less favorable. During the quarter, Embraer E2 family deliveries made up for 58% of the deliveries, while that was 41% a year ago. The Embraer E2 family airplanes currently still have lower margins, and that drives the margin contraction. However, it should be noted that those margins still have to mature and learning curve effects should gradually increase the margins while higher production rates should also help absorbing fixed costs. Also, for the commercial aviation segment, we see a strong backdrop with a book-to-bill ratio of 4x in the first half of the year and backlog growing 40% year-on-year.

Embraer

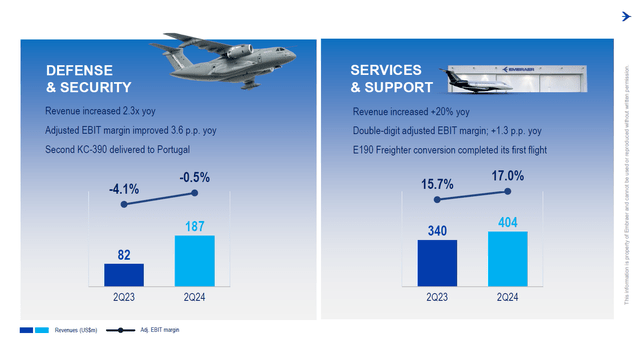

Revenues in the Defense & Security revenues climbed 130% driven by higher C-390 volumes while adjusted EBIT margins improved significantly driven by higher volume as the gross profit increased. For defense contracts, results are often recognized as a percentage of completion for the contract based on costs. Those costs are being recognized along with a portion of the expected profit. When a program volume increases, this can rather rapidly trickle through in the top line and gross profits, which we saw during the second quarter in combination with one-time items.

Services & Support is an increasing focus point for OEMs, and we saw Embraer growing its revenues by 20% to $404 million, while margins increased from 15.7% to 17%. Services come with really nice margins and those margins can also be expanded as volumes increase, allowing for even better fixed cost absorption.

Embraer

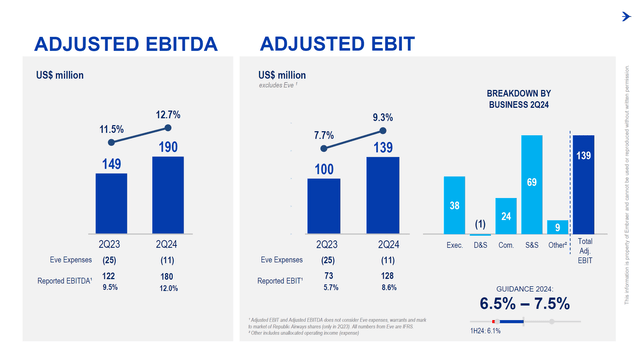

Overall, revenues grew 16% to nearly $1.5 billion with revenue growth in the commercial aviation, defense and services business partially offset by revenue decline in the executive aviation business. Adjusted EBIT grew from $99.9 million to $138.8 million and while that points at margin expansion from 7.7% to 9.3%, that margin expansion was driven by a 250 bps tax credit tailwind. Tax credits normally do not directly affect EBIT, since EBIT is earning before interest and taxes, but if re-invested or those tax credits are used to generate income that could be a tailwind to the margins. So, while we see productivity gains in for instance Executive Aviation and a strong contraction in the loss margin for the defense segment it seems that absent of the one-off tailwind margins would actually have contracted and there would be around a 100 bps headwind on the EBIT margins However, the H1 margins do point at some acceleration in the second half of the year as we will see aviation deliveries increase. So, I am not too worried about the performance in the second half of the year but do think it is important to point out that margin growth from operational strength wasn’t nearly as strong as the numbers would suggest.

What Are The Risks And Opportunities For Embraer?

