")

")

")

Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the third week of August. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

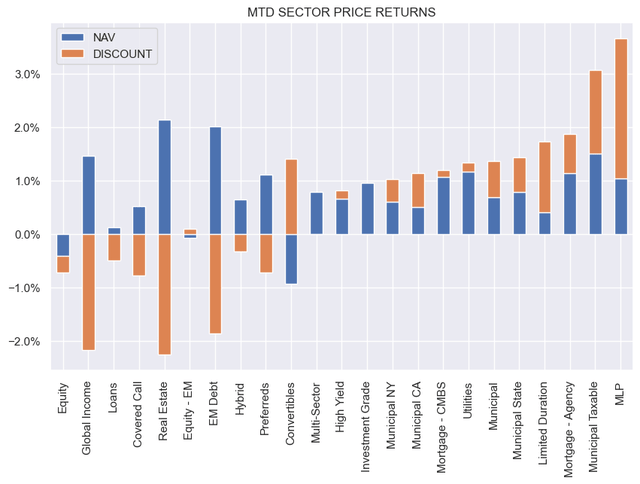

It was a strong week for CEFs with all but one sector finishing in the green. Month-to-date, most CEF sector NAVs are up, with discounts mixed.

Systematic Income

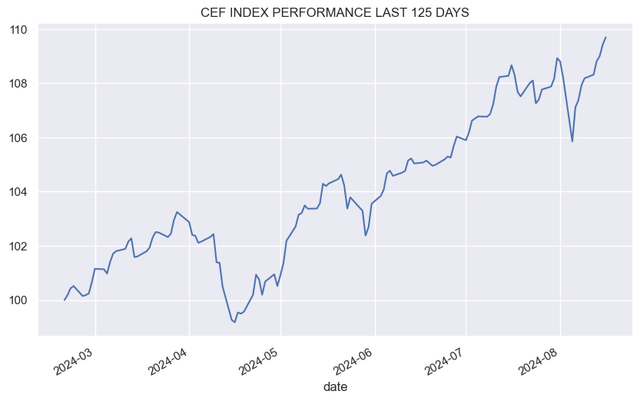

CEFs powered through the recent drawdown and pushed higher, supported by lower Treasury yields.

Systematic Income

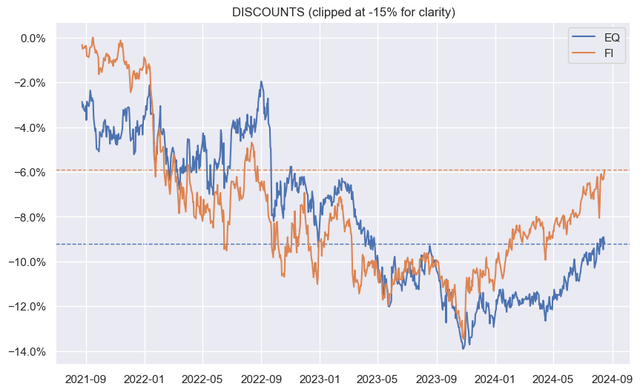

Fixed-income CEF sector discounts have continued their tightening trend and are on the expensive side of fair-value.

Systematic Income

Market Themes

Tortoise is planning to merge three of its MLP-focused CEFs (TPZ, NDP, TTP) into a new ETF. The discounts of the 3 funds are around 4%. If this happens, the discounts will move to zero, however it’s important not to consider this an “arbitrage”.

The word is thrown around very carelessly. This situation, like many others, does not offer an arbitrage, which itself means a riskless profit. That said, it’s sensible to hold the funds in expectation of the merger, particularly for investors who hold other MLP funds and who are comfortable with the sector.

There are two primary risks to investors in this strategy. One is the sheer volatility of MLP funds – last week NDP fell nearly 10% which illustrates that the 4% discount accretion “arbitrage” can be easily negated to result in a significant loss to shareholders. And two, shareholders have yet to approve the transaction, and if they don’t (CEF shareholders have a tendency to not care), then the discounts will widen back out – a real risk to holders.

