")

")

Introduction

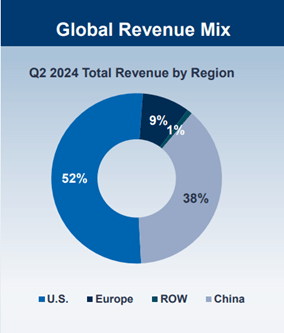

BeiGene (NASDAQ:BGNE), founded by American entrepreneur John V. Oyler in 2010, is a leading global biotech company based in Beijing. The company focuses on discovering and developing innovative drugs for oncology. Currently, BeiGene is a commercial stage company with two approved products: zanubrutinib, a Bruton’s tyrosine kinase (BTK) inhibitor, and tislelizumab, a PD-1 inhibitor. It has also in-licensed several drugs from other multinational corporations and biotech companies to sell in the Chinese market. BeiGene generates 52% sales from the U.S., followed by 38% from China market.

Chart 1: BeiGene’s revenue breakdown by region

Source: Company Presentation

BTKi surprised the market, leading to 2Q eat.

When BeiGene was developing zanubrutinib, I had a low expectation for its peak sales, given that it would be the third BTK inhibitor in the U.S. market. The previous two were J&J’s (JNJ) ibrutinib and AstraZeneca’s (AZN) acalabrutinib, both of which were approved by the FDA as breakthrough therapies. Moreover, these two large pharma have well-established distribution networks in the US. In contrast, BeiGene is only a startup biotech based in China and Zanubrutinib will be its only drug approved in US. Hence, it would be difficult for BeiGene to gain meaningful market share in the US.

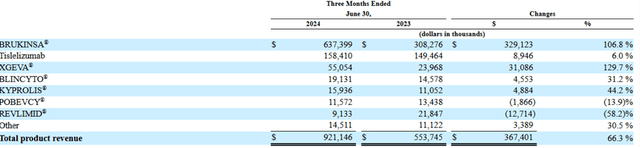

However, the sales ramp-up of zanubrutinib continues to surprise the market. In 2Q24, zanubrutinib global sales grew 107% YOY to USD$637 million. In comparison, ibrutinib and acalabrutinib has only limited growth during the period, indicating zanubrutinib has aggressively gained market share in the US market. BeiGene’s management also stated in its quarterly report that,

“BRUKINSA (zanubrutinib) is emerging as the BTKi class leader in the U.S. in new patient starts across all approved indications, demonstrating the strength of its clinical efficacy and safety data, and is the only BTKi to demonstrate superior efficacy versus ibrutinib in a head-to-head trial. “

Chart 2: BeiGene’s revenue breakdown by product

Source: Company SEC Filing

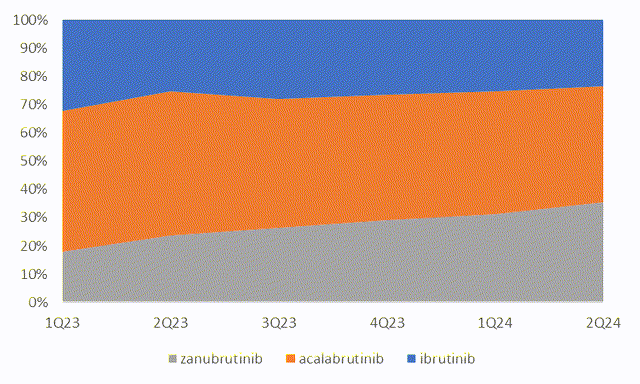

Chart 3: BeiGene’s market share in US continue to climb

Source: Company data

Turned profitable for the first time

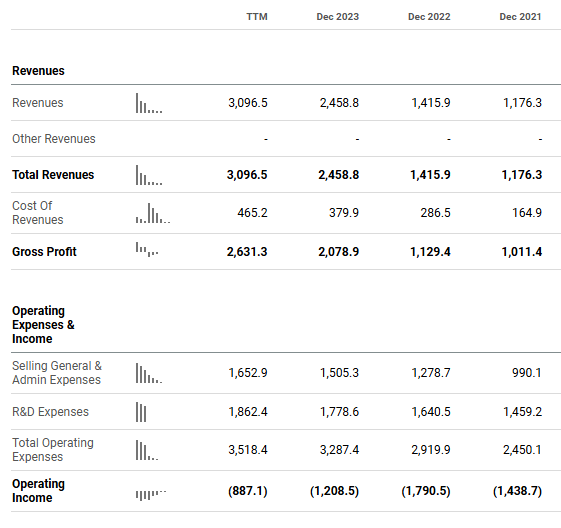

BeiGene had very high R&D spending, as it focused on the global market rather than Chinese market. In 2023, its R&D spending was US$1.8 billion, accounting for 72% of its revenue (See Chart 4 below). To finance its R&D spending, BeiGene had three rounds of equity financing including Hong Kong IPO, private placement to Amgen and China A share IPO. Post COVID, the global market for healthcare companies cooled down significantly. BeiGene also saw its share price dropped by over 50% from its peak. Hence, the market was concerned about whether BeiGene could raise additional capital to continue its R&D.

