")

")

Introduction

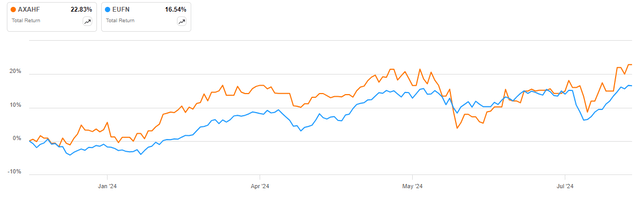

AXA (OTCQX:AXAHF) has outperformed the iShares MSCI Europe Financials ETF (EUFN) so far in 2024, delivering a ~23% total return against the ~17% gain for the benchmark ETF:

AXAHF vs EUFN in 2024 (Seeking Alpha)

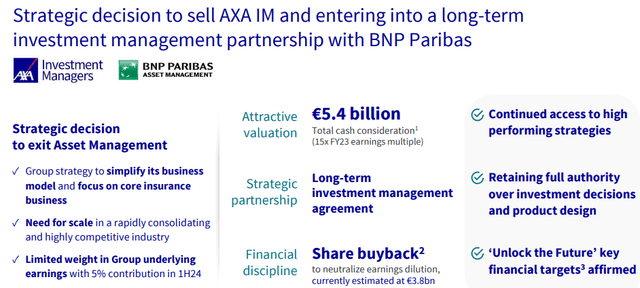

I also covered the shares back in February 2024, arguing they were undervalued in light of the company’s new financial targets and discount relative to its largest European peer Allianz (OTCPK:ALIZF). In today’s article, I will highlight the company’s H1 2024 results and the announced sale of AXA Investment Managers, or AXA IM, to BNP Paribas (OTCQX:BNPQF) for €5.4 billion:

AXA Investment Managers transaction overview (AXA H1 2024 Results Presentation)

I think the transaction makes a lot of sense for AXA given the ~15x underlying earnings multiple – well above the company’s 9x current valuation. Furthermore, AXA’s H1 2024 results showed good progress toward 2026 goals and the discount relative to Allianz is intact. As such, I still think AXA is worth a buy rating.

Company Overview

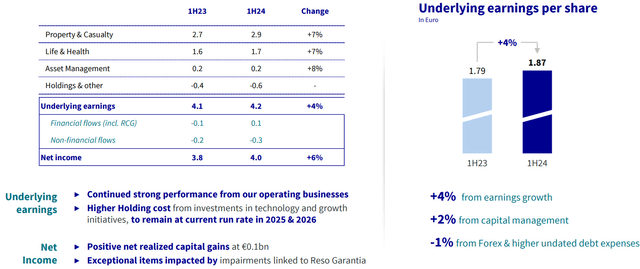

You can access all company results here. Closing of the AXA IM deal is expected in Q2 2025, allowing AXA to focus on its core insurance business, split between Property & Casualty which accounts for 60% of H1 2024 underlying earnings, and Life & Health with a 35% contribution:

Underlying earnings breakdown (AXA H1 2024 Results Presentation)

AXA IM currently contributes 5% of underlying earnings, or about €0.4 billion annually. AXA plans to compensate for the loss in underlying earnings by carrying out a share buyback of €3.8 billion immediately after the AXA IM deal closes.

Operational Overview

Property & Casualty, or P&C, grew revenues by 7% Y/Y in H1 2024, driven by all subsegments. The combined ratio improved by 0.7% Y/Y to 90.2%, helped by a smaller loss ratio and reserve releases. All in all, P&C underlying earnings increased 7% Y/Y in H1 2024.

Life & Health also increased revenue by 7% Y/Y, with an equal contribution from both the Life and Health subsegments. Underlying earnings growth was also 7%, as a 42% Y/Y increase in Health helped offset weakness in Life insurance profitability.

AXA IM delivered 5% Y/Y revenue growth, driven by €7.1 billion in net flows, bringing assets under management to €859 billion. The Cost/Income ratio improved by 1.6% Y/Y to 67.3%, which pushed underlying earnings growth to 8% Y/Y.

On a consolidated basis, H1 2024 revenue increased 7% Y/Y while underlying earnings grew 3% Y/Y. Underlying EPS increased 4% Y/Y to €1.87/share, helped by share buybacks. The return on equity stood at 16.6% in H1 2024 (2023: 14.9%).

AXA also announced the purchase of Nobis Group which will boost the company’s position in Italy to number 4. The €0.5 billion transaction implies a P/E ratio of 11 for Nobis Group after synergies, with closing expected in Q1 2025.

Capital and Comparison with Allianz

The Solvency II ratio stood at 227%, flat relative to year-end 2023, as organic earnings growth was offset by dividends and share repurchases. Debt gearing increased by 1.8% to 22.1% in the first six months of 2024. The Nobis transaction is expected to decrease Solvency II by 1% in Q1 2025.

Even before the sale of AXA IM, AXA remains better capitalized than Allianz, which ended H1 2024 with a Solvency II ratio of 206%:

| IndicatorCompany | AXA | Allianz |

| Solvency II, H1 2024 | 227% | 206% |

| Underlying ROE, H1 2024 | 16.6% | 17.5% |

| P/E, August 2024 | 9 | 10.9 |

Source: Author calculations based on company disclosure

From the table above, we observe that despite its lower profitability in terms of ROE, AXA remains attractively valued relative to Allianz, with the company only trading at a P/E of about 9x.

AXA IM Transaction

I think the deal to sell AXA IM is attractive for AXA, considering the French insurer’s P/E of 9x versus the 15 underlying earnings multiple achieved with the transaction. In essence, the market is currently valuing AXA IM at €3.6 billion, while AXA will bring in an additional €1.8 billion on top of that.

Of course, there is plenty of room for operational optimization at AXA IM, as evident from its cost/income ratio of 67.3% – quite high for an asset management company. For reference, European peer DWS Group, which manages around the same amount in assets has a cost/income ratio of 63.2% and targets a result of below 59% in 2025. So clearly there is ample opportunity for BNP Paribas to improve the profitability of the combined entity.

Risks

AXA is showing robust operating performance and is on track to meet its 2026 targets. As such, aside from the usual risks of unusually large losses which are intrinsic for any insurance company, I would put the main risk in the company’s large exposure to France, at 25% of H1 2024 revenue. As you probably know, following the snap parliamentary elections in 2024, French assets nosedived, with a gradual but incomplete price recovery underway. As such, domestic political developments are likely to continue to impact French stocks. The key consideration for me is whether the far left and the far-right join together to dial back some of Macron’s business-friendly policies.

Conclusion

AXA delivered robust H1 2024 results and is on track to unlock significant value from its AXA IM transaction with BNP Paribas. Given the strong capital position and consistent discount relative to Allianz, coupled with potential share buybacks early next year, I am confident AXA will continue to outperform its European financial peers. As such, I reiterate my buy rating.

Thank you for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")