")

")

Co-authored by Treading Softly.

Rarely do you build something with a desire to see it get destroyed in the future. However, many companies are receiving negative attention for what is called planned obsolescence. Essentially, it is built into their product, they will stop working after a set period. This helps ensure that there will be continued demand for this product because if you liked it, and it stopped working, and you can’t fix it, you have to buy another, thus ensuring the company’s survival.

However, if consumers are aware that a product is designed to expire, they may not value it for its quality or utility, but instead for its expected lifespan. This is why many individuals are willing to pay more for well-made older products that can be serviced and maintained for a longer time compared to their modern equivalents. How often do we see older cars on the road that are well maintained and cared for, instead of buying a new car that is impossible for such an enthusiast to service and maintain?

When it comes to the market and building my portfolio, my goal is simple. I use my unique Income Method to achieve my passive income goals. I want my portfolio to generate an ever-expanding stream of income into my account. To achieve this, I demand every investment I own to pay me regularly and generously. I do sell and buy to optimize my income stream, but I don’t sell to “unlock” income as many do with non-dividend-paying investments.

Today, I want to look at a company that just hiked my income again. Let’s dive in!

More Income For Your Wallet

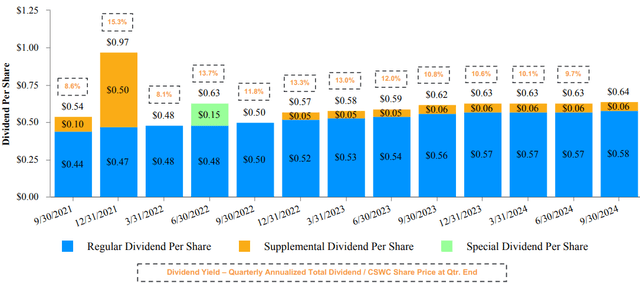

During earnings season, there are often surprises. Capital Southwest Corp (NASDAQ:CSWC), yielding 9.7%, provided us with a very nice surprise — it raised its dividend by another $0.01. CSWC is now paying $0.58/quarter as its “regular” dividend, and is continuing to pay a $0.06 supplemental dividend. At $0.69/share, NII (net investment income) continues to significantly exceed both the regular and supplemental dividends. CSWC continues to reward shareholders with a growing regular dividend, and numerous supplemental and special dividends. Source.

CSWC August 2024 Presentation

CSWC was able to provide large special dividends when interest rates were 0% and, while rates have gone up, has been able to pay regular supplemental dividends. The regular dividend represents the amount that management believes can be expected to be regular and recurring in most economic conditions. For example, if interest rates are cut, the “supplemental” dividend is the portion that is most at risk of being cut or even eliminated. The purpose of the supplement is to distribute the excess that is generated from higher-than-normal interest rates. When buying, keep that in mind. Plan on receiving the regular dividend, and accept the supplements and specials as what they are, supplemental and special. They are the whipped cream and cherries topping of our dividend sundae.

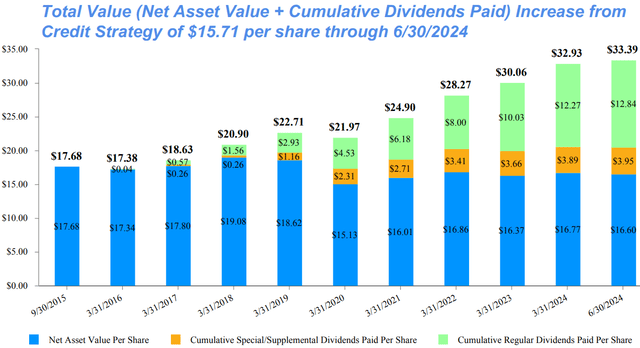

Book value was down slightly to $16.60, about a 1% decline from last quarter. If we look at the big picture, we can see that it is well in line with what we have seen from CSWC over the past several years.

CSWC August 2024 Presentation

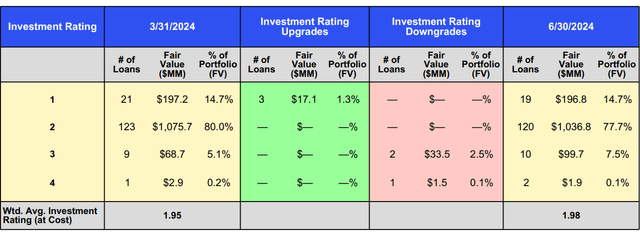

In terms of credit quality, CSWC’s portfolio has held up well.

CSWC August 2024 Presentation

There were three upgrades and three downgrades in the portfolio last quarter. CSWC has only two loans in level 4, their lowest rating, which suggests a high probability of loss. They have 10 loans that are at level 3 which is the bucket for loans that are below expectations and are on their watch list. This is compared to 139 loans that are at their starting level of 2 or are outperforming expectations in level 1.

