")

")

")

Many dividend stocks remain a great place to be despite recent uncertainty around the pace of rate cuts. That can especially be true for those companies that have inflation-protected revenue streams, durable contracts, and strong balance sheets.

This brings me to Kinder Morgan (NYSE:KMI), which checks those aforementioned boxes and more, all while paying a decent yield above 5%. I last covered KMI in April, highlighting its attractive valuation and forward growth opportunities.

I should probably have bought more at the time, as the stock has given investors a 17% total return since my last piece, beating the 7% rise in the S&P 500 (SPY) over the same timeframe.

In this article, I revisit KMI to discuss its recent business performance and why KMI remains a ‘buy right hold tight’ stock at the present valuation for income and growth, so let’s get started!

KMI: Still A Great Bargain At 7x Price-To-Cash Flow

Kinder Morgan remains one of my top picks in the midstream energy space for a number of reasons. This includes its moat-worthy presence of 66K miles of natural gas pipelines that traverse the U.S., moving ~40% of the country’s natural gas production. Other factors include the following:

- Working storage of 702 bcf, representing 15% of U.S. natural gas capacity

- 9,500 miles of refined products and crude pipelines

- 139 oil terminals and 135 mmbbl of total liquids storage capacity

- 1,500 miles of CO2 pipelines

- Growing renewable natural gas production capacity

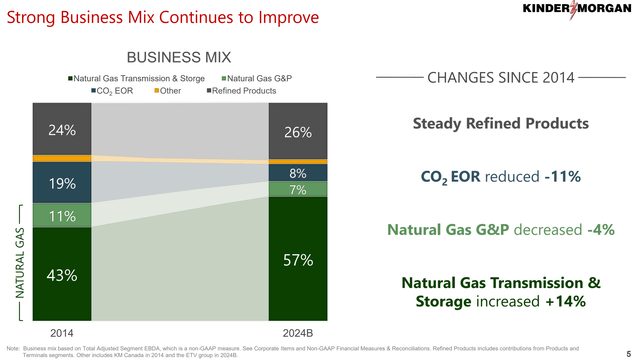

KMI’s business mix has evolved over the past 10 years to include more natural gas, which is cleaner burning than other fossil fuels and is a more reliable energy source than intermittent sources of renewable energy like sun and wind. As shown below, natural gas now makes up 64% of KMI’s EBDA, up from 54% 10 years ago.

Investor Presentation

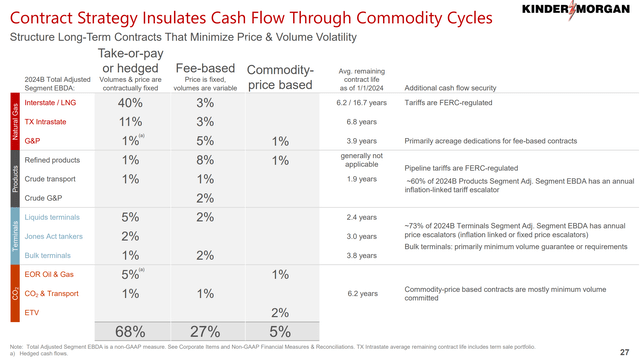

Moreover, KMI enjoys mostly steady earnings as it only has 5% exposure to commodity prices with the remaining 95% being take-or-pay/hedged or fee-based. Plus, over half of EBDA in the products and terminals segment have inflation or fixed price escalators, as shown below.

Investor Presentation

Meanwhile, KMI continues to execute well, with distributable cash flow per share growing by 2% YoY to $0.49 during Q2 2024. Adjusted EBITDA also grew by 4%, driven by growth in the natural gas segment and two refined products segments.

Natural gas gathering volumes were up 10% YoY during Q2, driven by Haynesville and Eagle Ford volumes, and KMI is seeing strong demand coming from utilities and the data center segment.

Management is guiding for a robust 8% increase in both Adjusted EBITDA and DCF per share this year. Longer term KMI sees significant project opportunities across its gas pipeline network to expand transportation capacity and storage capacity.

