")

")

")

The Q2 Earnings Season is off to a solid start for the Gold Miners Index (GDX) and gold producers as well as royalty/streaming companies are enjoying record gold prices of $2,300/oz. However, more important than any quarterly figures to be released later this month are resource/reserve statements updated in H1 for most companies, which provide a glimpse into how they are succeeding regarding replacing their mined depletion and how reserves per share are trending. Alamos Gold (NYSE:AGI) was one of the first companies to report its results, which we’ll dig into below:

Alamos Gold Pour – Company Website

All figures are in United States Dollars unless otherwise noted. G/T = grams per tonne (of gold or silver). GEOs = gold-equivalent ounces. AISC refers to all-in sustaining costs.

Total Mineral Reserves & Reserves Per Share

Alamos Gold released its year-end reserve/resource update earlier this year, reporting a 2% increase in gold mineral reserves to ~10.7 million ounces (~201.6 million tonnes at 1.65 G/T of gold). This was complimented by a 1% increase in grades to 1.65 G/T of gold and was driven by growth at Island Gold and Lynn Lake, offset by lower reserve replacement rates at Mulatos and Young-Davidson. However, as we’ll detail later, Alamos will see significant reserve growth at year-end 2024 following its recent acquisition of Magino. In addition, there looks to be further long-term reserve growth in the tank at its Island Gold Complex (Island Gold, Magino) with significant regional potential and near-mine upside at both mines, in addition to reserve upside at Lynn Lake Regional (Burnt Timber, Linkwood). Let’s take a closer look below.

Alamos Gold Gold Mineral Reserves & Depletion – Company Website

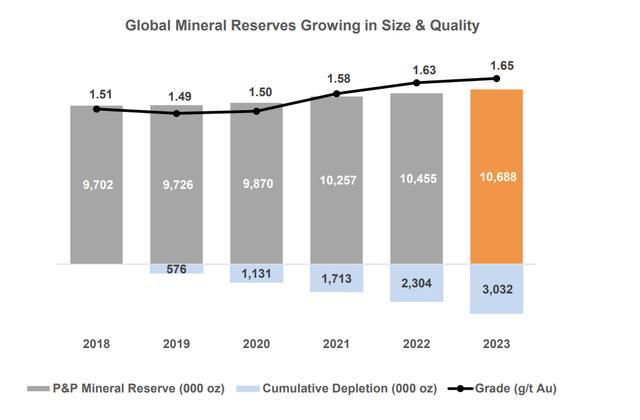

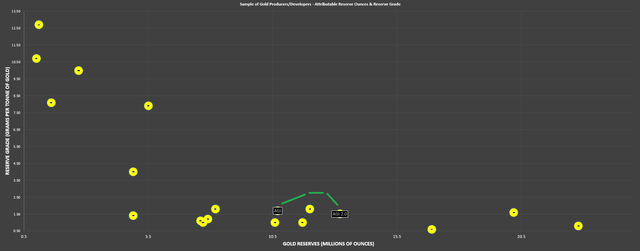

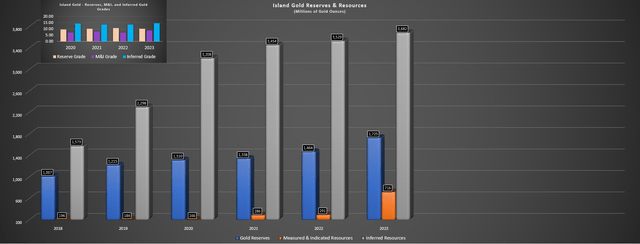

As the chart below highlights, Alamos ended the year with record gold reserves despite significant depletion in 2023 (~730,000 ounces) and has continued to see a steady rise in overall grades. The continued grade improvement has been helped by steady reserve growth at Island Gold and the depletion of lower grade reserves at Mulatos (offset by high-grade reserves at PDA, a new sulphide opportunity at Mulatos). And as highlighted in the below chart that compares several sub-2.5 million ounce producers, Alamos stacks up well from a reserve grade standpoint, ahead of producers with much lower reserve grades like Equinox (EQX), Eldorado Gold (EGO) and Iamgold (IAG).

