")

")

Iron Mountain Incorporated (NYSE:IRM) is an interesting trust and has good growth prospects. However, this is more than reflected in its valuation, which is difficult to justify at 32x FFO.

Company Overview

Iron Mountain is a Real Estate Investment Trust (“REIT”) specializing in data storage and information management, providing records management, data management solutions, and information destruction services.

It was founded in 1951, and nowadays has more than 240,000 customers in 60 countries around the world, employing about 27,000 people. It has been organized and has operated as a REIT since 2014. Its current market value is about $32 billion, and its shares trade on the New York Stock Exchange.

Its business is organized into two main segments, namely storage and service, which include several product and service offerings, including records management, digital solutions, and data centers. In 2023, the majority of its revenues were generated in the storage segment, representing some 62% of total revenue, while service was responsible for the remaining 38% of revenue.

Iron Mountain has excellent customer diversification given that no single customer accounts for more than 1% of revenue, and its customer retention rate is quite high (approximately 98%). The majority of its revenues are generated from contracted storage rental fees, through long-term agreements that usually have a duration of one to five years.

This means its revenue is highly recurrent and somewhat predictable in the short to medium term, being a supportive factor for a sustainable business model over the long term. Indeed, Iron Mountain is not exposed to economic activity and recessions do not have much impact on its business, which is a very positive business profile within the REIT sector.

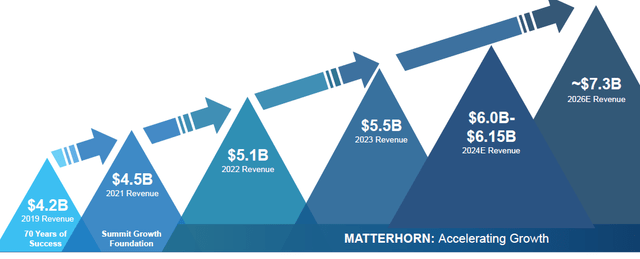

Regarding its growth strategy, the trust has identified three main areas which have structural growth prospects, namely global data center, consumer storage, and asset lifecycle management (ALM), as its major growth engines over the coming years. Iron Mountain established in 2022 a project called Matterhorn, in which the trust intends to orient its business towards technology-driven solutions, focusing particularly on data management and digital transformation solutions for its customers. From a financial perspective, its goal is to gradually increase its revenues over the coming years, from about $5.5 billion in 2023 to some $7.3 billion by 2026, showing that its growth prospects over the medium term are quite good.

Revenue targets (Iron Mountain)

Financial Overview

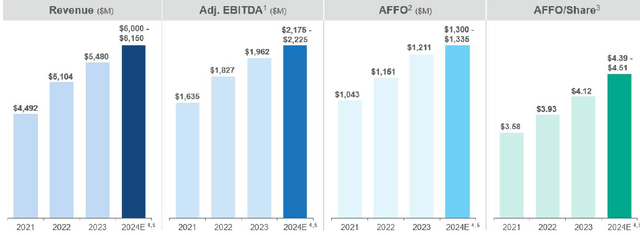

Regarding its financial performance, Iron Mountain has a very good track record given that it has delivered solid business growth over the past few years and expects to maintain this trend in the near future. As shown in the next graph, its revenue and profitability have increased consistently over the past three years, showing that its business has solid fundamentals.

Key metrics (Iron Mountain)

Despite that, Iron Mountain’s occupancy rate is not high, considering that at the end of 2023, its building utilization in records management was 77% and in data management, its occupancy was only 41%. This means the trust has the potential to improve its financial performance organically, as there is considerable vacant space.

This seems to be a reason why Iron Mountain’s strategy has shifted in 2022. The trust wants to transform its business from a local operating model to a more global one, focusing its customer proposition from a product-driven offering into a solution-based sales approach. This should lead to better cross-selling across its operating units and better optimize the trust’s shared services, potentially leading to higher occupancy rates and growing revenue over the medium to long term.

The implementation costs of its growth initiatives are expected to be about $150 million per year, during 2023-2025. This includes restructuring costs, site consolidation, or employee severance costs, which have a negative impact on its profitability in the short term, but should lead to higher business growth and a more sustainable business model over the long term.

Regarding its operating performance, Iron Mountain reported a positive momentum in 2023, as revenues increased by 7.4% YoY to nearly $5.5 billion, and its adjusted EBITDA was $1.96 billion. Its EBITDA margin was stable at 35.8%, as operating expenses also increased in the year due to the inflationary environment, while in “normal” times it would be expected some margin expansion due to positive operating leverage.

By segment, its major growth driver was in the storage rental business, which reported revenues of $3.37 billion, up by 11% YoY, while the service segment increased revenues by only 1.9% YoY to $2.1 billion. In the storage segment, revenue growth was mainly driven by its growing markets and the data center business (+23% YoY to $495 million, representing 9% of its total revenue), a trend that is expected to be maintained in the near future.

