")

")

")

")

Editor’s note: Seeking Alpha is proud to welcome Marek Malina as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

In previous years, investors avoided small companies and focused their attention on large companies. That can be understood. Bigger companies mean more security, and big companies have also benefited more from the excitement around artificial intelligence.

However, I believe that the years of underperformance of smaller stocks, represented by the iShares Russell 2000 ETF (NYSEARCA:IWM), are coming to an end. There are several reasons for this statement.

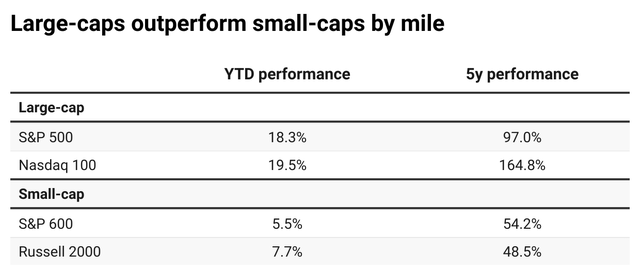

Small caps performance lags large caps

The performance of small-caps thus lags behind. The performance of the S&P 500 index is YTD +18.3% and the Nasdaq 100 even +19.5%. In contrast, the small-cap indices S&P 600 and Russell 2000 have a YTD performance of S&P 600 +5.5% and Russell 2000 +7.7%. The five-year lag is even more pronounced. In 5 years, the S&P 500 grew by +97.0% and the Nasdaq 100 by +164.8%. On the other hand, S&P 600 only by +54.2% and Russell 2000 by +48.5%.

Comparison of indexes performance (Author)

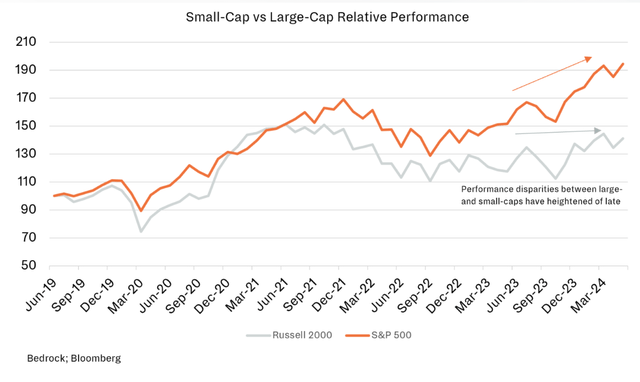

Small vs. Large Cap stocks relative performance (Bedrock, Bloomberg)

Historically cheap

Thanks to the worst relative performance of Russell 20000 against the S&P 500 in 23 years, the valuation of small-caps reached historically low levels. In the last 30 years, we have seen such a low relative valuation of small stocks against large stocks only twice. During the dotcom bubble of 1999 to 2000 and during the financial crisis of 2007.

Why small-caps fall behind?

