")

")

")

We last covered British American Tobacco p.l.c. (NYSE:NYSE:BTI) in May, calling it a ‘hybrid value’ opportunity. Since then, the stock has outperformed the S&P 500, prompting me to update our thesis, especially as fundamental changes have emerged in the tobacco industry.

Pearl Gray’s Previous Rating (Seeking Alpha)

Will British American Tobacco’s stock sustain its performance, or is it set for a correction? Here are some of my latest thoughts.

Recent Performance

British American Tobacco has outperformed the SPY ETF (SPY) since the turn of the year. However, it has performed in line with its peers, which is essential to consider before analyzing the company’s idiosyncrasies.

Furthermore, despite tobacco stocks’ solid year-to-date performance, fundamental concerns have emerged within the industry. For example, British American Tobacco, Altria (MO), and Imperial Brands (OTCQX:IMBBY) have all experienced a drop in year-over-year revenue growth, illustrating systematic headwinds. As such, an argument favoring a pullback cannot be neglected.

| Stock | Latest Quarterly Revenue | Y/Y Change |

| British American Tobacco | £12.34B (1H) | -0.8% (Organic) |

| Altria | $5.28 bn | -3% |

| Imperial Brands | £15.36B | -1.3% |

Source: Seeking Alpha (Respective Links Embedded Within The Chart)

Fundamental headwinds exist. However, I think British American Tobacco remains a solid investment; here’s why.

Update On BTI’s Operating Performance

Top-Line

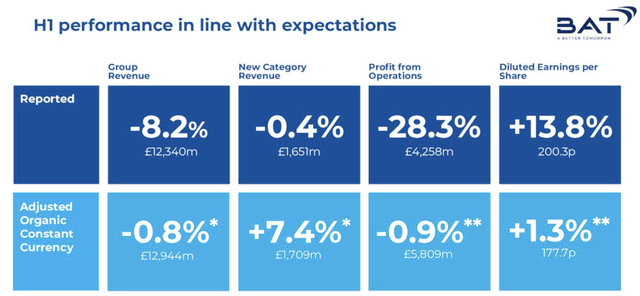

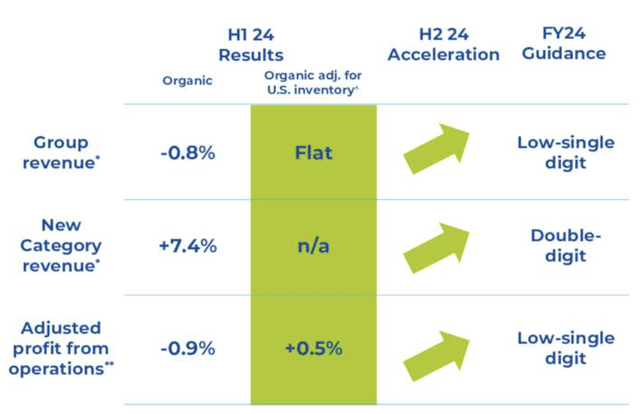

British American Tobacco reported its half-year and quarterly results in July, revealing an 8.2% year-over-year decrease in its half-year revenue. However, the company says most of its nominal revenue decline was due to the sale of its Russian and Belarus segments, and, therefore, core revenue declined by only 0.2% year-over-year.

Headline P&L (British American Tobacco)

Furthermore, British American Tobacco’s organic revenue was impacted by pricing. I see the firm’s current pricing challenges as an economy-wide phenomenon instead of a distinct feature due to disinflation in the U.S. and Euro areas. However, I anticipate the impact will lessen as talks of global interest rate pivots have intensified (this might add a floor to disinflation).

P&L (British American Tobacco)

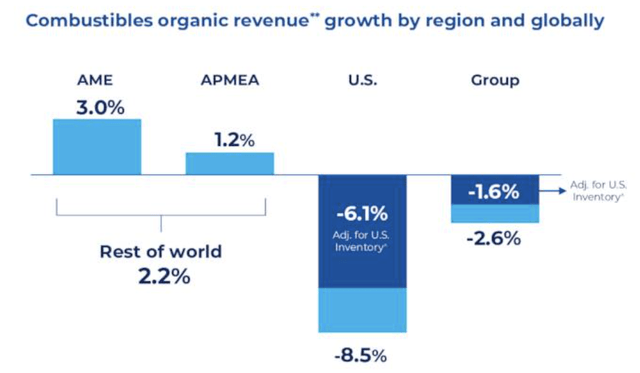

In truth, British American Tobacco’s combustible product sales struggled in H1. Although its volumes persisted, it failed to pass disinflation through to its consumers.

Regardless of its battles, I’m giving the segment leeway because most of its revenue decline was due to a single territory (see the diagram below). Additionally, British American Tobacco has a stellar brand, allowing the segment to normalize when key economic variables settle down. However, I’ll monitor it closely for the remainder of 2024 and update my outlook if additional impactful events occur.

Combustibles (British American Tobacco)

British American Tobacco’s “new categories” segment now spans about 17.9% of the firm’s revenue mix. The segment delivered robust year-over-year performance. However, the business unit’s ex-ante performance is anticipated to eclipse its current growth through Velo and additional product innovation.