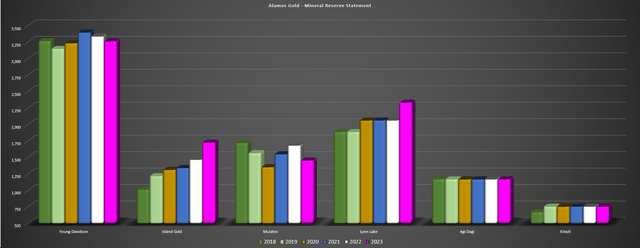

Alamos Mineral Reserves by Asset – Company Filings, Author’s Chart Alamos Gold Reserve Ounces & Reserve Grade – Company Filings, Author’s Chart & Estimates

Some investors might not be impressed with the marginal year-over-year increase (1% increase in tonnes and 1% increase in grades) in reserves, but it’s important to look at the big picture. Ten years ago, Alamos had a ~1.7 million ounce reserve base at 1.16 G/T of gold and a single operating mine (Mulatos) with a seven-year mine life. Today, it has four mines (including a top-10 gold mine by grade), an advanced Tier-1 jurisdiction development project, an industry-leading weighted average mine life and will be among the top-five lowest cost producers post-2026. Hence, it has done a phenomenal job of diversifying its operating/development portfolio, significantly increasing its weighted-average mine life and focusing on high-grade/high-margin ounces vs. focusing on a production figure.

The result of this 10-year transformation is that it’s difficult to find a higher-quality producer in the sector today outside of Agnico Eagle Mines (AEM), with Alamos checking all the important boxes when it comes to owning a producer which include the following with emphasis on #5 where Alamos has excelled relative to peers.

1. low jurisdictional risk (~90% of NAV in Canada)

2. a highly diversified portfolio (4 mines, 1 development project)

3. industry-leading margins (sub $1,050/oz post-2027)

4. a strong pipeline (organic growth at Island/Magino + Lynn Lake + PDA)

5. a consistent track record of per share growth

As I’ve stated in past updates, reserve growth is important to provide visibility into future production and cash flow, but most important is reserve per share growth. This is because many investors hold miners to get exposure to gold and avoid seeing their purchasing power erode. However, if gold production, cash flow and gold reserves are steadily rising, but declining on a per share basis, this is a recipe for underperformance and one is better off holding the metal. The reason is that no real value is being created for shareholders given that their ownership percentage of production, reserves, cash flow is shrinking each year as the share count growth outpaces these key metrics. Fortunately, Alamos Gold, like Agnico Eagle, has figured out the proverbial secret sauce to enjoying industry-leading per share growth, with both employing a similar strategy that involves:

1. counter-cyclical M&A with a significant weighting placed on jurisdictional risk and asset quality

2. highly successful exploration campaigns that have led to significant organic resource/reserve growth and extended their mine lives

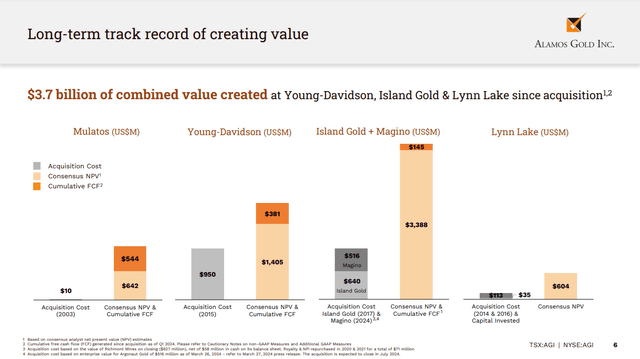

Alamos Gold Track Record Of Value Creation – Company Website

Focusing on acquiring ounces in the ground when there’s a significant valuation disconnect might seem simple, but it’s clearly easier said than done when looking at per share growth among constituents in Alamos’ industry group. And while some have got the counter-cyclical part right, they’ve failed miserably regarding taking risk into the equation, and billions of shares have been issued for ounces that will likely stay in the ground indefinitely. This is due to heightened geopolitical risk, permitting issues and/or a lack of community support, or acquiring orebodies were less robust and/or more challenging/costly to mine than initially expected.

