")

")

")

In June-end, we initiated International Airlines Group (OTCPK:ICAGY) (OTCPK:BABWF) coverage with a buy rating supported by:

- A strong brand portfolio with the ability to compete in long-haul distance (flag carrier peers) and with low-cost operators;

- A positive outlook thanks to corporate travel demand and a leaner cost structure;

- An unjustified valuation discrepancy compared to its peers.

On 01/08/2024, the company reported its H1 results and was the only EU airline company to beat Wall Street analysts’ expectations. Despite higher capacity, the company achieved unit revenue growth, and the management team believes its customer exposure and geographic footprint, along with IAG transformation initiatives, resulted in the Q2 outperformance. Here at the lab, we have already seen support from our investment equity story, and the company stock price is up by 10.7% (Fig 1).

Mare Ev. Lab Rating Change

Fig 1

Q2 Results

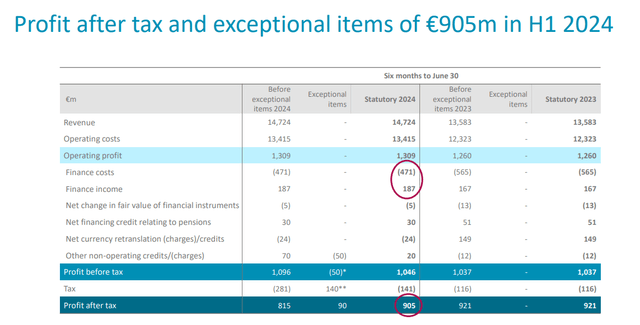

International Airlines Group reported a Q2 operating profit of €1.24 billion, compared to a company-compiled consensus of €1.08 billion. The outperformance is clearly due to cost control. Q2 capacity was up 8.0% year-on-year with a load factor of 86.7%, again indicating a plus three basis points higher than last year. Revenue per Available Seat Kilometre (RASK) increased by 1.8% thanks to passenger revenue pricing power. Excluding fuel costs, IAG’s operating costs were flat. On a positive note, we report the company’s cargo capacity is up by 15.4%, and as anticipated, thanks to our follow-up note on Deutsche Post, the division’s unit sales were down by 12.4%. Here at the Lab, we believe this is mainly due to IAG’s lack of exposure to Asia. According to the P&L analysis, IAG’s net profit reached €908 million and was 10% lower than last year. The higher corporate tax impacted net income but was still ahead of Wall Street consensus, which was estimated, on average, €815 million.

IAG H1 Financials in a Snap

Source: IAG Q2 results presentation – Fig 2

The company’s results showed a substantial earnings uplift from British Airways. We also report an outperformance in IAG loyalty profits. On a negative note, Aer Lingus’s results were weak, and we see a small softening at Vueling and Iberia. IAG reported a solid performance in Europe and the North Atlantic compared to its flag carrier peers. Contrary to the cargo division, we believe IAG was helped by its small exposure to Asian consumer sales.

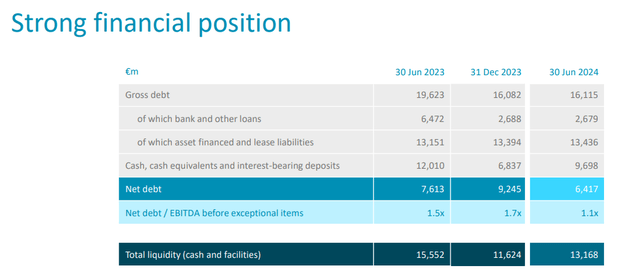

With support from an FCF generation, IAG’s net debt reached €6.4 billion and fell by €1.0 billion in the quarter. This was also due to seasonal working capital patterns. Consequently, the company’s net debt/EBITDA decreased to 1.1x from 1.3x quarter-on-quarter (Fig 3).

IAG debt evolution

Fig 3

Why are we still positive?

Last time, we anticipated a dividend reinstatement. In the Q2 results presentation, the company announced it would pay a €0.03 interim dividend. The CEO commented: “We are pleased to announce a return to paying a dividend, which reflects our confidence in the business, our performance, and our transformation. We are delivering on our strategy and commitment to sustainable shareholder returns”. Here at the Lab, despite widespread investor concerns about the sustainability of airline companies’ profits, we believe this €0.03 interim dividend is symbolic but a sign of IAG’s confidence in its future performance. This is also the first return shareholder returns since the pandemic outbreaks.

Again, starting with the CEO’s comment, IAG continues to see “strong demand for travel in the attractive core markets in which we operate: North Atlantic, Latin America and intra-Europe.” Last time, we reported the long-haul capacity upside. Here at the Lab, we believe there is a risk that yield pressure might come from consumer demand from value to premium segments or competitor supply capacity shifts. While cognizant of these risks, IAG does not see signs of deteriorating supply/demand and pricing trends, with a Q3 already booked at approximately 80%. In the Q2 results, we report solid premium leisure demand and Iberia Airlines benefiting from increased business demand on LATAM routes.

