")

")

")

Introduction

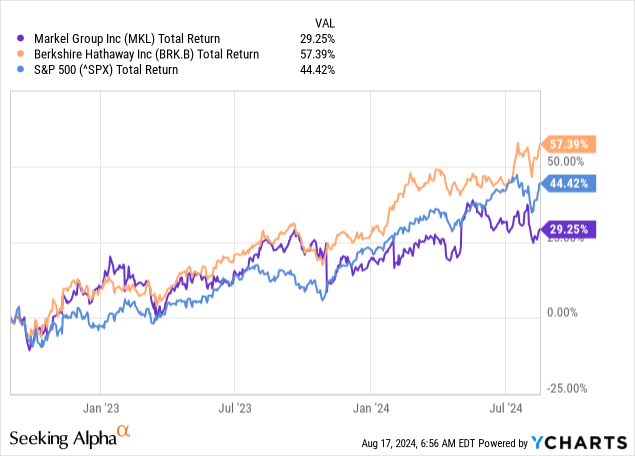

Markel Group Inc. (NYSE:MKL) has performed well since my article in September 2022. In about 2 years, the stock has risen by 29.3%. However, the stock is slightly lagging behind its sector peer Berkshire Hathaway Inc. (BRK.B) and therefore offers an attractive entry point.

Markel’s second quarterly earnings report shows a revenue decline of more than 10% year-on-year. This was mainly due to the lower market value of equity investments. Operationally, Markel performed well, achieving 1.8% year-on-year revenue growth in the insurance segment and 4.5% year-on-year for Markel Ventures. The insurance segment has discontinued underperforming activities, which will strengthen the combined ratio and premium growth in the near future. Investment income increased 31% thanks to high interest rates.

Markel, like Berkshire Hathaway, operates in the insurance sector and invests premiums in a high-quality investment portfolio consisting of stocks, bonds, and companies. Because of its similar activities, Markel is sometimes referred to as the baby Berkshire Hathaway.

I find Markel attractive because of its strong growth characteristics. A small insurer can grow its profits faster than a large insurer. Berkshire Hathaway has fewer of these economies of scale because it is already quite large.

Both Markel and Berkshire Hathaway have their own interesting characteristics and risk profiles, which I discuss in my article.

The Insurance Engine

Markel’s success is spread across 3 growth engines:

- The Insurance Engine.

- The Investment Portfolio.

- Markel Ventures.

The combination of both the insurance business, investment portfolio, and Markel Ventures ensures strong earnings growth in the coming years and assures Markel of a stable revenue stream during turbulent markets.

Markel’s main business is insurance, such as property and casualty insurance, credit and surety products, and other specialized risks, but it also operates in reinsurance. What makes Markel strong is their eye for assessing risk and determining the premium to match. This has resulted in strong profitability and growth in recent years.

Premiums have been growing steadily for years. Consolidated, premiums increased at a CAGR of 12% over the past 4 years to $8.3 billion by the end of 2023. Yet premiums are not rising as fast as expected. In the second quarter, they increased by only 2%.

This was mainly due to the discontinued intellectual property protection insurance products. Internationally, Markel performed particularly strongly with a premium growth of 8% and a combined ratio of less than 80%.

The combined ratio increased by 1% quarter-on-quarter due to higher attritional loss ratios on the US professional liability and general liability product lines, but also losses on the intellectual property protection products (which have now been discontinued). This will improve Markel’s financial performance in the coming quarters.

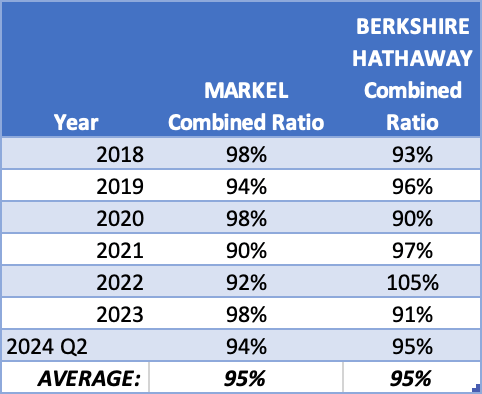

Combined ratio of Markel and Berkshire Hathaway (Annual Reports)

On average, both Berkshire Hathaway and Markel are equally efficient, as the average combined ratio of both is 95%. Markel, on the other hand, is growing much faster. Berkshire Hathaway’s premiums increased only 17% overall from 2018 to 2023, while Markel’s nearly doubled.