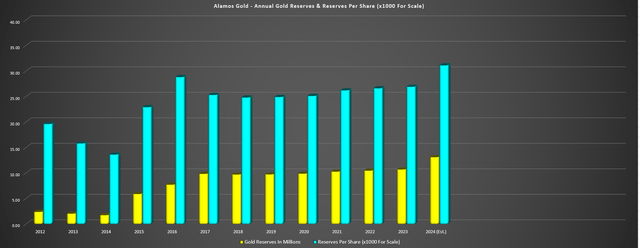

Fortunately, Alamos has executed near flawlessly on this strategy (shown below), with it seeing a consistent trend higher in reserves per share while most of the industry has struggled.

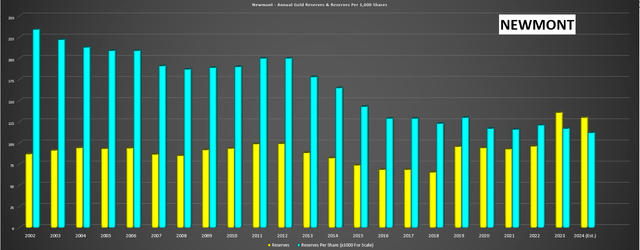

Alamos Gold Annual Gold Reserves & Reserves Per Share – Company Filings, Author’s Chart & Estimates Newmont Annual Gold Reserves & Reserves Per Share – Company Filings, Author’s Chart & Estimates

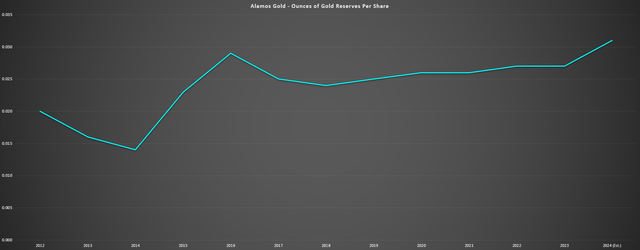

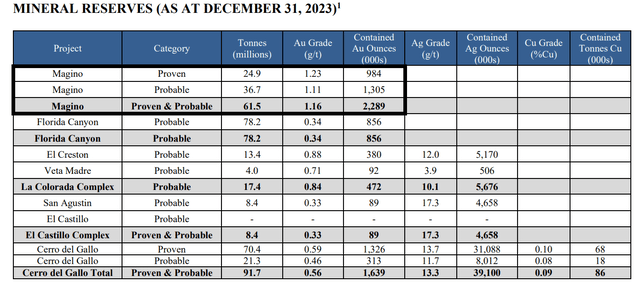

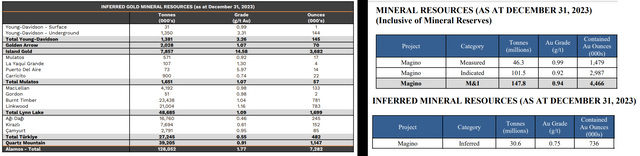

Importantly, while Alamos’ ~70% growth in reserves per share from 2013 to 2023 has trounced its peers, it will see significant growth at year-end 2024. This is because its recently acquired Magino Mine had ~2.29 million ounces of gold at 1.16 G/T of gold as of year-end 2023 and Argonaut has been busy drilling with the aim to add 500,000 to 1.0 million ounces of resources to reserves. Hence, even if we assume moderate depletion on Alamos current portfolio at year-end, incorporate depletion at Magino and add in a conservative 500,000 incremental ounces at Magino (low end of reserve growth target), we should see Alamos total reserves grow to ~13 million ounces at year-end 2024, enabling a significant spike in reserve per share growth.

Alamos Gold Reserves Per Share & Forward Estimates – Company Filings, Author’s Chart & Estimates Magino Mineral Reserves – Argonaut Filings, 2023 AIF

Putting it all together, Alamos reported 2% reserve growth year-over-year while maintaining its extremely conservative $1,400/oz gold price assumption on reserves. However, we should see 20%+ reserve growth at year-end 2024 with Magino moved into reserves and a massive increase in reserve growth per share. And it’s important to highlight that this reserve growth per share was achieved by being extremely disciplined and waiting for Argonaut Gold to run out of runway before making its bid whereas another producer might have been much less patient and seen limited per share growth when acquiring a neighbor.