On the new upside, we positively report the following:

- (No additional M&A). IAG terminated the agreement to acquire Air Europa. A €50 million break-up fee is to be considered. The company was unable to earn the approval of EU competition authorities. Here at the Lab, we were concerned about the debt that needed to be raised. In addition, in the first place, we were believers in the IAG’s initiative to win market share from Air Europa more straightforwardly by competing against it. We believe IAG has the chance to redeploy some Air Europa investments across its existing businesses. Air Europa is the third-largest Spanish airline after Iberia and Vueling (owned by IAG). Therefore, it was a complex deal execution;

- (Buyback Upside). As already reported, at June-end, supported by summer bookings inflow, net debt reached €6.4 billion. We anticipated a higher dividend payment, but following the €0.03 interim dividend proposal and the solid Q2 FCF generation, we see a 2024 Net Debt/EBITDA estimate improvement from 1.4x to 1.3x. This is well below IAG’s target of <1.8x. Therefore, the company could announce a share buyback on top of the dividend payment. According to our calculation, with a €600 million buyback, equal to 6% of the company’s market cap, the leverage would increase by only 0.1x. This also takes into account a lower 2024 CAPEX guidance. This is now set at approximately €3.3 billion, with an FCF estimate (after lease payments) at €1.7 billion. Lower CAPEX investments are due to aircraft delays;

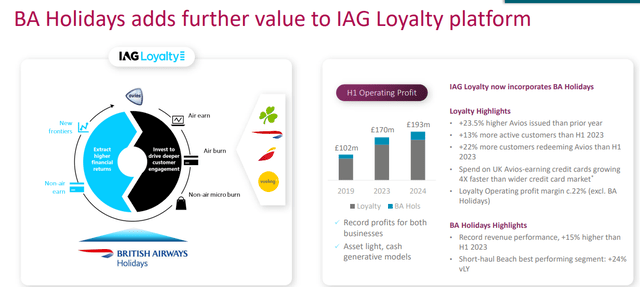

- (IAG Loyalty Platform). One of IAG’s new earnings pillars is generating capital-light profit growth. In April 2024, the company unified its loyalty program division. We anticipated synergies over time and higher profitability. That said, looking at the results, IAG registered 13% more active consumers on a standalone basis than H1 2023 (Fig 4). At first glance, this business might be marginal; however, it accounts for 15% of the company’s total EBIT.

IAG Loyalty Platform Upside

Fig 4

Adjusting Estimates and Valuation

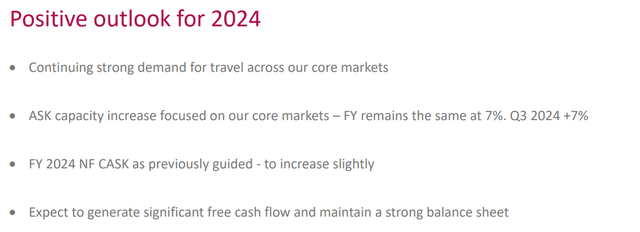

Before the Q2 results, our team was already above Wall Street’s expectations. The airline reiterated its plan to grow capacity by approximately 7% in 2024 (Fig 5). For this reason, we leave our top-line sales estimates of €31.9 billion unchanged. Considering the current booking trend, this includes an achievable load factor of 85.8%.

The company also guides non-fuel CASK to rise slightly but points to significant positive free cash flow expansion after lowering the capex. The company-compiled consensus set a 2024 operating profit of €3.58 billion. Given the fuel hedge, which is at 74% compared to a previous quarter of 70%, and a lower oil barrel cost projection, we believe there is still an upside. That said, we are already incorporating an EBIT forecast of €3.8 billion ahead of consensus and leave our estimates unchanged. On the technical guidance, IAG corporate tax might be higher than 24%, but we estimated €500 in net financial expenses (given the FCF generation, the company now has balance sheet flexibility). Therefore, our net profit projection remains at €2.5 billion with a €0.47 EPS.

Our team continues to see IAG’s relatively high margin and attractive valuation. The company trades on 4.3x 2024 P/E, still below the pre-pandemic median (8.2x) and its peer group median (5.8x). For consistency, applying a 5x P/E and a 4.5x EV/EBITDA multiple, we value the company at €2.5 per share ($5.34 in ADR). IAG has strong positions in the North and South Atlantic region, which we anticipate will deliver strong profitability through Q3. In addition, IAG trades at a 2024 EV/EBITDA of 3x, which is well below the bottom end of the last cycle range. Indeed, IAG has always traded between 3.5x and 7x). This offers potential valuation upside ahead.

IAG 2024 Outlook

Fig 5

Risks

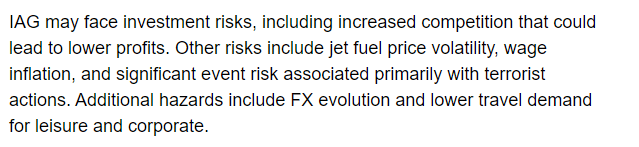

Here at the Lab, we have already reported IAG’s main risks (Fig 6). In addition, other downside pressure might come from natural catastrophes related to weather events and geopolitical headwinds. Given that the two companies are going their separate ways in Spain, we will closely watch the competition from Air Europa. Still related to Spain, there are unresolved labor issues with Iberia Airlines, which might impact the company’s profitability.

There is an ongoing valuation discrepancy between EU peers and our target price, and we implied a supportive unit revenue trend compared to peers.

Mare Previous Risks section

Fig 6

Conclusion

IAG Q2 results were very supportive, and the company’s valuation is even more attractive. We view this deleverage path positively, and a dividend reinstatement offers downside protection. We include three additional upsides to consider. For this reason, we confirm our buy rating target.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")