This is also supported by the trust’s significant investments in data centers, given that some $964 million of its capital expenditures in 2023 were related to data centers, representing 72% of total capex. This clearly shows that Iron Mountain is investing significantly in data centers, which clearly makes sense as the industry’s growth prospects are supported over the coming years.

Indeed, data center operators have enjoyed strong demand over the past few years and the recent rise of Artificial Intelligence (AI) bodes well for robust demand for data center space in the medium to long term.

While Iron Mountain’s current exposure to data centers is limited, this is expected to change gradually as the company completes its current constructions and potentially makes acquisitions. This is one of the strongest growth drivers for its business in the coming years.

During the first half of 2024, Iron Mountain’s operating performance remained quite positive as the trust reported higher revenue and earnings, beating market expectations by a slight margin over the past couple of quarters.

In Q2 2024, its revenues amounted to $1.53 billion, up by 13% YoY, and its adjusted EBITDA was $544 million (+14% YoY). Its EBITDA margin was 35.4% in the quarter, which was relatively stable compared to previous quarters. By segment, service has been stronger lately, reporting revenues of $1.2 billion in H1 2024 (+17% YoY), while storage revenues were up by 10% YoY to $1.8 billion in the first semester.

This growth was fully organic, through new customer acquisitions and expanding its services into new areas for existing customers. In the data center business, Iron Mountain’s revenues increased by 24% YoY. This was supported by higher pricing and new leasing, which amounted to 97 megawatts during the first half of the year, and has increased its leasing projection to 130 megawatts in 2024, showing that demand for data center space remains strong.

Its adjusted funds from operations (AFFO) increased by 12% YoY in the last quarter to $321 million, and its AFFO per share was $1.08 (+10% YoY). For the full year, the trust expects to report financial metrics closer to the upper level of its guidance range. This is supported by its strong operating momentum that should continue in the sector half of the year and represents business growth in the double-digit area.

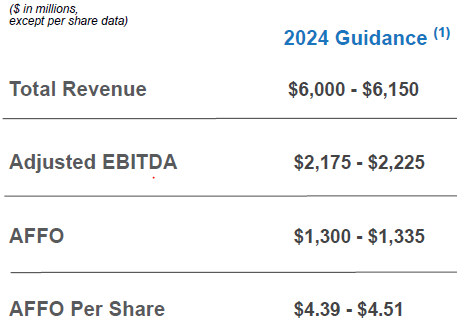

Guidance (Iron Mountain)

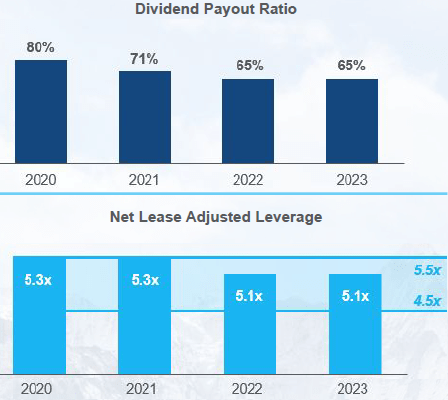

Regarding its balance sheet, Iron Mountain has a comfortable position. This is because it has some $2.3 billion of liquidity and its leverage has been declining in recent quarters, with its net debt-to-EBITDA ratio being 5x in Q2, its lowest level over the past decade.

This means its leverage position is quite good and lower than compared to most of its peers. Thus, IRM does not need to retain much of its organic cash flow generation, being positive both for its capex needs and dividend distributions. Indeed, its leverage ratio target is between 4.5x-5.5x and its dividend payout ratio is in the low to mid-60% (based on AFFO), which allows it to invest in business growth and distribute a good part of its generated funds to shareholders.

Payout and leverage (Iron Mountain)

Reflecting its comfortable balance sheet position, Iron Mountain has recently increased its quarterly dividend by 10%, in line with its AFFO growth, to $0.715 per share. This means its annual dividend is now $2.86 per share, leading to a forward dividend yield of about 2.55%, which is not particularly attractive compared to other REITs.

Regarding its valuation, Iron Mountain is currently trading at some 32x FFO, which is almost double its historical average over the past five years. Compared to its peers, this also represents a significant premium given that its peer group trades at about 18x FFO, a valuation that in my opinion is difficult to justify.

Its multiple expansion has happened mainly over the past year. This is due to the AI hype, which seems hard to justify given that Iron Mountain’s exposure to AI is still limited. Its pure data center peers Digital Realty Trust, Inc. (DLR) and Equinix, Inc. (EQIX) trade at lower multiples (21x FFO and 30x, respectively).

Conclusion

Iron Mountain Incorporated has an interesting business profile and good growth prospects ahead, but this appears to be more than priced into its share price now. Its current high valuation doesn’t leave much upside potential ahead and its income appeal is low, thus, Iron Mountain’s risk-return proposition is not great right now for long-term investors.

Read the full article here

")

")