")

")

")

Despite operating in the promising semiconductor sector, Navitas Semiconductor (NASDAQ:NVTS) has been one of the worst performers of the year so far with its stock down more than 61% YTD. The main reason for this substantial drop in the company’s share price is soft demand for its power semiconductors in light of the current multi-decade high interest rates and weakening EV demand which have caused the company’s top line growth to decelerate substantially in the first half of 2024.

That said, Navitas has a strong customer pipeline which it will start tapping into starting next year, which could aid it to return to its high revenue growth figures. In light of this, as well as possible interest rate cuts later this year and the forecasted growth in the SiC and GaN power semiconductor market, I believe Navitas could be a bargain at its current valuation. Therefore, I’m rating it as a buy with a price target of $70.43 by 2032, implying 2179% upside from current levels.

Business Overview

Navitas specializes in the development and manufacturing of GaN power semiconductors. The company’s products are known for their high efficiency, fast switching speed, and smaller size compared to traditional silicon semiconductors. These features make Navitas’ semiconductors ideal for applications that require high power density and efficiency such as data centers, electric vehicles, solar systems, consumer electronics, and industrial applications.

Given the size of the industries Navitas serves, it has been witnessing substantial revenue growth over the years until this year where it is seeing soft demand for its products. This is mainly due to the current high interest rates which have led companies to reduce their spending. At the same time, the EV demand growth slump has impacted the company negatively since it is one of Navitas’ largest segments.

In Q2 2024, the company’s revenues grew 13% YoY from $18.1 million to $20.5 million, however, its revenues declined QoQ for the second consecutive quarter from the $23.2 million reported in Q1. Both quarters mark the first time Navitas’ revenues declined QoQ since its public debut in October 2021.

Although Navitas’ revenues grew YoY, its operating loss widened from $27.2 million to $31.1 million. This was mainly due to an increase in R&D costs from $16.8 million to $19 million, along with another increase in G&A costs from $13.1 million to $15.4 million. These increases were driven by product developments related to EV, solar, and enterprise segments as well as personnel growth to build out the company’s target end markets, as mentioned in the 10-Q filing.

Despite this increase in operating loss, Navitas’ net loss for Q2 2024 was $22.3 million compared to $58.5 million in the prior year. This was a direct result of the company reporting a $7.5 million gain from change in fair value of earnout liabilities compared to a loss of $32.2 million last year.

For Q3, Navitas is guiding revenues of $22 million, non-GAAP gross margin of 40%, and non-GAAP operating costs of $21.5 million.

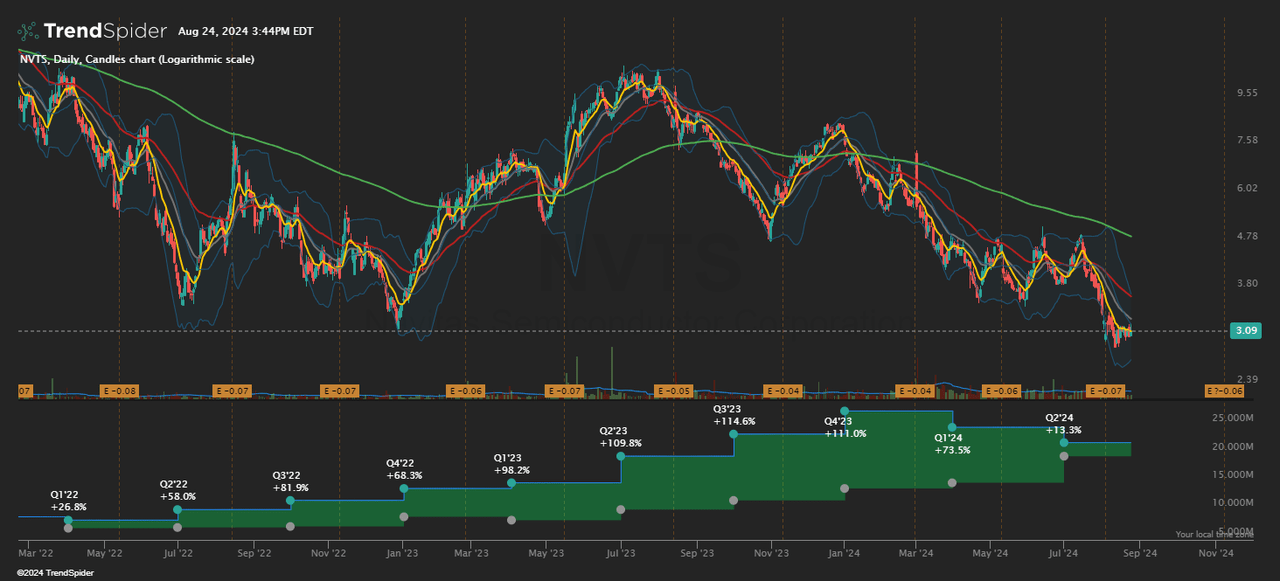

Seasonality Factor

In my opinion, Navitas’ guidance of a return to revenue growth on a QoQ basis might be an indication that its revenues have bottomed out. As is, the company’s business is seasonal with the majority of its revenues realized in the second half of the year, as shown in the TrendSpider chart below.