The Investment Portfolio

Much of the insurance premiums are reinvested in their investment portfolio, which is managed by Chief Investment Officer Tom Gayner. CIO Tom Gayner’s investment philosophy is very similar to Warren Buffett’s.

Like Warren Buffett, CIO Tom Gayner invests in valuable companies whose profits are rising. He prefers companies that are consistently profitable and attractively priced. As a result, the stock portfolio has grown significantly and contributed significantly to the growth in book value.

Book value per share has risen an average of 8.1% per year over 4 years. Berkshire’s book value has increased more sharply over the same period, averaging 10.5% per year. This is partly due to the high profitability of Berkshire Hathaway’s companies.

The equity portfolio with a total value of $10.2 billion is well diversified across different companies. Berkshire Hathaway is the largest holding. It contains about 12.8% of the total equity portfolio.

|

Stock |

Allocation % |

|

Berkshire Hathaway |

12.8% |

|

Alphabet |

5.0% |

|

Amazon |

3.9% |

|

Brookfield Corp |

3.6% |

|

Home Depot |

3.1% |

|

Deere & Co |

3.1% |

|

Novo Nordisk |

3% |

|

Rest |

65.5% |

The above companies are all growing at 5+% revenue/profit per year and are very healthy financially.

Furthermore, Markel has a fixed income securities portfolio worth $15B. The vast majority of these consists of U.S. Treasury Securities (30%) and bonds of states, municipalities, and political subdivisions (25%). Markel’s bond portfolio provides protection in turbulent markets because the coupons paid out are more certain.

Net investment income (interest + dividends earned) rose sharply, 34% year-on-year to $441 million in Q2, driven by higher interest rates that positively impacted the fixed-maturity portfolio. Markel expects yields on fixed-maturity securities to rise as low-yielding securities mature this year and are replaced by higher-yielding securities.

Markel Ventures

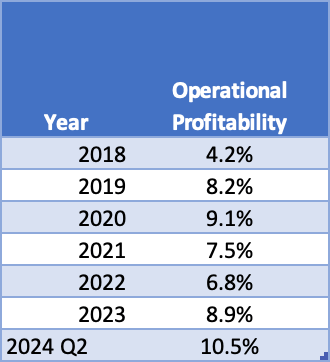

Markel also invests in private equity companies under the name Markel Ventures. Markel Ventures achieved an annual revenue of $5B and an operating profit of $438M (operating profit margin = 8.9%) in 2023. In the second quarter of 2024, the profit margin improved significantly to 10.5%. This was mainly due to a change in accounting:

Prior to 2024, the segment profitability metric for the Markel Ventures segment included amortization of acquired intangible assets. The new metric, as previously described, better aligns with how the chief operating decision maker reviews and assesses the performance of the Markel Ventures segment.

Operational Profitability of Markel (Annual Reports)

Markel Ventures provides a solid foundation as an alternative to volatile markets. Although the markets in the investment portfolio can be volatile, the market does not directly affect the value of Markel Ventures.

Markel can therefore opportunistically deploy capital in acquisitions (insurers or other companies), equity investments, or bond investments. This gives Markel a solid foundation for continued growth in virtually all market conditions.

Markel Ventures’ total revenue increased 4% in the second quarter compared to the same period in 2023, operating income increased 7%.

With the recent acquisition of Valor Environmental, Markel has added a business specializing in erosion control, land services, and more. Valor Environmental will not be consolidated until the third quarter, with $108 million allocated to goodwill and $49 million to intangible assets (current goodwill = $2,738 million, intangible assets = $4,291 million).

Share Buybacks, Valuation Metrics, and Risk Analysis

Markel doesn’t pay a dividend, just like Berkshire Hathaway. But instead, the company buys back its own shares. In 2023, the company bought back $445 million worth of its own shares (about 2% of its market capitalization). Buying back shares is currently a tax-free alternative to paying dividends. And the fewer shares in circulation, the more valuable a stock becomes. Markel aims to maintain the policy of buying back its own shares in the coming years to increase the value of its shares.

In the insurance industry, book value is an important measure of the value of the business. It is important that book value continues to grow in the coming years.

While book value may increase annually, it is also important that the stock price also increases with book value.

