")

")

")

")

We previously covered Medical Properties Trust, Inc. (NYSE:NYSE:MPW) in June 2024, discussing why we had upgraded the REIT as a speculative buy then, attributed to Steward’s finalized bankruptcy and the long awaited FQ1’24 dividend announcements – with it providing the much-needed resolution to its ongoing tenant troubles.

With FQ1’24 bringing forth a decent balance sheet as the management also guided improved liquidity in 2024, we believed that MPW was likely to weather the near-term uncertainties well enough, warranting the upgraded Buy rating for patient investors with higher risk appetite.

Since then, MPW has traded sideways at -2.7% compared to the wider market at +3.4%. Even so, we are reiterating our speculative Buy rating, since H2’24 may bring forth a healthier balance sheet and improved bottom-lines, thanks to the ongoing capital raises through asset sales.

While the elevated short interest of 36.3% remains a major concern, the bulls has continued to defend the Q2’24 bottom of $4s, with it triggering an improved margin of safety for those looking to dollar cost average.

MPW’s Investment Thesis Continues To Improve On A Sequential Basis

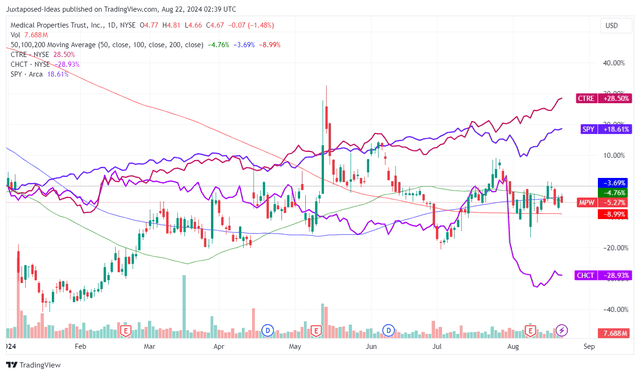

MPW YTD Stock Price

Trading View

MPW’s YTD stock performance has been nothing to shout about indeed, with it underperforming the wider market and its healthcare REIT peers, aside from Community Healthcare Trust (CHCT) attributed to the latter’s FQ2’24 earning misses.

Even so, there has been improved clarity from the Steward bankruptcy, significantly aided by the MPW’s ongoing sales of numerous assets, including:

- its interests in five Utah hospitals for $1.1B,

- five facilities in California and New Jersey for $350M,

- eight facilities in Arizona for $160M – at an estimated $68M spread,

- eleven facilities in Colorado for $86M – at an estimated $22M spread,

allowing the management to unlock more cash to bolster its balance sheet.

For now, the excess cash has allowed the REIT to report the repayment of approximately $1.5B in debt including those maturing in 2024, with it freeing up any further capital raises over the H2’24.

Even so, readers must note that MPW still reports a relatively elevated Transaction Adjusted Net Debt to Annualized EBITDAre Ratio of 8.1x in the latest quarter, compared to the 6.9x reported in FQ2’23 and 6.0x in FQ4’19, with the ongoing asset sales triggering the moderating Adjusted EBITDAre at $257.01M (-3.6% QoQ/ -26.7% YoY).

This has been well balanced by the lower adjusted interest coverage ratio of 2.6x in the latest quarter, compared to the 3.4x reported in FQ2’23.

With only five months left in the year and another $1.28B of MPW’s debts maturing in 2025/ $2.35B in 2026, we believe that the raised liquidity target from $2B to over $2.5B has been rather encouraging indeed, since it allows MPW to “create additional liquidity, comfortably satisfying our expected maturities in 2025 and beyond.”

This is also why the REIT’s cut dividends from the quarterly payout of $0.15 per share to “no more than $0.08 per share” effectively allows the management to rebuild its balance sheet health over the next few quarters.

Most importantly, aside from Steward Health Care and the recently sold CommonSpirit Health assets, MPW’s other assets continue to generate robust rental revenue growth to $246.69M in FQ2’24 (+6.6% QoQ/ +5.7% YoY).

While FQ2’24 has brought forth numerous impairment charges on the REIT’s Other (Expense) Income, attributed to the ongoing asset sales and fair value adjustments on securities, we believe that the worst may very well be behind us and H2’24 likely bringing forth improved clarity on a sequential basis.