New Products Growth (British American Tobacco)

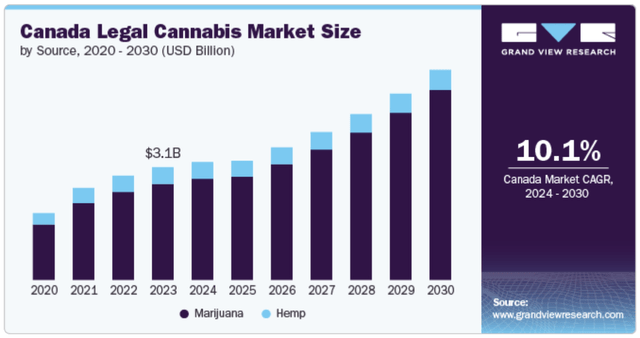

To conclude this segment, I want to shed light on British American Tobacco’s Organigram (OGI) investment. British American Tobacco has agreed to increase its stake in the Canadian cannabis producer to 45% from an initial 19% by investing £74m between January 2024 and January 2025. Although nothing is certain, the Canadian cannabis industry can provide British American Tobacco with diversification benefits, revenue smoothing, added growth, and synergies.

Canadian Cannabis Market Potential CAGR (Grand View Research)

Down-The-line

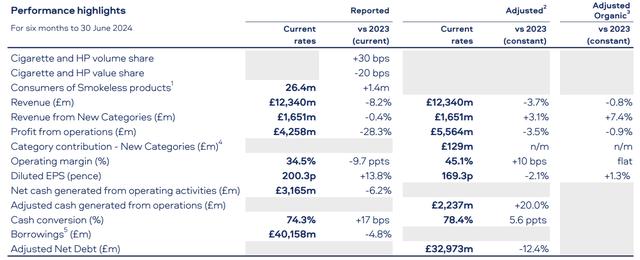

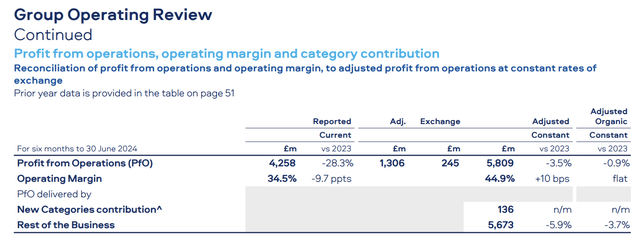

A glance at British American Tobacco’s operating profit margin shows that it achieved a margin of 34.5% in H1 and 44.9% on an adjusted basis. I consider the firm’s operating margins robust, allowing it to deliver residual value to its shareholders while using profits to reinvest in its new products category.

British American Tobacco

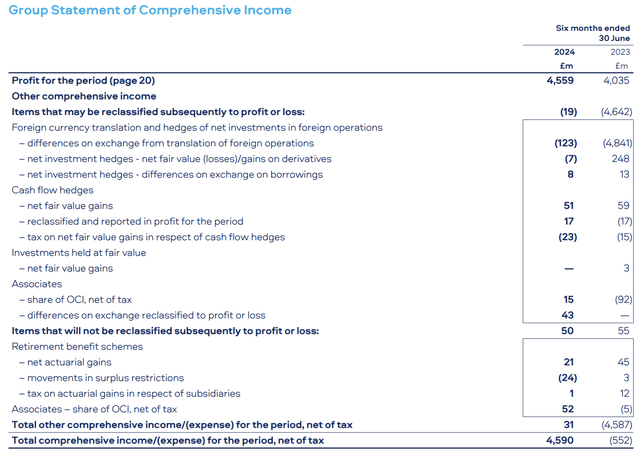

Furthermore, British American Tobbaco’s bottom line seems commendable.

To my knowledge, the company wrote down about $34.5 billion of its U.S. brands earlier this year. Additional write-downs through its Russian and Belarusian operations are possible. However, I see write-downs as a non-core interim risk and believe British American Tobacco’s throughout-the-cycle (or normalized) net profitability will be unabated.

Comprehensive P&L (British American Tobacco)

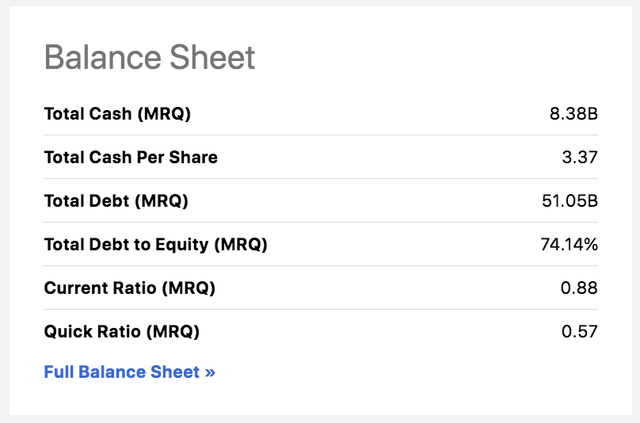

Lastly, for this section, I would like to mention the company’s solid cash position and net debt-to-EBITDA target of between 2x and 2.5x. I believe low debt levels return undistributed value to shareholders and/or allow British American Tobacco to accelerate its new product pivot strategy.