CSWC is operating at a low level of leverage at only 0.75x debt/equity. Since CSWC tends to lend to smaller companies, we do expect them to maintain a more conservative level of leverage than many peers. However, there is definitely room to leverage up to 0.8x-0.9x.

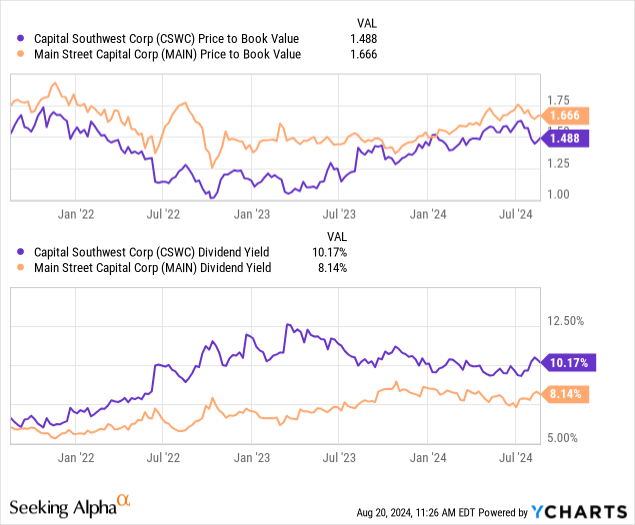

Compared to another premium business development company, or BDC, Main Street Capital (MAIN), CSWC has seen its valuation rise as investors recognize its strengths.

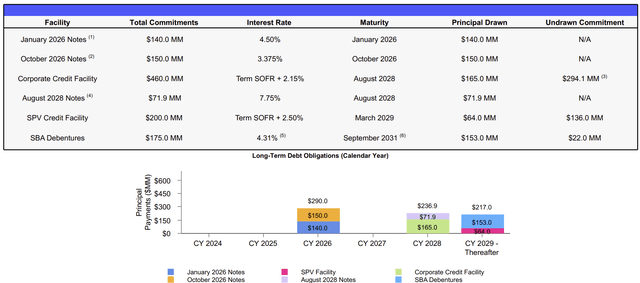

Currently, CSWC is still trading discounted compared to the valuations that we’re seeing MAIN trade for. However, its yield is still far superior. This means that you can buy a more discounted BDC and get a better yield on your price today than buying its more premium traded for peer. Furthermore, when we look deeper into CSWC’s debt profile, we can see that there is no pressing need to manage any maturity until two years from now.

CSWC August 2024 Investor Presentation

This provides a clear runway for CSWC to not have to fiddle with its current leverage and take on new leverage, if desired, during a period of time when interest rates are primed to be cut. Unlike many other BDCs and other companies, such as Sachem Capital (SACH) or B. Riley Financial (RILY), that are forced to manage debt maturities currently in the current high-interest environment, CSWC is set up to have a strong balance sheet. This will be valuable through what could be a turbulent period of a recession.

When we bought CSWC, it was because we viewed it as a company with the potential to become another MAIN. That is, a premium BDC that has proven an ability to keep growing through a wide variety of economic conditions, including the GFC. So far, CSWC has continued to live up to our expectations. With discounted value compared to MAIN, higher yield, and a strong balance sheet going into what could be a recessionary period with low yields on most of their debt, CSWC is a perfect opportunity to hold through a recession.

Conclusion

CSWC has continued to prove itself to be worthy of the “premier BDC” status. While it focuses on smaller companies versus peers like ARCC or MAIN, it has continued to show the ability to trade at a premium to book value and out-earn its dividend, all while rewarding its shareholders with supplemental dividends. As we look towards a recessionary environment, the goal for an intelligent BDC investor should be to own companies that show adept management. In my opinion, CSWC has one of those management teams.

When it comes to retirement, your goal should be to meet those expenses head-on with an overwhelming force of growing income. The income generated by your account should vastly overwhelm and put out the wildfire expenses every single month, allowing you to have a healthy reserve of additional income to draw from as needed. If your portfolio has to be thrown into the fire every single month to meet your needs and your expenses, then perhaps your portfolio is built wrong and unfit for retirement. If your portfolio is a stack of water bottles that you use to try to fend off the fire of your expenses instead of overwhelming them with a recurring stream of income, all you’re doing is throwing away your entire life’s work one month at a time. That’s not something I want any of us to experience because that leaves you increasingly exposed to the dangers and risks of aging.

Would you rather be the retiree who is afraid of getting ill, lest it destroy their nest egg? Or the retiree who knows that their health care will be taken care of by the income stream that they’ve carefully crafted and developed over the years? I would choose the latter, all day, every day.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here

")

")