This is a unique attribute to Alamos Gold, which makes it near unparalleled from a quality standpoint among its producer peers because you can’t buy discipline. And it’s this discipline that is responsible for Alamos’ industry-leading per share returns, with its founder and CEO John McCluskey at the helm for the past two decades. Finally, Alamos will see massive benefits from a tax standpoint medium-term and huge savings from a capex standpoint with it taking over a newly constructed mill & tailings facility next door which is not reflected in reserve per share growth or production per share growth but are very important to investors. Let’s look at Alamos’ mines in more detail:

“With three operations in Northern Ontario in close proximity to each other, we expect to realize increased purchasing power for consumables. We also expect to benefit from Magino’s significant tax pools that can be used to defer any meaningful cash taxes payable in Canada by three years to 2028.”

– Alamos Gold, Q1 2024 Conference Call

Mineral Reserves by Asset

Island Gold

Starting with Alamos’ flagship Island Gold Mine, the mine enjoyed its 11th consecutive year of reserve growth and ended the year with ~1.73 million ounces of gold reserves at 10.3 G/T of gold based on ~5.21 million tonnes of ore. This represented a 23% increase in tonnes offset by a 4% decline in grades, and ultimately resulted in reserves increasing 18% year-over-year (year-end 2022: ~1.46 million ounces of gold). Meanwhile, measured & indicated [M&I] ounces increased materially as well to ~716,000 ounces at 8.73 G/T of gold (year-end 2023: ~291,000 ounces at 7.09 G/T of gold), and inferred ounces saw continued growth at higher grades, ending the year with ~3.68 million ounces at 14.58 G/T of gold.

Island Gold Reserve/Resource Progression & Grades – Company Filings, Author’s Chart

As the chart above highlights, Island Gold has clearly seen phenomenal growth in reserves and resources since Alamos acquired Richmont Mines in 2017 and has added mineral resources at a cost of ~$13/oz over the past five years. For a mine that has the potential to produce at $1,500/oz margins ($2,300/oz gold) post-2026, this is outstanding, and grades have trended higher as well despite significant of high-grade reserves in the period. Plus, while this reserve base may look small at first glance, its total ounce count at Island sits at ~6.1 million ounces of gold with its 2022 P3+ Expansion Study (prior to further resource growth) estimating an 18-year mine life. Hence, when factoring in untested regional upside, land acquisitions (Manitou, Trillium) and recent resource growth, I would not be surprised to see Island Gold producing out to 2050.

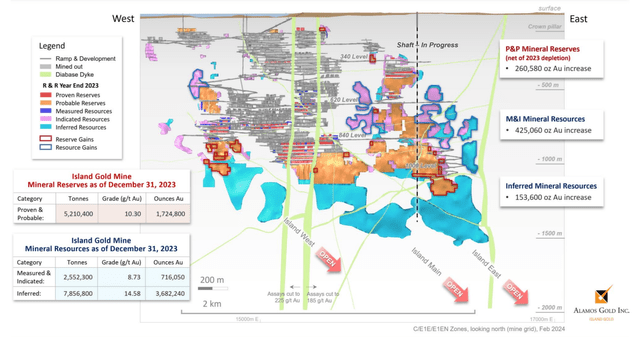

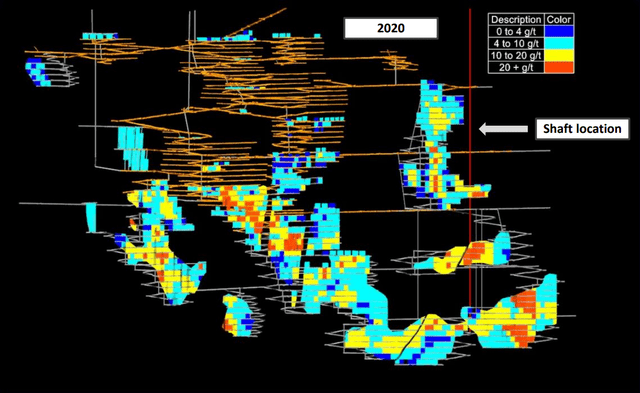

Alamos Gold Reserves & Resources Year-end 2023 – Company Website Island Gold Grade Distribution (2022) & Shaft Location – Company Website