The word arbitrage is typically applied to a trade in two different but related assets such as cash Treasuries and Treasury futures, i.e. a long/short transaction which can generate a riskless profit. This is the right context for the word. Anything else is more of an asymmetric risk/reward, alpha pick-up or relative value rather than an arbitrage.

Market Commentary

Nuveen Preferred & Income Term Fund (JPI) discount widened as the tender offer expired. Not enough shares were tendered (37% were tendered) which fulfilled the condition for the fund to carry on as a perpetual fund rather than terminate. The discount now stands at 3.3% and could widen slightly in the coming days. The tight 4% discount on its sister fund JPC should limit the widening. The Nuveen preferred CEFs don’t look very attractive in the sector. The Flaherty and Cohen funds look more compelling, e.g. PFO and LDP.

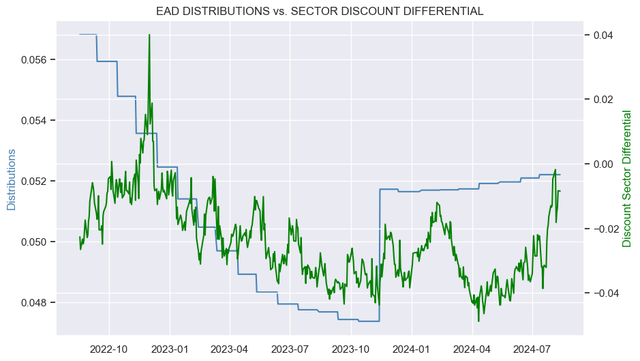

Allspring CEFs (EAD, ERC, ERH, EOD) made their usual distribution adjustments. The funds have managed distribution policies that set the distribution to a percent of the trailing 12-month NAV. CEF NAVs have generally uptrended which has driven higher distributions. The discount differential of EAD to its sector has roughly followed its distribution changes. It’s one reason why the fund is no longer cheap in its sector.

Systematic Income

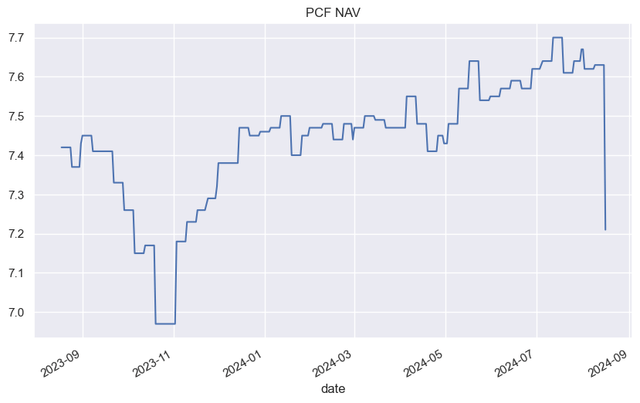

High Income Securities Fund (PCF) finished its rights offering. There was takeup of around 2/3 of shares offered. The NAV dilution was duly registered on Friday.

Systematic Income

The fund will hold a special meeting of shareholders later this month to consider a new advisory agreement with Bulldog and an expansion to the fund’s strategy. If both proposals are adopted, the fund will tender back 90% of the newly issued shares at a 2% discount and 60% if the proposals are not approved. If the NAV remains at today’s level, then the tender offer has around 9% of “juice” in it, given the subscription rights offering price of $6.48.

Stance And Takeaways

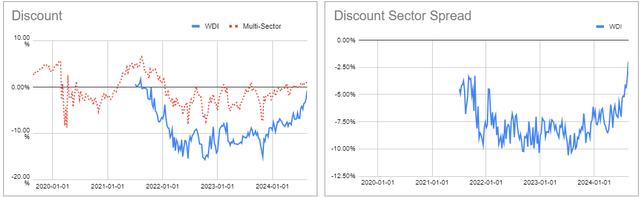

This week, we lightened up on the Western Asset Diversified Income Fund (WDI). The fund’s valuation has richened considerably, both in absolute terms as well as relative to its sector. The upcoming Fed cuts are also likely to reverse the fund’s previous distribution hikes.

Systematic Income BDC Tool

Read the full article here

")

")

")

")