TrendSpider

There are two main reasons why Navitas generates more revenue in the second half of the year, in my opinion. The first reason is seasonal demand patterns in the industries using Navitas’ products, especially electronics, where the production of new smartphones and laptops often peaks in the second half of the year. This factor generally leads to higher demand for Navitas’ semiconductors during this period.

The second reason is inventory adjustments at Navitas’ customers. Throughout the year, companies generally adjust their inventory levels which may lead to higher demand for power semiconductors in the second half of the year as they prepare for peak seasons or to replenish stock.

Looking at the past three years, Navitas has generated 41.8% of its total revenue in the first half of the year on average. In fact, the percentage of revenue generated in the first half has been declining over the past three years from 45.4% in 2021 to 40.5% in 2022 to 39.5% in 2023, indicating substantially higher demand in the second half of the year.

Considering the current weakness in the semiconductor market, I expect Navitas to generate less revenue in the second half of 2024 compared to last year. Therefore, by using the average percentage of 41.8%, I’m forecasting Navitas’ full year revenues to be around $104.44 million, which would represent 31.4% YoY growth.

|

Period |

Revenue |

% of Revenue |

|

H1 21 |

$10,767,000 |

45.4% |

|

FY 21 |

$23,736,000 |

100% |

|

H1 22 |

$15,351,000 |

40.5% |

|

FY 22 |

$37,943,000 |

100% |

|

H1 23 |

$31,420,000 |

39.5% |

|

FY 23 |

$79,456,000 |

100% |

|

H1 24 |

$43,643,000 |

41.8% |

|

FY 24 |

$104,439,548 |

100% |

*Data compiled from Navitas’ earnings reports.

While my forecast may appear too optimistic given that the consensus revenue estimate for Navitas this year is $89.72 million, I believe the company could achieve my forecast through its design wins that will contribute to revenues in the second half of the year.

Seeking Alpha

In the Q4 2023 earnings call, management announced a design win in the appliance and industrial pipeline with a tier 1 player which is expected to generate $10 million per year, starting late this year.

The company also announced in the Q1 earnings call that its GaN ICs have been designed into the ground-based terminal for a major internet satellite rollout. This endeavor is expected to contribute $5 million in annual revenues starting late this year and over the next five to 10 years. Moreover, the company expects to generate $3 to $5 million in revenues in the second half of the year from more than 20 data center design wins.