Digging into the results a little closer, we saw a ~260,000 ounce increase in reserves net of depletion to ~1.73 million ounces at year-end with ~394,000 ounces of new reserves or ~261,000 ounces after ~134,000 ounces of mined depletion in 2023. Importantly, the bulk of new resource and reserve growth is located near existing infrastructure, which means it’s inexpensive to develop and access these ounces. Of course, accessing these ounces will get much cheaper with its new planned shaft underway right near where we’ve seen significant reserve growth, as well as pulling forward ultra high-grade ounces at Island Main/East.

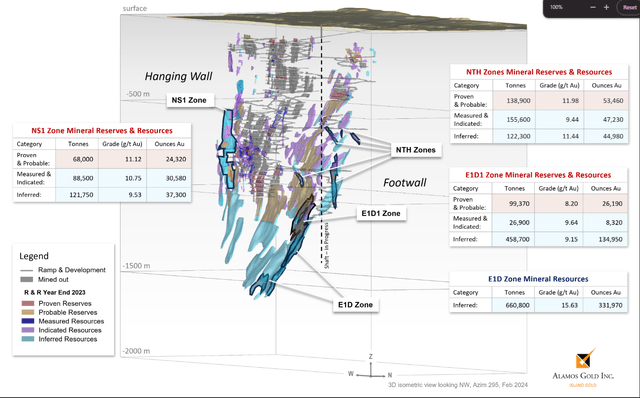

Island Gold Resource/Reserve Additions in New Zones – Company Presentation

Taking another look at the Island Gold Mine to focus on recent resource growth, we can see that Alamos has enjoyed considerable success adding ounces in hanging wall and footwall zones at Island. The most productive of these was the E1D Zone (footwall) where we’ve seen ~332,000 ounces added at 15.63 G/T of gold, ~7% above its current average inferred resource grade. Meanwhile, the NS1 Zone (hanging wall) added ~92,000 ounces of resources at ~10.3 G/T of gold, in line with Island’s current reserve grade. Finally, the NTH zones (footwall) saw nearly 150,000 ounces of total additions, including ~53,000 ounces at 11.98 G/T of gold.

While this has provided a significant boost to total resources ahead of increased depletion when Island Gold morphs into a ~300,000 ounce per annum asset post-2026, there looks to be considerable upside here. This is because the company has over 2,000 intersections above 3.0 G/T of gold outside of resources and reserves near-mine, including a massive hit of 2.9 meters at 1,389 G/T of gold in an unknown zone. Additionally, the company has consolidated its land package to ~60,000 hectares following a string of low-cost acquisitions. And while it’s still early days and Alamos has barely scratched the surface on regional potential, Pine-Breccia is looking quite promising with a multiple high-grade near-surface intercepts including 9.3 meters at 29.77 G/T of gold, 7.45 meters at 7.22 G/T of gold and 0.67 meters at 3,442 G/T of gold.

In summary, the ~$650 million acquisition of Island Gold is looking like the steal of the century with Island Gold only getting better at depth, the discovery of significant ounces near current infrastructure and what looks to be a 20+ year mine life at a near Tier-1 scale (400,000+ ounces) mining complex between Island Gold and Magino. And given the scarcity of 400,000+ ounce assets in safe jurisdictions with sub $900/oz AISC and industry-leading resource growth, Alamos deserves to trade a significant premium relative to its mid-tier peers.

