")

")

")

")

Investment thesis

I have mixed feelings about my initial bullish thesis about Veeva Systems (NYSE:VEEV). The stock rallied by solid 11% since December 2023, but the broader market’s performance was far better.

The company reports its Q2 earnings on August 28, which is always a crucial development. I want to update my thesis in light of the upcoming earnings release and explain why recent developments support my bullishness. VEEV’s valuation is also still very attractive. All in all, I reiterate my “Strong buy” rating for VEEV.

Recent developments and Q2 earnings preview

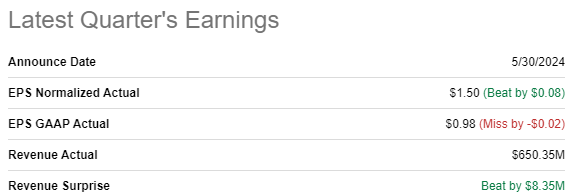

VEEV released its latest quarterly earnings on May 30. The company delivered positive surprises both from revenue and adjusted EPS perspectives. Revenue grew by 23.5% on a YoY basis. The adjusted EPS expanded notably YoY, from $0.91 to $1.50.

Seeking Alpha

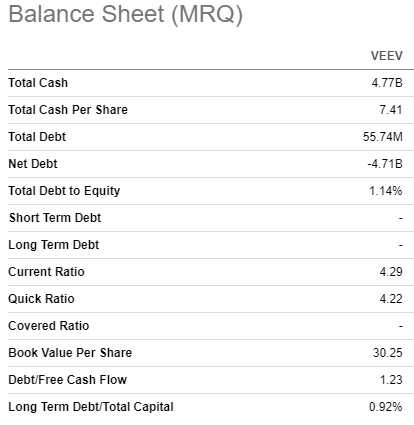

VEEV demonstrated strong operating leverage in Q1, which is always a bullish sign for me. The gross margin expanded YoY from 70.8% to 73.3%. The operating margin has more than doubled YoY, from 11.7% to 24.6%. Strong efficiency allowed VEEV to significantly improve its levered free cash flow [FCF], from $432 million to $749 million on a YoY basis. As a result, VEEV’s balance sheet became stronger with a massive $4.77 billion cash pile and almost no total debt. The company’s fortress financial position is another apparent bullish indicator that provides VEEV with a massive financial flexibility to invest in new projects.

Seeking Alpha

Despite stellar Q1 performance, the stock saw a 10% selloff on May 30. The reason is in the guidance downgrade, but it was almost invisible. The company’s full-year guidance was about $10 million lower revenue, and one cent lower EPS compared to consensus. I consider these discrepancies as insignificant and definitely not deserving such a one-day selloff.

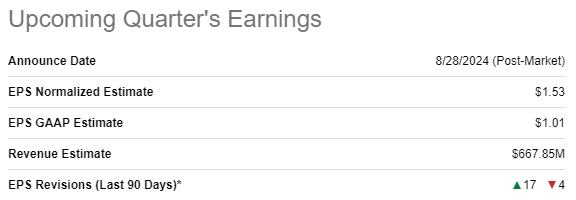

The upcoming earnings release is scheduled for August 28. Wall Street analysts forecast Q2 revenue to be around $668 million, which will be a 13% YoY growth. The adjusted EPS is expected to expand from $1.21 to $1.53 YoY. Wall Street analysts appear to be quite optimistic about VEEV’s upcoming earnings release as there were much more EPS upgrades than downgrades over the last 90 days. This is a solid bullish indicator that adds optimism before the earnings release.

Seeking Alpha

Another reason to be bullish is VEEV’s historically strong performance against consensus estimates. According to the earnings surprise record, VEEV has never missed revenue or EPS consensus estimates over the last sixteen quarters. Such stability in delivering positive surprises suggests the management’s ability to plan and execute.

My optimism is also backed by recent reports from reputable names on Wall Street. For example, two months ago BofA Securities analysts included VEEV in their list of the “best of breed’ stocks for 3Q2024. The list also includes such AI superstars like Nvidia (NVDA), AMD (AMD), and Palantir (PLTR).

TrendSpider

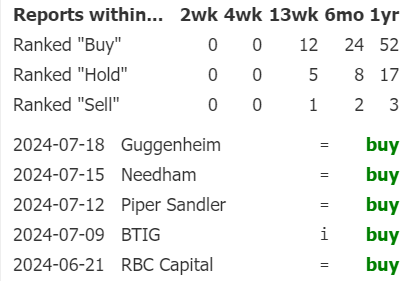

VEEV also received “Buy” rating from other reputable analysts like Guggenheim, Needham, Piper Sandler, BTIG, and RBC capital over the last few months after the Q1 earnings release.

To conclude, the fundamentals mix looks robust. We saw a massive growth in revenue and EPS in Q1, which is expected to remain robust in Q2. The company has a flawless earnings surprise history over the last sixteen quarters and Wall Street analysts are quite optimistic. The company’s fortress financial position means that VEEV is well-equipped to make strong strategic moves that boost shareholders’ value.