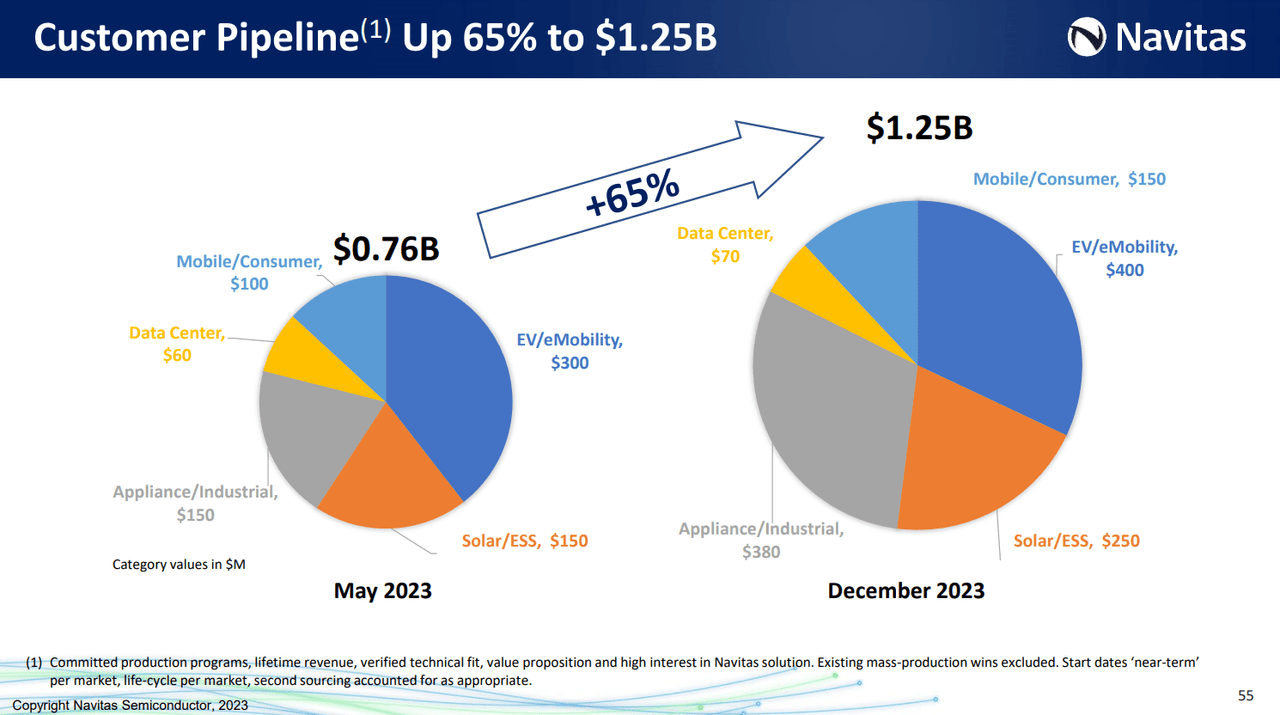

Rich Pipeline To Drive Meteoric Growth

In addition to these short term revenue tailwinds, Navitas appears to be on track to return to its meteoric revenue growth starting next year thanks to its rich customer pipeline which was worth $1.25 billion last December. This pipeline has only increased since then with multiple design wins announced in previous earnings calls.

2023 Investor Day Presentation

In terms of the appliance and industrial pipeline, management shared in the Q4 2023 earnings call that the company is in development with seven of the world’s top 10 home appliance OEMs which will drive revenue growth starting this year and accelerate in 2025 and 2026. The company also shared that it’s working with two of the top three global leaders in industrial pumps and one of the top three global leaders in heat pumps on designs that are expected to generate tens of millions in revenue starting late 2025 or 2026. Moreover, Navitas announced 25 new design wins in this segment in the Q2 earnings call that will contribute to revenues starting next year or 2026.

Looking at the solar pipeline, Navitas shared in the Q4 earnings call that it is working with three of the top five US solar OEMs and most of the world’s top 10 solar players. The company expects these design wins to add tens of millions of revenue starting 2025. Meanwhile, in Q2, the company announced 6 new design wins and is on track for a major US GaN based microinverter ramp in the first half of 2025.

Navitas’ EV pipeline is also witnessing strong growth with the company adding multiple Tier 1 EV roadside charging wins that are expected to add more than $5 million in revenue in 2025. The company is also on track to start mass production of EV GaN ICs that offer bidirectional charging at 6.6 kilowatts and 11 kilowatts with its EV design center. Moreover, the company expects to start realizing revenues from its partnership with Shinry, an onboard charger supplier for Hyundai, BYD, Honda, and Geely, in early 2025.

Moreover, Navitas is seeing strong demand for its 22 kilowatt onboard charger platform which enables three times faster charging with two times higher power density, 30% energy savings, and 40% lighter compared to other solutions on the market. According to management in the Q2 earnings call, this platform has received 15 new design wins in Q2, including three SiC wins that will start production next year. In addition, the company is on track to realize its first GaN EV revenues by the end of 2025.

As for the data center segment, Navitas shared in the Q2 earnings call that this segment’s pipeline has doubled since last December’s Investor Day, mainly due to its technological advancements. The company’s AC to DC server power supply platforms are expanding rapidly and are currently at 4.5 kilowatts and are expected to reach 8 to 10 kilowatts by the end of the year, while providing industry leading energy efficiencies of 97%.

Moreover, the company announced a major technology breakthrough in PFC circuits by unlocking additional 30% energy savings through a patent pending high frequency soft switching control method. This translates to more than 99% peak efficiency for the PFC section with higher power densities.

In my opinion, the energy efficiency rates of Navitas’ data center offering could see higher demand in the coming quarters in light of the EU’s Energy Efficiency Directive (“EED”) which aims to reduce energy consumption. Under this directive, data centers are required to achieve an energy efficiency level of at least 96%. Therefore, if Navitas’ technology proves its efficiency with customers, I expect it to receive new design wins for its data center offering.

Meanwhile, Navitas maintains its strong position in the mobile segment and was recently selected by Samsung to be used in the new Galaxy Z Flip6, Z Fold6, and all A series phones, following its wins for Samsung’s Galaxy S23 and S24 phones. Overall, Navitas has more than 50 customer designs in its mobile pipeline and is the top player in mobile fast charging.

