")

Introduction

Albemarle Corporation (NYSE:ALB) is the world leader in production of lithium and lithium derivatives, operating over 25 production facilities around the world. Albemarle purchases lithium concentrates from Windfield Holdings, a JV that it owns 49% of. Windfield Holdings operates the Greenbushes Mine, in Australia. Albemarle also has other sources of lithium, such as Wodgina hard rock lithium mine, in Australia as well, that Albemarle owns 50% of the parent company, MARBL Lithium JV. There are other, less significant sources, such as ponds at Salar de Atacama, in Chile, and undeveloped mineral rights in Argentina and in Kings Mountain, North Carolina.

For a much more in-depth overview of the company’s business and history, please refer to my first article on Albemarle.

As a proxy for lithium prices throughout the article, I use the Lithium Carbonate 99.5%Min China Spot.

2Q24 Financials

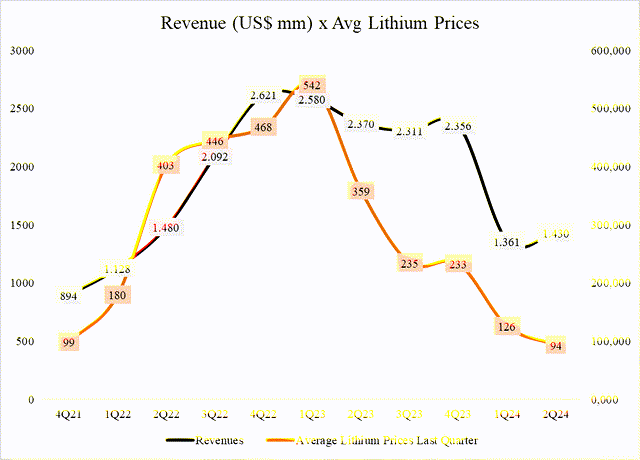

Revenues improved slightly, despite lower lithium prices.

Revenue (US$ mm) and Average Lithium Prices (Past quarter) (Company Filings, Author)

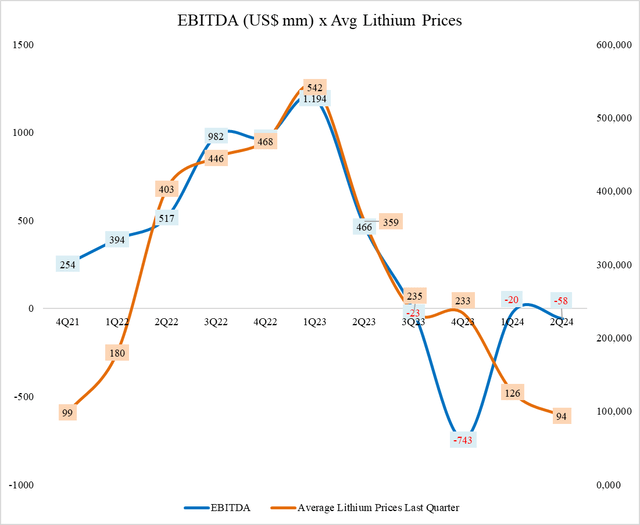

EBITDA remains negative, however.

EBITDA (US$ mm) and Average Lithium Prices (Past quarter) (Company Filings, Author)

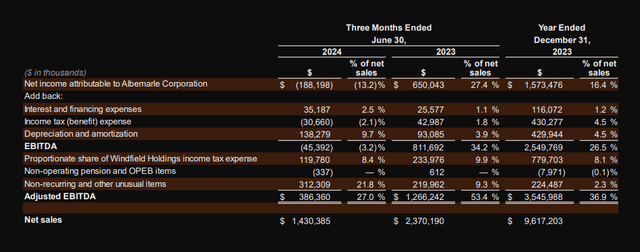

It’s important to note that the company’s own Adj. EBITDA is a very different number, as management feels this is the best way to represent the company’s operations.

Albemarle’s Adj. EBITDA (Company Filings)

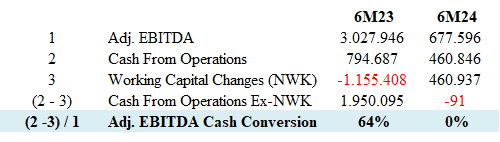

The company adds back almost 30% of revenue (8.4% + 21.8%) to arrive at that adjusted EBITDA. The best technique, in my opinion, to understand if the adjustments make sense, is to compare the adjusted EBITDA to Cash From Operations (Ex-Working Capital Changes).