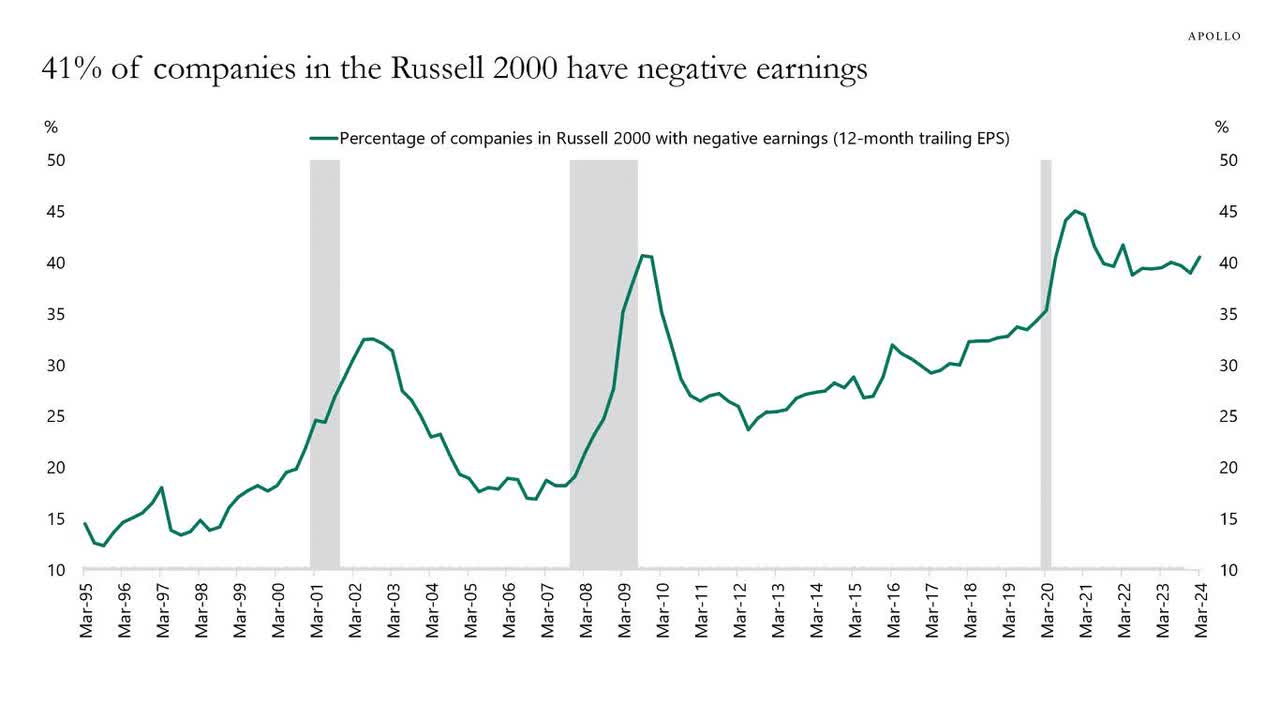

One of the reasons why small-caps lag behind is the very quality of the companies. Of course, you won’t find names like Microsoft or Nvidia in the Russell 2000 or S&P 600 index. The financial position of the companies in the small-cap indexes is weaker and so are the profit margins, which I consider to be one of the main indicators of the quality of companies. Profit margins have grown steadily in large U.S. businesses over the past several decades, but have stagnated with fluctuations in small companies. Even up to 41% of companies in the Russell 2000 index do not generate a regular profit.

41% of Russell 2000 components don´t generate profit (Apollo Academy, Bloomberg)