Chart 4: BeiGene has been aggressive in R&D spending over the past 3 years

Source: Seeking Alpha

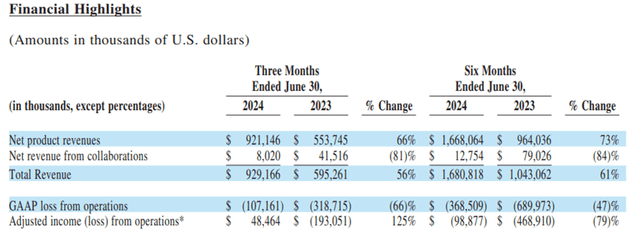

The strong zanubrutinib sales have helped alleviate such concerns. Furthermore, BeiGene has also slowed down the R&D growth to low teen percent annually since 2021. In 2Q24, BeiGene became profitable on a non-GAAP net income basis. The company can finally support itself internally, without the need for funding needs.

Chart 5: BeiGene’s 2Q financial results

Source: Company filing

Expectation on BeiGene’s Pipeline was reset

Over the past three years, BeiGene’s share price has suffered as investors have discounted the value of one of its key pipeline assets, ociperlimab, a TIGIT inhibitor, following a series of failed trials by Roche (OTCQX:RHHBY) and Merck (MRK) Novartis (NVS) has also retreated from its joint development program with BeiGene on TIGIT, indicating a lack of confidence in this drug target. While this was negative to BeiGene, we believe investors’ expectation on TIGIT has been reset and they will begin to focus on its other pipeline assets.

After the setback with TIGIT, BeiGene has also slowed down the development of its other immune checkpoint inhibitors, such as OX40 and TIM3, and refocused on its strong franchise of blood cancer drugs. Its two main assets under development are

1. Sonrotoclax, a BCL-2 inhibitor, which will be used in combination with zanubrutinib to treat first-line treatment-naïve Chronic Lymphocytic Leukemia (1L TN CLL). This combo will also evaluate the potential for time-limited therapy, which will be a key differentiator from existing BTK drugs. This combo will also explore the potential for fixed-duration therapy, which could be a key differentiator from existing BTK drugs. However, the Phase III clinical trial may last until 2032 so we don’t expect any meaningful revenue contribution to BeiGene in the near term.

2. BGB-16673 (BTK CDAC), a first in class BTK degrader. This drug candidate is designed to degrade-wild type BTK and multiple mutant forms, including those that have developed resistance to BTK inhibitors. BeiGene is developing it for BTK resistant patients.

With these two drug candidates, BeiGene will further solidify its leading position in the BTK class of drugs, competing against AstraZeneca’s acalabrutinib and venetoclax combination for first-line treatment-naïve Chronic Lymphocytic Leukemia (1L TN CLL) and Eli Lilly’s non-covalent BTK inhibitor pirtobrutinib for relapsed and refractory (R/R) CLL.

Overhang on IRA Drug Price Cut has been Removed.

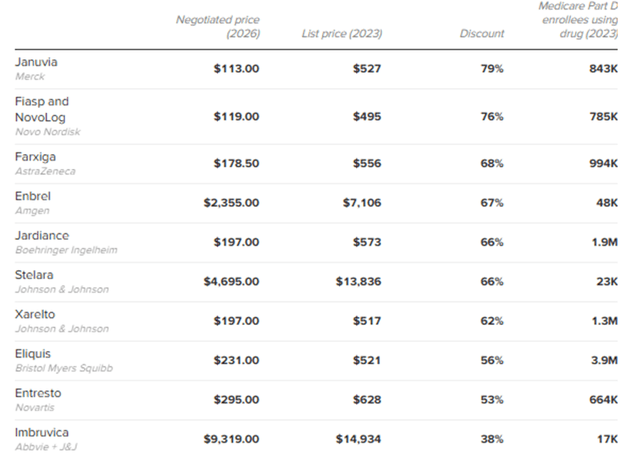

Under the Inflation Reduction Act (IRA), the Centers for Medicare and Medicaid Services (CMS) can identify the highest spending drugs in Medicare Part D, which have been approved by the FDA for over 7 years for chemical drugs and 11 years for biologic drugs, and then set a maximum fair price (MFP) which CMS would be willing to cover. While pharmaceutical companies can make a counterargument on MFP, they will most likely to accept the price or face heavy fines. The new price, once agreed upon, will become effective since January 2026.

The first batch includes 10 drugs, including J&J’s ibrutinib, one of the main competitors of BeiGene’s zanubrutinib

Investors were concerned that if CMS significantly cut the price for ibrutinib, it might impact the pricing of all BTK class drugs, including BeiGene’s zanubrutinib. On August 15th, CMS announced its initial offer for the 10 drugs. Ibrutinib had the mildest gross price cut of 38%, while the rest saw price cuts ranging from 48% to 79% (see table below). If pharmaceutical company accepted the offer, it will also stop paying mandatory rebates to Medicare. Hence the total impact on pharmaceutical net price would be lower than the gross price cut. We believe the result has alleviated a key near term overhang on BeiGene, given the price cut Ibrutinib is quite mild.

Chart 6: Prices for first 10 drugs in Medicare negotiations

Source: Centers for Medicare and Medicaid Services

Concluding thoughts

We believe BeiGene offers a favorable risk reward as market expectations regarding BeiGene’s weak pipeline development were priced in, and its valuation has returned to an attractive level. On the other hand, zanubrutinib sales will continue to surprise the market, and is on track to become a leader in BTK class drugs in the US. The company has also achieved breakeven in 2Q, making the business more sustainable in a turbulent market.

Read the full article here

")

")