")

")

")

| Seeking Alpha")

I have gone from being cautious on cannabis stocks to very optimistic, but I still do not like Curaleaf (OTCPK:CURLF). The stock has declined 42.5% since I last wrote about it May, suggesting then that CURLF had little upside, but I see the stock as overvalued relative to peers even at the lower price. With that said, I am raising my rating from Strong Sell to Sell to reflect less downside risk.

CURLF reported its Q2 earlier this month. In this follow-up, I discuss the chart, review its Q2, assess the outlook and analyze its valuation.

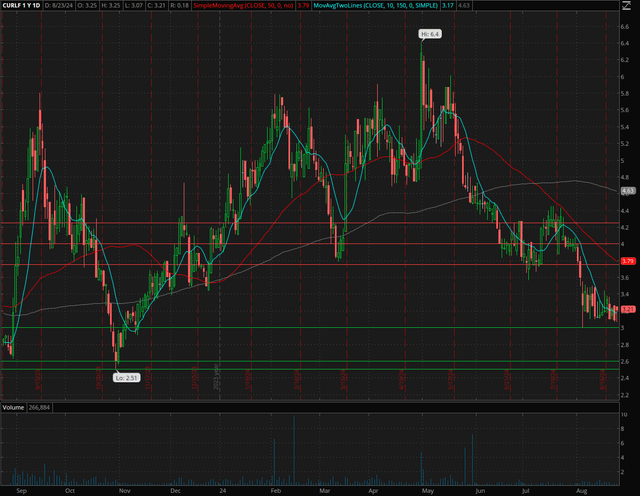

The Curaleaf Chart Is Not Good

Since reporting its Q2 on 8/7, the stock is down slightly. In August, though, it has posted a six-month low at $3.00. The stock is not too far away from its 52-week low of $2.51:

Schwab – Thinkorswim

Curaleaf has dropped more than 20% in 2024 so far. Interestingly, last October, it fell below where it was trading in late August when the potential rescheduling news hit. The all-time low of $2.19 set in April 2023 is still intact. For now, I see resistance at $3.75 to $4.50.

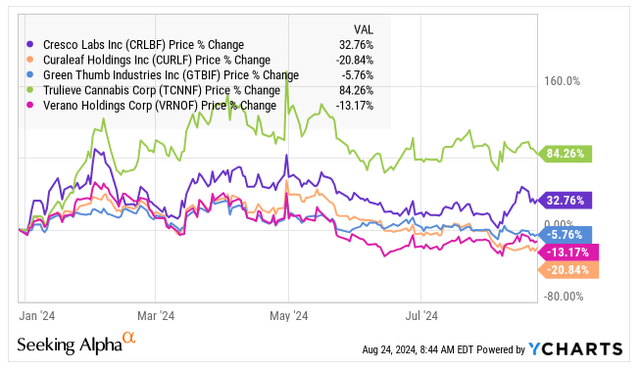

The company is one of the five Tier 1 MSOs, and its performance in 2024 has been the worst of these large companies:

YCharts

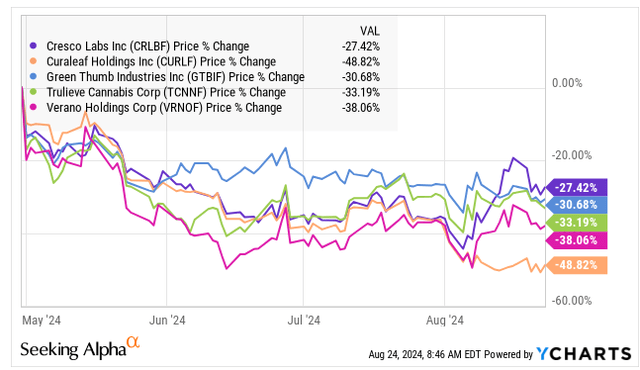

Since the peak in the market on 4/30 (when the news of the official DEA rescheduling intention hit), it has pulled back the most:

YCharts

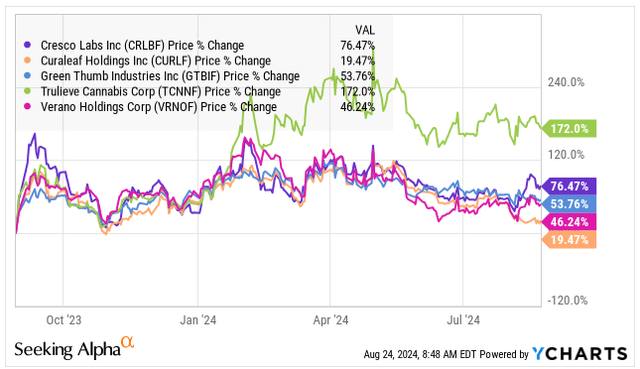

I like to compare prices to where they were on 8/29/2023, which was the day before the news hit that the Department of Health & Human Services was recommending that the DEA reschedule cannabis. Curaleaf has rallied, but it trails its peers:

YCharts

I have discussed a risk to Curaleaf: The stock represents 16.8% of the AdvisorShares Pure US Cannabis ETF (MSOS). The falling price has reduced it and has left it as the third-largest position, but the fund, which has sold a lot of shares this year, has increased its holdings of Curaleaf by 48% in 2024 to 46.5 million shares effectively. The ETF has faced liquidations before (late 2022), and it could get very nasty if that were to happen again.