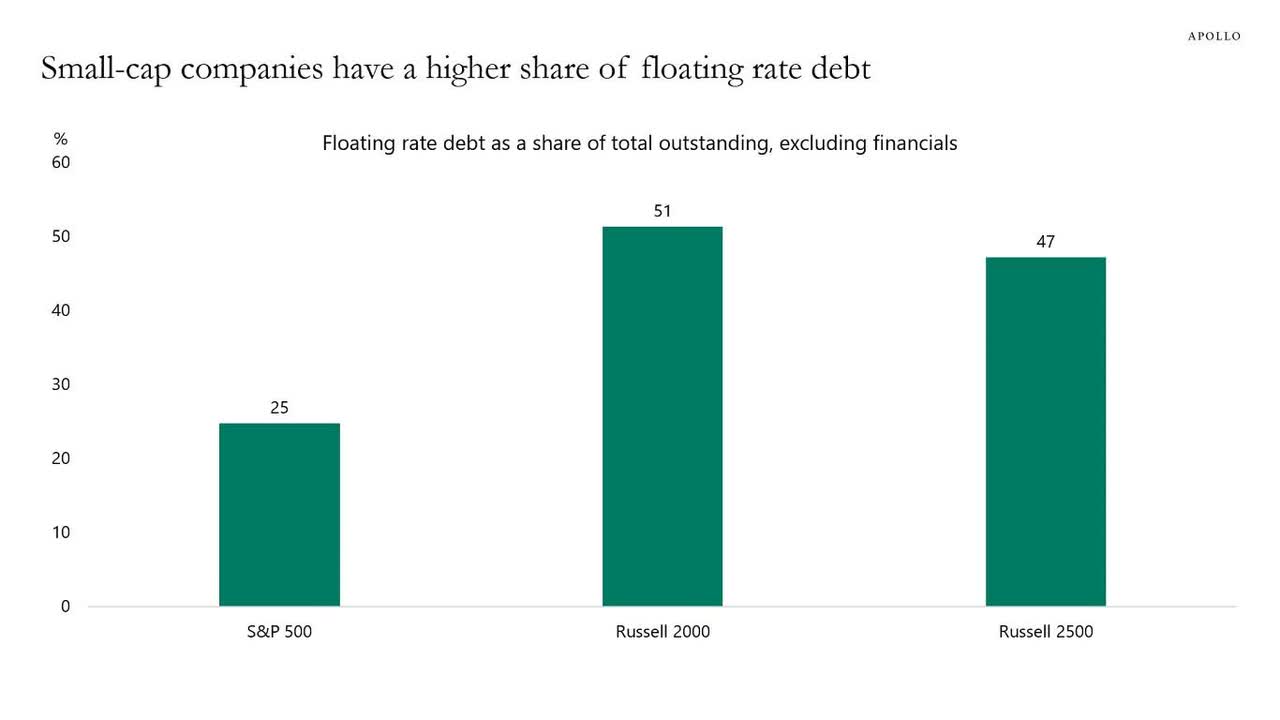

High interest rates also play a key role in the lagging behind of smaller companies. Small-caps are more sensitive to their movements because they are more exposed to foreign financing, in other words, they have higher debt. The average net debt/EBITDA for companies in the Russell 2000 is 3.2x, compared to 1.6x in the S&P 500. Moreover, up to 51% small-caps have a floating interest rate, in the S&P 500 it is only 25%.

41% of small-caps have a float debt (Appolo Academy, Bloomberg)

Last but not least, M&A has historically always increased the performance of smaller companies. Small-caps are often the target of larger companies that decide to buy them. But in recent years, M&A activity has subsided as larger firms have focused on their business and cost savings. This also dragged down the performance of smaller businesses.

Change is around the corner

Many believe, and I am among them, that in the case of small-caps they can see the light at the end of the tunnel. The Fed will start lowering interest rates and, based on market economic data that indicated an economic slowdown in the US, the cycle of easing monetary policy will take a faster decline. By the end of the year, I expect three rate cuts of 25 basis points. The liberalization will continue in 2025 and with it, a large burden will be lifted from the shoulders of smaller businesses today.

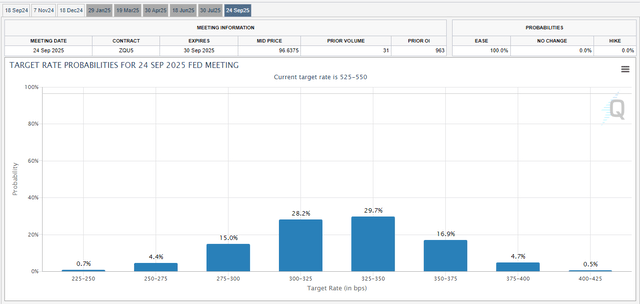

Probability of interest rates in USA in September 2025 (CME FedWatch Tool)

Thus, one year from now, the markets give the highest probability to the scenario that interest rates in the US will be in the range of 3 to 3.5%, which is 200 basis points lower than today. Cheaper financing will be reflected in faster expansion plans of small companies in an effort to maximize their growth potential, but also in the growth of profitability.