Adj. EBITDA Cash Flow Conversion (Company Filings, Author)

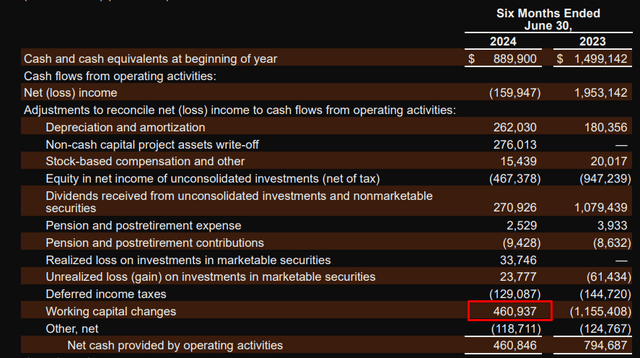

As you can see in the image above, while in 2023 the company had a strong conversion of 64% (adjusted EBITDA into Cash Flow), in 2024 that conversion is not there anymore. That’s because most of the operational cash flow in 2024 came from working capital changes.

Cash From Operations (Company Filings)

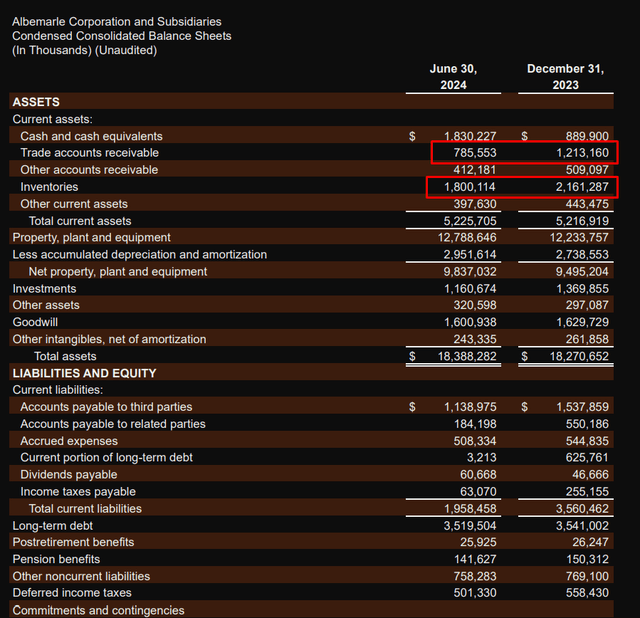

Looking at the balance sheet, we can see that most of the cash must have come from diminished accounts receivable and inventory.

Balance Sheet (Company Filings)

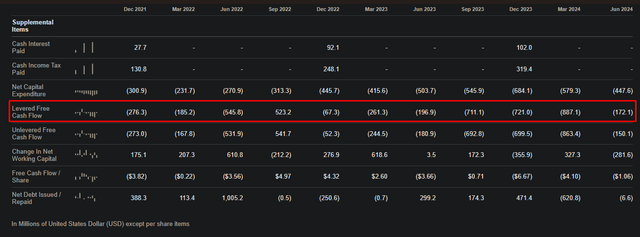

Adjusted or not, the bottom line is that the company isn’t generating free cash flow, being negative at almost every quarter (with the exception of the one ending on September 2022):

Albemarle’s Free Cash Flow (Seeking Alpha)

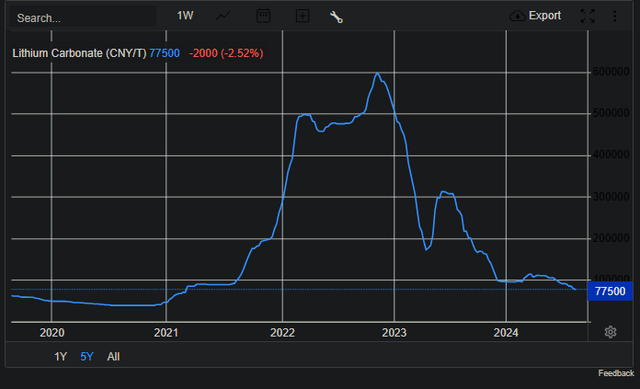

Lithium prices continue plunging.