Valuation update

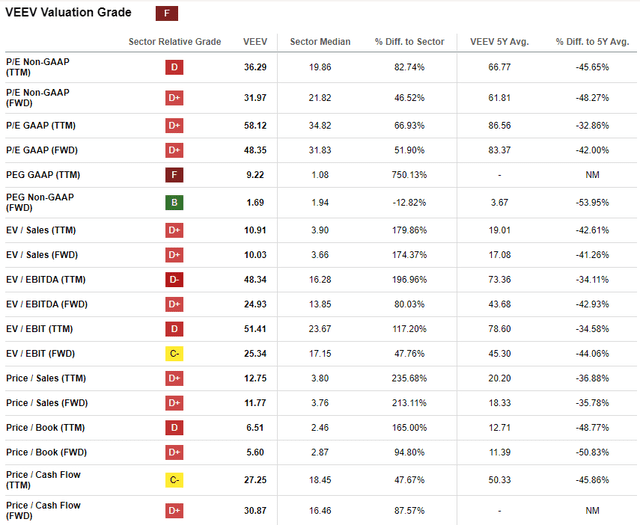

VEEV’s price appreciated by 3.5% YTD, notably underperforming the broader U.S. stock market. The stock has the lowest possible “F” valuation grade from Seeking Alpha Quant. This is because VEEV’s valuation ratios are far higher than the sector median across the board. On the other hand, it is crucial to emphasize that VEEV demonstrates an “A+” profitability and solid growth across key financial metrics. Therefore, comparing current valuation multiples with Veeva’s historical averages would be more proper. From this point of view, the stock looks attractively valued as most of the ratios are 30%-50% below the last five years’ averages.

Seeking Alpha

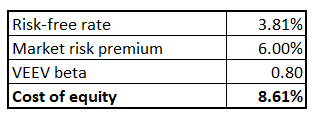

Looking only at valuation ratios is insufficient, meaning that I must simulate the discounted cash flow [DCF] model as well. The discount rate I will use for my DCF will be the company’s 8.61% cost of equity calculated under with the CAPM approach below.

Author’s calculations

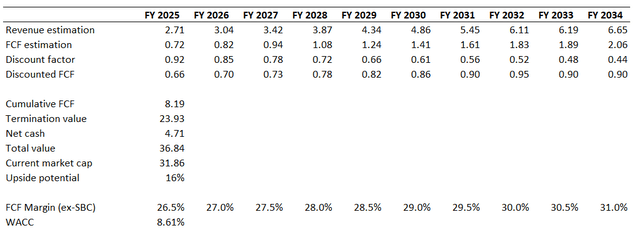

Consensus revenue estimates are available for the next decade, projecting a 10% CAGR, which I consider fair enough. I use a 26.5% TTM FCF ex-SBC margin and expect 50 basis points yearly expansion due to the projected confident growth in EPS. I also add the company’s massive $4.71 billion net cash position to VEEV’s fair value.

Author’s calculations

The business’s fair value is $36.8 billion, meaning there is a 16% upside potential. I find such a valuation compelling for a profitability and growth star like VEEV.

Risks update

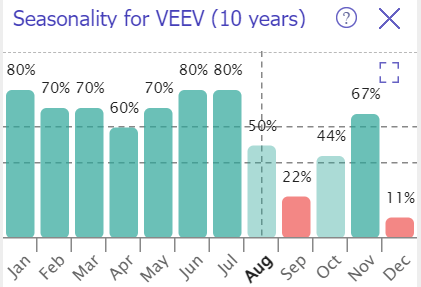

Any stock’s seasonality trends are important for me and VEEV is not an exception. The below bar chart suggests that VEEV historically performs much weaker in the second part of a year. Moreover, September was negative in 78% cases over the last ten years. Investors should be aware about this warning trend and be ready to dollar average their positions in case of a pullback.

TrendSpider

The company generates substantial portion of its sales outside the U.S., according to the latest 10-K report. It means that the company faces a set of risks of operating abroad. These risks include significant foreign exchange risks, geopolitical risks, and potential sudden changes in rules and regulations abroad.

VEEV”s latest 10-K report

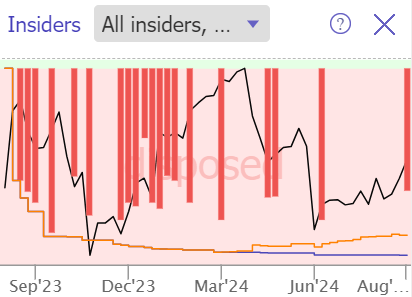

Another warning sign is that despite the stock’s attractive valuation, insiders were only selling the stock over the last twelve months. The below chart suggests that insiders were not buying at all during the last twelve months. On the other hand, selling activities became much less aggressive in 2024 and most of selling relates to 2023.

TrendSpider

Bottom line

To conclude, I believe that there are no fundamental reasons to be less bullish about VEEV. The stock deserves a “Strong buy” rating due to its profitability, strong revenue growth, and solid strategic positioning.

Read the full article here

")

")

")

")