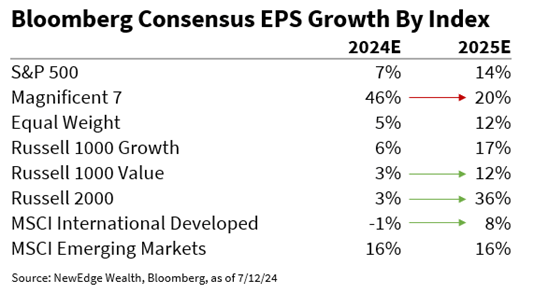

The table below shows consensus earnings estimates for various indices for 2024 and 2025. The Russell 2000’s +3% EPS growth estimate for 2024 earnings trails large cap indices, but note the big expectation for a recovery in earnings growth in 2025 to +36%.

Consensus of EPS growth of major indexes (NewEdge Wealth, Bloomberg)

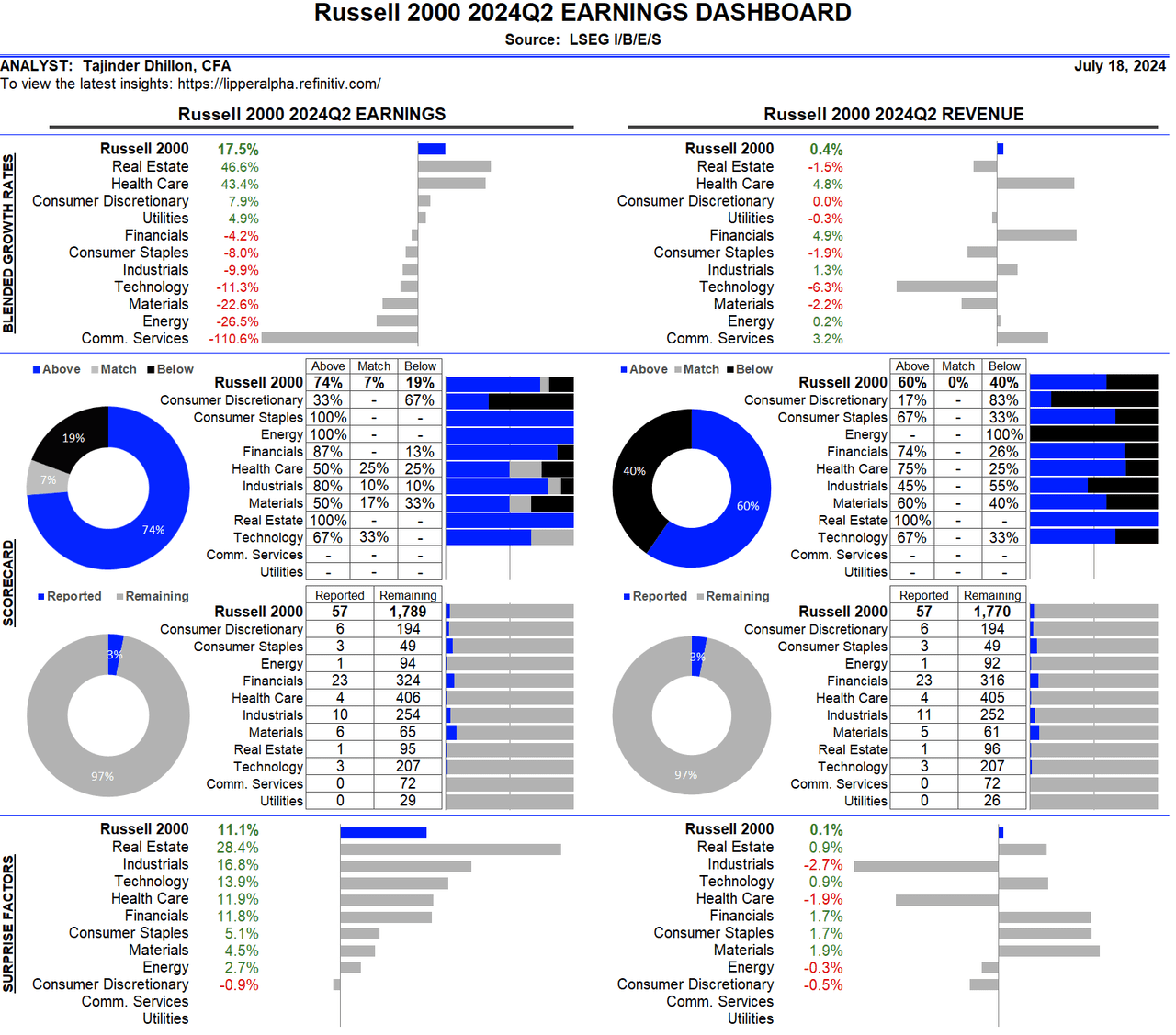

In fact, the profitability of small businesses has already begun to rise. According to data from the London Stock Exchange Group, as of August 15, the year-on-year growth rate of the Russell 2000’s earnings reached 17.5%. This is the highest increase since the fourth quarter of 2022.

Excluding the drag on income from the energy sector, the Russell 2000’s year-over-year earnings growth is 28.3%. Overall, about 60% of small-cap companies that reported their most recent quarterly results beat analysts’ expectations. On the revenue side, 55.9% of these companies beat analysts’ estimates.

Looking ahead, analysts are bullish on small caps. In the third quarter of 2024, the Russell 2000’s earnings are expected to grow by 43% year-over-year, while in the fourth quarter, the growth rate is projected to increase to 73.8% year-over-year.

Russell 200 Q2 24 results (LSEG)

A recovery in the M&A market should also help small-caps return to a growth trajectory. In Q1 24, the M&A market rose by 30% year-on-year. Moreover, deal volumes could rise by as much as 50% in 2024, after the lowest activity in almost two decades in 2023.