Lithium carbonate prices. (Trading Economics)

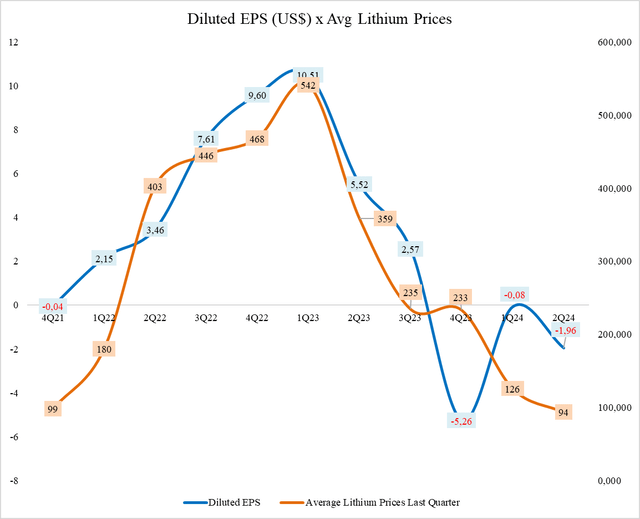

Given the company’s history and lithium prices, I find it very difficult for Albemarle to be able to generate a positive, non-adjusted EBITDA. More concerning is the fact that the company struggles so much with generating free cash flow. It doesn’t matter how good your adjusted EBITDA is, at the end of the day, cash flow is what really matters. Naturally, the company’s profitability is extremely negative.

Diluted EPS (US$), average lithium prices (Company Filings, Author)

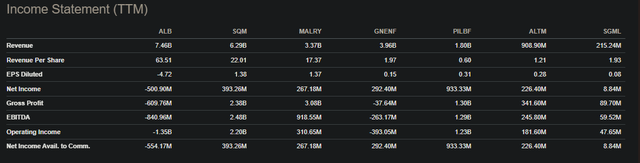

The peer companies I use to compare ALB to are: SQM, MALRY, GNENF, PILBF, ALTM, and SGML. Among them, SQM is probably the closest in size. Unlike Albemarle, SQM has positive EBITDA and Net Income numbers.

Income Statement (TTM) peer comparison (Seeking Alpha)

And while all companies burned cash in the past year (showing a negative Levered Free Cash Flow), the magnitude of Albemarle’s cash burn is unmatched by its peers at negative US$ 2.5B

Cash Flow Statement (TTM) peer comparison (Seeking Alpha)

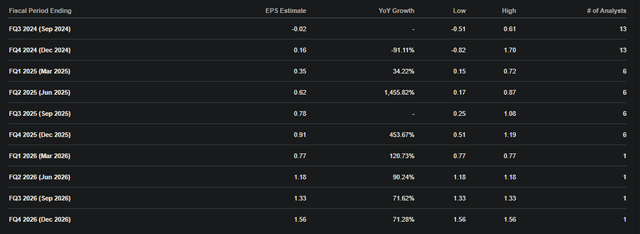

Despite all this, the market is still pricing in a recovery in lithium prices. You can see that by the market consensus earnings expectations, which are positive post 3Q24:

Earnings Expectations (Seeking Alpha)

Current lithium prices are in the range of 70-80. The last time Albemarle had a positive EPS, lithium prices were around 230. I think it’s very unlikely for lithium prices to triple within the next six months for those expectations to realize. Either an extreme bull market in lithium will begin extremely soon, or those numbers will be revised/missed.

Conclusion & Risks

It is my opinion that Albemarle is a company in an extremely difficult position. For it to even have a hope of generating positive FCF, lithium prices would need to get much, much higher. I find commodity prices to be almost impossible to predict, so I wouldn’t bet in such a strong recovery. If you are a strong believer in lithium prices, there are probably other, easier ways to put that thesis in your portfolio, as Albemarle’s cash burn and negative margin makes it extremely unattractive in my opinion.

Read the full article here

")

")