")

")

Investors often ask what is the optimal number of stocks to hold in one’s portfolio, and the answer is that it’s not a one size fits all scenario. For one thing, sometimes it’s hard to justify dollar cost averaging into existing positions when they are trading at fair or lofty valuations.

That’s why I always keep an eye open for value stocks that pay high and well-covered dividends. Rather than simply reinvesting dividends into the same stock, I find it more appealing and rewarding to take those dividends and invest where the best opportunities are.

This brings me to the following 2 picks, which provide mission-critical infrastructure that’s unlikely to go out of fashion any time soon. Both support high yields at reasonable valuations, offering potentially strong total returns, so let’s get started!

#1: Brookfield Renewable Partners

Brookfield Renewable Partners (BEP) issues a schedule K-1 and is one of the largest pure-play owners of renewable assets, including hydropower, wind, solar, and batter storage technologies. BEP is also well-diversified by geography, with exposure to North and South America, Europe, and Asia.

BEP has a strong track record of delivering growth and value for unitholders, with 12% FFO per share CAGR since 2016 and 6% CAGR on its distribution for over two decades. It enjoys steady revenue streams from long-lived assets that carry on average 13 year contracts, and 70% of its revenues are indexed to inflation.

BEP delivered strong performance during Q2 2024, with FFO per share rising by 6.3% YoY to $0.51. This growth was driven by strong contributions from recent acquisitions, asset development, and favorable pricing in the clean power market.

Notably, BEP’s core portfolio of hydroelectric assets, which comprise 47% of the portfolio is seeing strong demand, while the wind and solar assets were bolstered by platform additions in key markets across North America, U.K., and India. This enabled BEP to commission 1.4 GW of new capacity during the quarter, furthering its market-leading position.

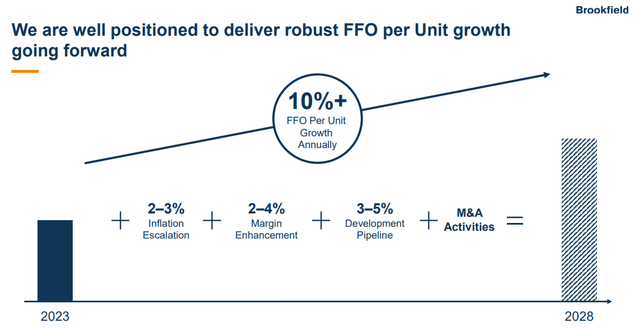

Management is guiding for double-digit FFO per unit growth this year, reflecting favorable dynamics the renewable industry. As shown below, this fits into BEP’s plan to grow FFO per unit by 10% annually through 2028.

Investor Presentation

BEP’s strategy is focused on leveraging its differentiated capabilities and access to capital to capitalize on growth opportunities in high-demand markets. This includes seemingly insatiable growth in the data center market, as highlighted below during the recent conference call:

Indicative of this, just this past week, PGM, a top market for data center development and a market where we have significant presence, had its capacity auction for 2025 and 2026 delivery.

In this auction, prices hit record highs, increasing almost 10x from the last auction indicative of supply and demand dynamics in the market. Data center investment continues to accelerate globally and it is widely estimated that data centers could reach up to 10% and 20% of electricity consumption globally and in the United States, respectively, by the end of the decade.

Meanwhile, BEP carries a BBB rated balance sheet with $4.4 billion in total liquidity. It also expects to generate an additional $1.3 billion in asset sales this year to fund opportunistic investments. Plus, 95% of BEP’s debt is held at fixed rates, and it has a long weighted average remaining debt term of 12 years with no debt maturities this year and just $300M of maturities next year.

BEP is attractively valued at its current price of $24.38 with a 5.8% distribution yield. The distribution is also well-covered by a 70% FFO payout ratio. I find the 13.3 forward P/FFO to be reasonable, considering management’s guidance for 10% annual FFO/share growth over the next 5 years. With a near-6% yield and the aforementioned FFO per share growth expectations, BEP could deliver market-beating returns from here.