BTI’s Balance Sheet Metrics (Seeking Alpha)

Valuation and Dividends

Multiples

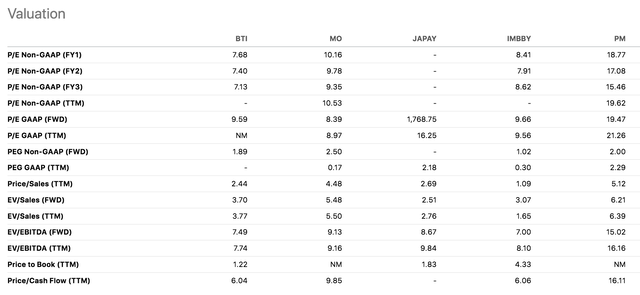

I extrapolated data from Seeking Alpha’s toolkit to conduct a peer-based analysis of British American Tobacco, comparing its valuation metrics to Altria, Philip Morris, Imperial Brands, and Japan Tobacco (OTCPK:JAPAY).

Peers (Seeking Alpha)

In my view, British American Tobacco’s price multiples are low as it is a non-cyclical company with fundamental growth potential. Furthermore, a relative comparison shows that British American Tobacco’s trailing price-to-cash flow ratio is lower than its peers. Although its forward price-to-earnings ratio is in line with its peers, its forward price-to-earnings-growth ratio of 1.89x is best-in-class, communicating compelling bottom-line value.

Peers (Seeking Alpha)

Lastly, I used a P/E expansion formula to examine British American Tobacco’s price in absolute terms. I multiplied the firm’s five-year average forward P/E multiple with Seeking Alpha’s December 2025 earnings-per-share estimate, giving me a price target of around $41 per share.

| Metric | Value |

| EPS Estimate Dec. 2025 | $4.9 |

| 5-Y AVG P/E (Forward) | 8.41x |

| Price Target | $41.2 |

| Stock Price At Close 22/08/2024 | $36.25 |

| Upside Potential | +13.67% |

Sources: Seeking Alpha, Yahoo Finance

Aside: The P/E expansion formula, aka forward P/E valuation, is merely a guidepost; it doesn’t guarantee a stock’s returns.

Dividends

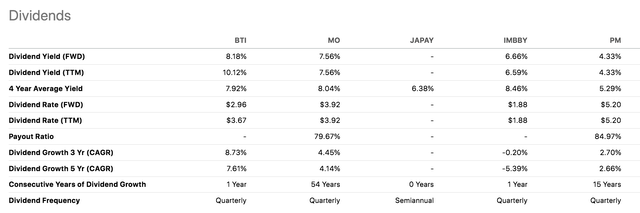

British American Tobacco’s forward dividend yield is around 8.18%, which is higher than that of its peers. In my experience, British American Tobacco has paid consistent dividends and rarely fails to disappoint.

I don’t see any reason to be bearish about British American Tobacco’s dividend prospects, especially if its fundamental developments are considered.

Peers (Seeking Alpha)

Risk Factors

I mentioned a few risks throughout the article. However, I wanted to consolidate a few risk factors in a discreet segment.

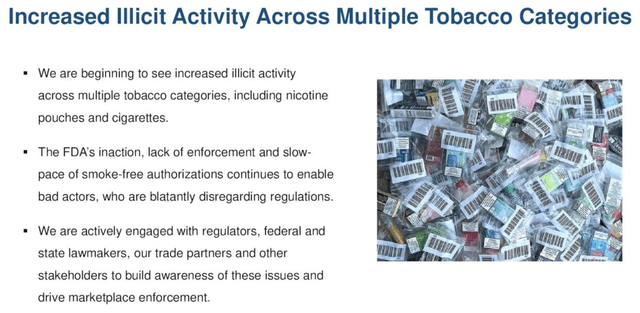

Firstly, tobacco companies are highly susceptible to losing business to illicit vendors, a phenomenon that British American Tobacco experienced to the extent that it scaled down on its South African operations. Another example of illegal risk trade within the industry was recently highlighted by Altria, who cautioned about the rising trade in nicotine pouches and cigarettes.

Altria; Seeking Alpha

Furthermore, as highlighted earlier in the article, British American Tobacco’s stock has surged in recent months, which I deem abnormal for a low-beta (beta of 0.27) stock. So, the question becomes: Is British American Tobacco’s surge overcooked? It’s possible, especially as consumer demand is waning.

Final Word

British American Tobacco’s stock spiked in recent months, so questioning its sustainability is normal.

Based on my findings, British American Tobacco remains undervalued and presents a best-in-class dividend yield. Moreover, its key metrics are supported by fundamental growth through its new products segment.

Despite risks such as slowing interim nominal sales growth and industrywide illicit trade threats, I/we remain optimistic about British American Tobacco’s stock.

Read the full article here

")

")