At the same time, small-caps can rely on the cooling but still very strong US economy, in which the Russell 2000 generates up to 90% of revenues, in contrast to the S&P 500 with a share of 60%.

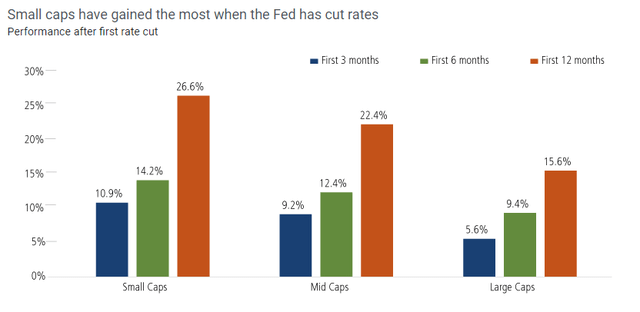

Although past results are no guarantee of future results, history tends to repeat itself often in financial markets. Especially when talking about Fed monetary policy and market reactions. In times of interest rate cuts, small-caps (Russell 2000) tend to outperform mid-caps and high-caps.

Outperformance of small-caps after Fed cuts (Bloomberg)

In July, Russell 2000 already tried one comeback, but it was unsuccessful. In response to the inflation data, the index recorded its best 5-day winning streak since 2020, during which it rose 12%. Subsequently, however, he erased most of the profits. In the last days we can see another attempt and I believe that this time it will be more successful also thanks to strong data from the second quarter.

Although the Russell 2000 cannot match the quality of the S&P 500 or the Nasdaq 100, I believe it can outperform them in the next 18 months.

Finally, I would like to point out that small-cap stocks like the Russell 2000 (IWM) should serve as a diversification piece in a portfolio that can help boost its performance. In times like these, it may make sense to increase the share of small-caps in the portfolio to somewhere between 15-20%. It depends on the investment strategy. However, too much concentration in small stocks can be risky because small-caps are much more volatile and can do worse in the event of economic difficulties.

Read the full article here

")

")

")

")