#2: Plains All American

Plains All American (PAA) also issues a K-1 and is an energy midstream company that owns a large network of pipelines, traversing across the Permian Basin, Canada, Rocky Mountains, Mid-Continent and South Texas/Gulf Coast.

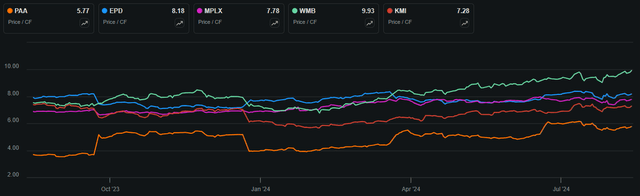

PAA is a hidden strong performer with a total return that’s beaten that of the S&P 500 (SPY) and peers Williams Companies (WMB), Enterprise Products Partners (EPD), and Kinder Morgan (KMI) over the past 3 years. As shown below, PAA’s total return of 138% compares favorably over the others.

PAA vs Peers Total Return (3-Yr) (Seeking Alpha)

PAA is executing well, achieving Adjusted EBITDA growth of 13% YoY to $674 million in Q2 2024, driven by higher tariff volumes and market-based opportunities in the crude oil business. Moreover, PAA saw favorable spreads in its NGL segment and lower-than-expected operating expenses.

While management expects for some of the savings in H1’24 to be reversed in the second half of the year, they expect to remain cost disciplined. As a result, management raised Adjusted EBITDA guidance for the full year by $75 million to $2.75 billion at the midpoint, and reiterated cash flow guidance of $1.55 billion.

This leaves PAA with plenty of cash to fund both the distribution and capital projects. It currently yields 7.1% and the distribution is very-well covered by a 190% DCF-to-Distribution coverage ratio. PAA grew its annual dividend rate by $0.20 this year to $1.27, and expects to raise it by $0.15 annually until a 160% coverage ratio is achieved.

This also leaves it with plenty of retained capital to fund growth projects, including buying an additional 0.7% stake in the Wink to Webster pipeline for $20 million, and $150M to $200M in investments into an integrated NGL value chain that includes gathering, fractionation, storage and transportation.

This positions PAA well to capture growth in this market, as NGL demand is expected to grow by $19.6 billion between now and 2028 at a 6.5% CAGR. A key driver of this demand comes from the industrial segment, as natural gas liquids are a major feedstock for petrochemical production.

Importantly, PAA carries a strong balance sheet to navigate the current interest rate environment, with BBB credit ratings from S&P and Fitch. Its net debt to EBITDA ratio of 3.1x puts it on par with that of big players Enterprise Products Partners and MPLX LP (MPLX), and it carries a sizable $3.2 billion in total liquidity.

Lastly, PAA appears to be bargain-priced at $17.85 with a Price-to-Cash Flow of just 5.8x. As shown below, this sits markedly lower than that of peers EPD, MPLX, WMB, and KMI, which carry P/CF ratios in the 7.3x to 10x range.

PAA vs Peers P/CF (Seeking Alpha)

With a 7.1% distribution yield that’s very well-covered by cash flows, ample capital for growth funding, a strong balance sheet and my expectations for a baseline annual DCF per share growth in the mid-single digit range, PAA could reasonably deliver market beating total returns from here.

Investor Takeaway

Brookfield Renewable Partners and Plains All American are two stocks that may be under the radar for many investors and present attractive opportunities to put new capital to work. This is due to their high yields, strong growth prospects, and solid financial positions within their respective infrastructure sectors.

BEP, a leading renewable energy player, benefits from its diversified portfolio, inflation-linked revenues, and a robust growth pipeline in the expanding clean energy market. PAA, an energy midstream company, has an extensive pipeline network, disciplined cost management, and very well-covered distribution, all supported by its strong balance sheet and strategic investments in the growing NGL sector.

Together, BEP and PAA provide investors with mission-critical infrastructure exposure that is positioned to deliver stable income and market-beating total return potential.

Read the full article here

")

")

")