CURLF Had Another Bad Quarter

Curaleaf reported its Q2 on August 7th and filed its SEDAR filings after the close on August 8th. It’s not the only large MSO that still does not file with SEC, but most MSOs file with the SEC.

Analysts, according to AlphaSense, were projecting Q2 revenue of $346 million with adjusted EBITDA of $81 million. The company reported lower revenue than had been expected, with growth of just 2% from a year ago to $342.3 million. Adjusted EBITDA of $73 million was also below what had been expected, and it rose just 1% from a year ago and fell 5% sequentially.

Helping the company’s revenue growth was its international operations, which expanded 78% from a year ago to $25.2 million, still less than 8% of its overall revenue. Its domestic revenue fell 1% to $317.0 million. With its domestic operations, retail business dropped 6% to $255.2 million, while its wholesale business expanded by 24% to $61.5 million.

The balance sheet saw tangible book value fall to -$782 million in Q2. Net debt, which excluded $632 million of income-tax related liabilities, was $474 million. Operating cash flow in H1 was $73.1 million, which is ahead of what they generated in 2023-H1, but the amount generated in Q2 fell sequentially. If rescheduling takes place, the elimination of 280E taxation will boost the cash flow. I think, though, that Curaleaf will be among the most likely MSOs to sell stock due to its balance sheet. If 280E remains, this could be a big challenge for the company.

After the Q2 report, the company announced that its CEO is leaving. The Executive Chairman, Boris Jordan, will be replacing him. The company has had a lot of turnover in this top role, and this is not a good sign. Jordan has been highly involved since before the company went public in 2018.

Analysts Are Less Optimistic About Curaleaf

Ahead of the Q2 report, analysts were projecting revenue of $1.404 billion in 2024 and $1.579 billion in 2025. They were forecasting adjusted EBITDA of $341 million in 2024 and $379 million in 2025.

After the report, analysts have lowered their estimates. Analysts now project 2024 revenue will grow 4% to $1.391 billion with adjusted EBITDA of $316 million, up just 4% as well. For 2025, they expect revenue will increase 10% to $1.526 billion. Adjusted EBITDA is projected to increase 18% to $371 million, a margin of 24.3%.

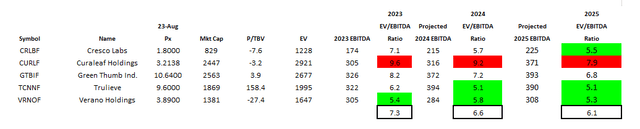

The Curaleaf Valuation Is Too High Relative to Peers

Curaleaf’s valuation seems very reasonable, but it is much higher than the other Tier 1 MSOs:

Alan Brochstein, using AlphaSense

The Tier 1 names are generally too highly valued compared to Tier 2 names in my view. My favorite Tier 2 stock, Ascend Wellness (OTCQX:AAWH), trades at an enterprise value to projected adjusted EBITDA in 2024 of just 4.4X.

Curaleaf has more debt than its peers, and it still has a negative tangible book value. Ahead of the report, I was sharing a year-end target with my subscribers at 420 Investor based on a multiple of 10X for its enterprise value relative to the projected adjusted EBITDA in 2025, and this worked out to $4.35. Updating it and using the same multiple, which I believe is a premium to its peers that may not be warranted, I now get $4.25. This would represent a gain of 32%. If rescheduling fails to take place, I think the valuation would drop considerably.

Conclusion

While CURLF has dropped a lot, it is not the stock to buy for those interested in cannabis. There are other MSOs that make more sense. For those that want a very large one, I have upgraded both Green Thumb Industries (OTCQX:GTBIF) and Verano Holdings (OTCQX:VRNOF) recently to Neutral from Sell, and I include both in my model portfolio at 420 Investor that aims to outperform the American Cannabis Operator Index. For those that can buy smaller operators, I still hold very large positions in both of my model portfolios in Ascend Wellness and Planet 13 (OTCQX:PLNH).

I continue to see opportunities beyond the MSOs with respect to rescheduling with Ancillary companies, like WM Technology (MAPS). This is one of my largest holdings in my model portfolio that aims to outperform the Global Cannabis Stock Index. Just a week ago, I explained why it is a Strong Buy still. The Canadian LPs don’t have a direct benefit from this likely rescheduling of cannabis, but my largest position is Village Farms (VFF). I include two others in my model portfolio.

Curaleaf, while popular with investors, is not performing well. The stock looks overvalued relative to peers and has a very challenged balance sheet. It has international opportunity, and I like that it now has two stores in New York for adult-use sales. While I have a Sell (instead of a Strong Sell), the stock could rally. I think that Curaleaf will underperform its peers. Cannabis investors should find a better stock!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")