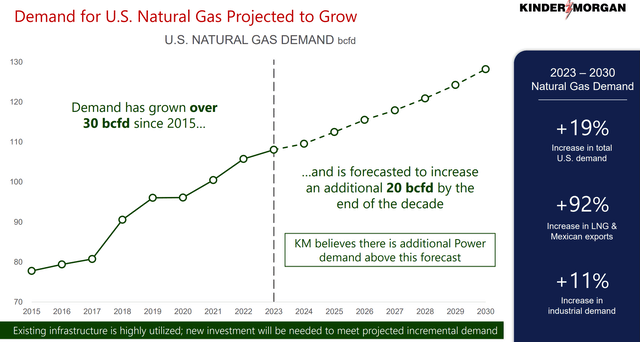

As shown below, demand for natural gas is projected to grow through the end of this decade with a 19% increase in total U.S. demand and 92% increase in LNG and Mexican exports between 2023 and the end of this decade.

Investor Presentation

As a result of increased demand on the horizon, KMI’s project backlog grew by $1.9 billion during the second quarter alone to $5.2 billion total. This includes the South System 4 Expansion project that’s designed to increase gas capacity by 1.2 Bcf per day. Management expects for this project, upon completion, to meet the growing power demand in the Southeastern markets.

Moreover, data centers are expected to be another underlying growth driver for the company, as noted during the recent conference call:

In Texas, the largest power market in the US, ERCOT now predicts the state will need 152 gigawatts of power generation by 2030. That’s a 78% increase from 2023’s peak power demand of about 85 gigawatts. This new estimate is up from last year’s estimate of 111 gigawatts for 2030.

Other anecdotal evidence also supports a vigorous growth scenario. For example, one report indicates that Amazon alone is expected to add over 200 data centers in the next several years, consistent with the large expansions being undertaken by other tech companies chasing the need to service AI demand.

Meanwhile, KMI sports a BBB investment grade credit rating from S&P and management expects to achieve a net debt to adjusted EBITDA ratio of 3.9x by the end of this year, down from 4.2x at the end of 2023.

At the same time, KMI expects to return $2.6 billion in capital through dividends this year, up from $2.5 billion last year. The stock currently yields a respectable 5.5%. The dividend is well-covered by a 59% payout ratio, based on the aforementioned $0.49 DCF per share generated in Q2.

Risks to KMI include commodity price volatility. While most of KMI’s cash flows are fee-based, low prices may not make it viable for some producers to utilize KMI’s services. In addition, economic uncertainty may reduce demand from end markets and a faster than expected ramp-up in renewable energy could result in displacement of traditional fossil fuel sources.

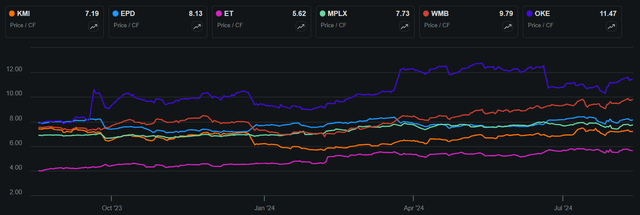

Lastly, while KMI is no longer cheap at the current price of $21.00, it’s not expensive, either, at a Price-to-Cash Flow of 7.2x. As shown below, this sits in the lower half of KMI’s trading range of 6-10x over the past 5 years.

KMI P/CF 5-Yr Trend (Seeking Alpha)

KMI also compares favorably to peers Enterprise Products Partners (EPD), MPLX LP (MPLX), Williams Companies (WMB) and Oneok (OKE), which carry P/CF ratios in the 7.7 to 11.5x range. KMI is more expensive than only Energy Transfer’s (ET) 5.6x P/CF.

KMI vs Peers P/CF (Seeking Alpha)

With a 5.5% dividend yield and my expectations for it to be able to achieve mid to high single digit distributable cash flow per share, KMI could deliver market-beating returns from here. These forward growth expectations are more or less in line with the aforementioned management guidance for this year and analyst estimates.

Investor Takeaway

Kinder Morgan remains a great potential wealth compounder for those seeking both income and growth in the midstream energy space. With a robust infrastructure portfolio, KMI is well-positioned to benefit from increasing natural gas demand and the expansion of its project backlog.

The company’s predominantly fee-based revenue model, inflation-protected contracts, and investment-grade credit rating further enhance its appeal. Although KMI’s stock is not as cheap as it was earlier this year, its reasonable valuation, combined with a well-covered 5.5% dividend yield and expected growth in distributable cash flow, suggests potential for market-beating returns, making it a buy-and-hold stock for long-term investors.

Read the full article here

")

")