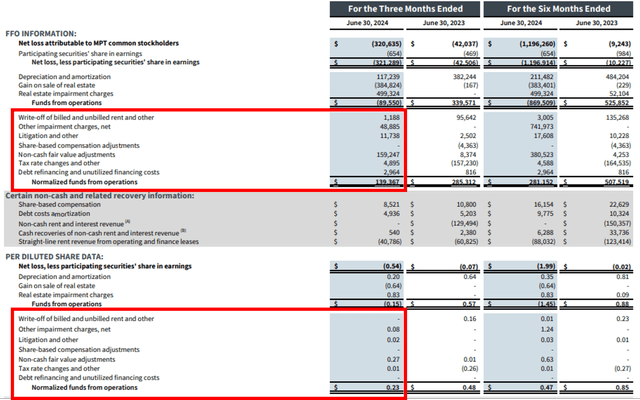

MPW’s Normalized FFO Remains Robust

MPW

As a REIT, the best measure of MPW’s cash flow will be its Normalized funds from operations, which has excluded the impact of Non-cash fair value adjustments/ impairments.

Despite the ongoing Steward bankruptcy and numerous charges, it is apparent that MPW remains profitable enough at Normalized FFO per share of $0.23 (-4.1% QoQ/ -52% YoY).

While this number may have declined on a QoQ/ YoY, we believe that the management’s aggressive deleveraging may significantly aid its bottom-lines ahead, allowing it to report a sequentially lower interest expense from the $101.43M (-6.6% QoQ/ -2.9% YoY) reported in the latest quarter.

Combined with the resultant lower FFO payout ratio of ~35% (-35 points YoY) compared to the sector median of 63.9%, we believe that MPW’s dividend investment thesis remains secure.

This is also why we believe that the stock has been well supported at the Q2’24 bottom of $4s, with it triggering an improved margin of safety for those looking to add.

So, Is MPW Stock A Buy, Sell, or Hold?

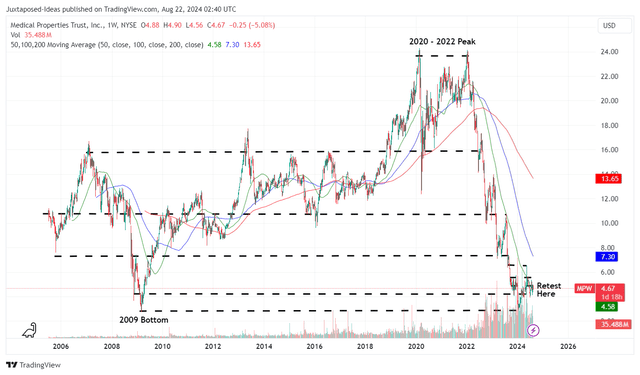

MPW 18Y Stock Price

Trading View

Based on the price chart above, it goes without saying that MPW has had a painful two years, with it effectively losing -86% of its value since the 2022 peak while trading near to its 50 day moving averages after the bounce observed in January 2024.

Despite the dividend cut and the potential value trap, the REIT continues to offer a relatively rich dividend investment thesis based on the forward yields of 6.8%, compared to the sector median of 4.33% and the US Treasury Yields between 3.66% and 5.13%.

This is especially since the market is already pricing in a 25 basis point rate cut in the Fed’s upcoming FOMC meeting in September 2024, building upon the 25 basis point cut observed in the EU by June 2024.

As a result of the still decent dividend investment thesis, we believe that investors may still continue holding on their existing positions – since MPW remains inherently undervalued at FWD Price/FFO valuations of 5.13x, compared to its 10Y mean of 11.20x and the sector median of 14.03x.

Even when compared to its healthcare REITs, such as CHCT at 9.48x and CareTrust REIT (CTRE) at 19.41x, we maintain our belief that the market may eventually upgrade MPW’s valuations nearer to its historical means once its financial turnaround is completed and market sentiments normalize.

The target timeline is likely to be on September 30, 2025, based on the temporary waiver of Steward’s loan provision and real estate leases, as discussed in the FQ2’24 earnings call.

MPW’s upgraded valuations to the 10Y mean of 11.20x naturally implies a speculative upside potential of +115.1% to our bull-case long-term price target of $10.20, based on the consensus FY2026 FFO estimates of $0.91.

As a result, we are reiterating our Buy rating for MPW, albeit with the caveat that investors temper their near-term expectations, since we expect the reversal in its financial performance/ stock prices/ valuations to be prolonged, worsened by the uncertain macroeconomic outlook.

At the same time, with the REIT likely to be inherently smaller and focused in its operations, as the management guides “no exposure to Steward” by 2025 through a mix of sales and re-tenanting, we may see its impairment charges continue for a little longer – impacting its bottom-lines and optics.

For now, investors may continue getting paid rich dividends while waiting for MPW’s speculative reversal by 2025.

Read the full article here

")

")

")

")