What I find quite remarkable is that the book value per share has grown at an average CAGR of 8.1% over the past 5 years, while the share price has grown at an average annual rate of only 6% over the same period. So we can suggest that the shares are more attractively valued than they were a few years ago.

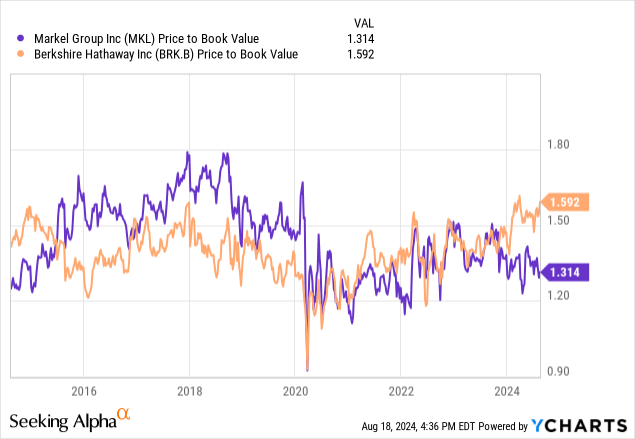

Berkshire Hathaway’s book value has risen faster than Markel’s in recent years (an average of 10.5% versus 8.1% annually). It also trades at a higher price to book value compared to Markel. At first glance, Berkshire Hathaway seems a bit overvalued.

The share price relative to book value has risen sharply for Berkshire Hathaway. However, that does not mean the stock can adjust downward. If book value continues to grow steadily, the price to book value will correct to its average level.

Markel looks a lot rosier. Its price-to-book value is below its 10-year average of 1.44, which represents a 10% discount. And that’s remarkable because Markel is performing exceptionally well operationally. The market has not yet priced in Markel’s strong operating performance in my opinion.

I fear that investors see more risk in Markel than in Berkshire Hathaway because of concerns about a recession. These concerns may have a greater impact on Markel than on Berkshire Hathaway. After all, Berkshire owns a huge amount of safe government bonds that provide solid income even in an economic downturn.

Berkshire Hathaway recently cut its stake in Apple in half. This increased their cash to a hefty $277 billion. I believe Warren Buffett sees little opportunity in this market because of sharply rising stock prices. Berkshire Hathaway can put the money to good use if a big opportunity arises. So Berkshire Hathaway is on the safe side.

In my opinion, Berkshire’s chances are already discounted in the more expensive share price. Markel, on the other hand, is attractively priced.

Timing Is Key

I would also like to compliment Seeking Alpha on the recent addition of the seasonal tables on each ticker page. This gives investors insight into the best month to enter the markets.

Some time ago, I wrote about Celsius Holdings, Inc. (CELH) stock and its seasonality. I wrote then that it was not the right timing to invest, but I was partly wrong (late October is the best time to enter rather than the entire fourth quarter). The seasonal tables from Seeking Alpha show this well. Thanks!

The same goes for Markel and Berkshire Hathaway. These companies can do well operationally, but investors are more enthusiastic at different times of the year. For example, months when extra claims are filed due to severe storms and the like.

Historically, late September is an excellent entry point to invest in Berkshire Hathaway. In September, the stock falls an average of 1.5%. Want to be more sure? Then buy the shares in late October; November is a top month with a high certainty of success (win rate = 80%, and 10-year average of 5%).

The same goes for Markel. Again, September is a bad month. Therefore, choose the end of September as an entry point. Or better: the end of October.

If I have to make a choice to invest in Markel or Berkshire Hathaway, I can’t really choose. Both stocks are attractive to invest in. Markel offers a lot of growth potential because of its smaller size. But is more susceptible to a market crash. Berkshire Hathaway is more resilient to a market crash and offers a higher return on book value. With its large cash position, Berkshire Hathaway can capitalize on potential opportunities. But the price to book value is at its highest point in 10 years.

If Berkshire Hathaway finds a great company at a great price, it is extra beneficial to the price to book value because it can significantly increase book value. And since I do expect some tension in the stock markets in the coming months, Berkshire Hathaway also seems like an excellent choice for me to invest in. Do you buy Markel cheap or do you buy Berkshire Hathaway slightly more expensive, but with lots of opportunity? That’s up to you.

Read the full article here

")

")