There are various risks and opportunities for Embraer. The first risk I see are the aerospace supply chain issues. Those could drive some delivery delays and additional costs into the system and for many aerospace companies that has led to a heavily backloaded delivery profile, meaning that a significant portion of the results is also backloaded. Embraer is utilizing digital and AI tools to counteract some supply chain pressure. However, if we look at the results, the margins are not really showing it and I would say that the application of these tools for supply chain management either have not had a huge impact or more realistically prevented the margins from being even weaker after taking out the tax benefit tailwind.

Since Embraer is Brazil-based, we also need to keep in mind currency volatility as a risk. A stronger Brazilian real puts some pressure as for many projects the billings are in US dollars and that same US dollar would pay for less real-denominated costs. Vice versa, a depreciating real in a stable demand environment could be a tailwind.

There also are various opportunities and those are underpinned by the backlog of $21.1 billion, which is up more than 20% from a year ago, driven by higher backlogs for commercial aviation and support services. That backlog growth supports higher production of the Embraer E2, which could drive margins on better cost absorption, and Embraer is still delivering E2 airplanes that came with some lower margins as initial orders came at a lower price. As we see more airplanes being produced and more airplanes out of the higher priced backlog, we should see some margin step up.

Embraer Stock Still Has Upside After A Huge Run Up

The Aerospace Forum

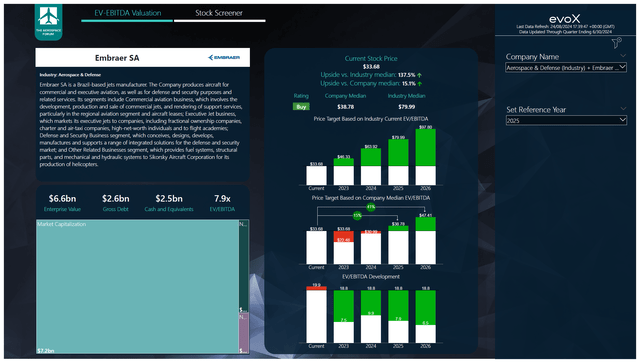

To determine multi-year price targets, The Aerospace Forum has developed a stock screener which uses a combination of analyst consensus on EBITDA, CapEx and free cash flow along with the most recent balance sheet data, cash flow statements and my assumptions on debt repayment, share repurchases and dividends. Each quarter, we revisit those assumptions and update accordingly and if need be, we supplement our own estimates if key items such as for example, acquisitions are not reflected in estimates yet. The estimates are not bases on any guidance provided by the companies we cover, but by a strong combination of consensus and my own estimates.

EBITDA estimates have gone up by around 7% for 2024 and 2025 with a 5% lift to the estimate for 2024 and 9.2% in 2025 and at least until 2026 we expect double-digit growth. Free cash flow estimates have gone up by around 10% with strong free cash flow generation expected as airplane production increases and margins should improve, while the services business could grow as well at appreciable margins.

Since the stock has run up rather quickly, I am downgrading Embraer stock from strong buy to buy. The stock is overvalued with 2024 earnings in mind from a EV/EBITDA perspective using the company median multiple. However, since we are four months away from the end of the year it does make a lot of sense to look at 2025 which would provide 15% upside with a $38.78 price target and against 2026 earnings the upside is even 41%, and then we do not factor in any multiple expansion which could also be a driver of higher stock prices.

Conclusion: Embraer Stock Is Still A Buy, But Q2 Margin Expansion Was Unimpressive

The Q2 results showed that while revenues are rising and margins are increasing year-on-year with improvement observed sequentially, there still are supply chain challenges that affect Embraer in the same way it affects many other aerospace companies. While management pointed out the utilization of digital tools and AI for supply chain management, we didn’t see any tangible impact and in the best case the use of those tools only prevented the margins from being even worse.

However, we see a lot of upside as aerospace supply chain issues ease that would allow for more evenly distributed cash flows apart from seasonal patterns and should drive some efficiency while the backlog supports higher production rates. So, as aerospace supply chain issues ease, we should see higher efficiency and higher volumes to drive growth. Keeping all of that in mind, I am putting a buy rating on Embraer stock.

Read the full article here

")

")

")