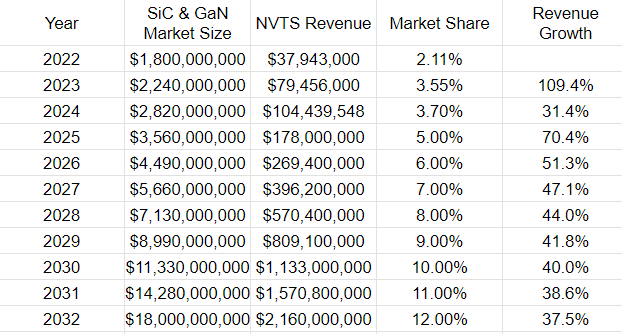

Revenue Projections

In my opinion, Navitas’ rich and growing customer pipeline will help it increase its share in the GaN and SiC power semiconductor market. This market was valued at $1.8 billion in 2022, $2.24 billion in 2023 and is expected to grow at a CAGR of 25% between 2024 and 2032 to reach $18 billion.

According to this forecast, Navitas’ share in this market grew from 2.11% in 2022 to 3.55% in 2023. At the same time, my revenue forecast for this year implies minimal market share growth to 3.7% which is attributable to the weakness in a number of the company’s end markets.

That said, since Navitas is on track to start tapping into its pipeline next year, I expect its share in this market to reach 5% in 2025 and grow by 1% in each following year. I believe that’s the case due to Navitas’ advanced technology, especially its data center offering, which could be a major attraction point to most hyperscalers. In light of this, my revenue forecasts for Navitas until 2032 are as follows.

Own Calculations

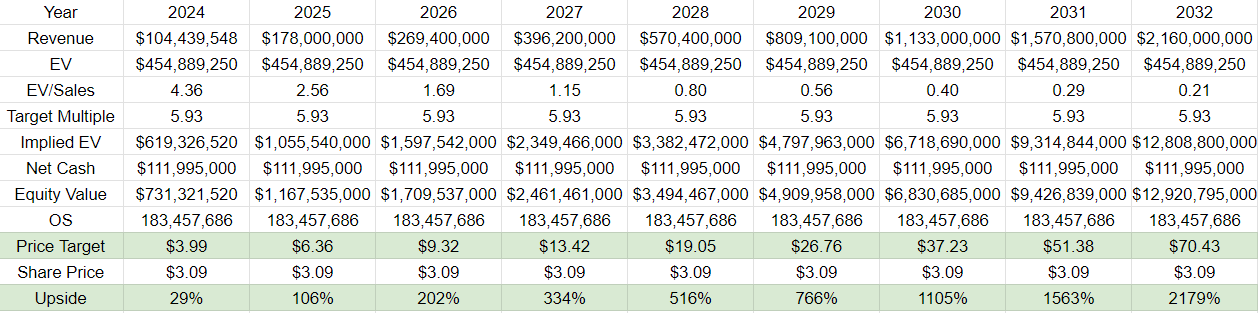

Valuation

At its current share price of $3.09, Navitas has an EV of $454.9 million, considering its cash balance of $112 million and zero debt. This translates to an EV/sales multiple of 4.36 at my 2024 revenue forecast. In comparison, Navitas’ main competitors in GaN and SiC power semiconductors Wolfspeed (WOLF) and NXP Semiconductors (NXPI) are trading at the following multiples.

|

Company |

EV/Sales |

|

WOLF |

6.30 |

|

NXPI |

5.56 |

|

Average |

5.93 |

By applying the average EV/sales multiple of Navitas’ competitors to my projected revenue figures, my price targets for the stock until 2032 are as follows.

Own Calculations

Risks

Risks to my bullish thesis on Navitas include competition which can impact its market share growth in the future and pricing power, which could lead to lower growth figures than my forecast. In addition, the semiconductor industry is rapidly evolving and if Navitas isn’t able to maintain its technological lead in the GaN and SiC market, it risks losing customers to its competitors.

Conclusion

In summary, I’m bullish on Navitas at its current valuation thanks to its growth potential in the GaN and SiC power semiconductors market. The company has a rich customer pipeline that it will start tapping into next year, and with possible interest rate cuts this year, it could return to its meteoric growth in the coming years. Considering the technological advancements of Navitas’ offerings, especially in data centers, I expect its share in the GaN and SiC power semiconductor market to increase over the coming years. In light of these factors, I’m rating Navitas as a buy with a price target of $70.43 by 2032, representing 2179% upside from current levels.

Read the full article here

")

")

")