Young-Davidson

Moving over to Young-Davidson, reserves fell year-over-year to ~3.26 million ounces of gold (~43.9 million tonnes at 2.31 G/T of gold) vs. ~3.34 million ounces at year-end 2022. This translated to a ~70,000 ounce decline in reserves on lower tonnes and grades, with just over 60% of reserves replaced for the year. However, it’s important to note that this reserve base still supports a 14+ year mine life based on an ~8,000 tonne per day throughput rate, and Young-Davidson had the same 14-year mine life as of year-end 2020 and has maintained a 13-year mine life since 2011, highlighting the strong track record of reserve replacement at this mine. Plus, while reserves sit at ~3.26 million ounces of gold, Young-Davidson has another ~1.27 million ounces backing up its reserve base, albeit at slightly lower cut-off grades (1.39 G/T of gold vs. 1.59 G/T of gold).

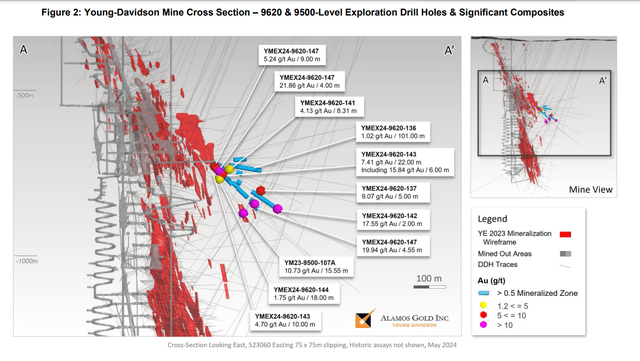

Young Davidson Mine Cross Section Looking East – Company Website

Although Young-Davidson may not be the lowest-cost mine, this is a consistent ~190,000 ounce per annum producer and Island has seen some exploration success more recently. This included high-grade intercepts of 22 meters at 7.41 G/T of gold, 4.55 meters at 19.94 G/T of gold, 4 meters at 21.86 G/T of gold and 9 meters at 5.24 G/T of gold drilled south of its existing resources and resources. Alamos noted that it is working to better define the extent, geometry and continuity of this high-grade hanging wall mineralization, but overall this is extremely encouraging for medium-term reserve growth given the proximity to existing infrastructure.

The other important takeaway from this recent news is that these grades are better than current reserve grades on average at Young-Davidson and this mineralization is outside of the syenite that’s responsible for most of the production at Young-Davidson to date and the bulk of MCM Mine production in 1934-1954 (Lovell, 1967 – Geology of Matachewan Area). Overall, this is very exciting as it represents a new form of high-grade mineralization that could allow for upside in its Young-Davidson’s production profile. And while Young-Davidson doesn’t get enough attention due to living in the shadow of Island Gold with its world-class grades/organic growth, this recent exploration success at Young-Davidson could see it start getting more attention vs. Island Gold stealing the spotlight.

Mulatos Complex

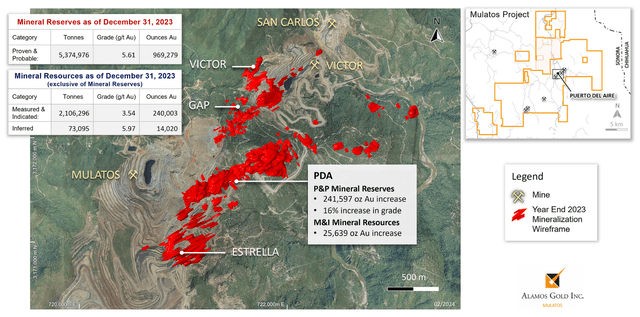

Moving to Mulatos in Mexico, year-end gold reserves came in at ~1.45 million ounces at 2.71 G/T of gold, a 14% decline in total ounces, partially offset by an increase in grades (year-end 2023: 1.95 G/T of gold). The higher grades were related due to the depletion of relatively lower-grade Mulatos Pit ore and material growth in the higher-grade PDA deposit, with year-end reserves of ~969,000 ounces at 5.61 G/T of gold. Meanwhile, although the company still has a decent amount of high-grade oxide ore at its new La Yaqui Grande Mine (~483,000 ounces at 1.33 G/T of gold), a solution will be needed to extend the Mulatos Complex mine life after what’s been a very productive 20 years since acquiring this asset.

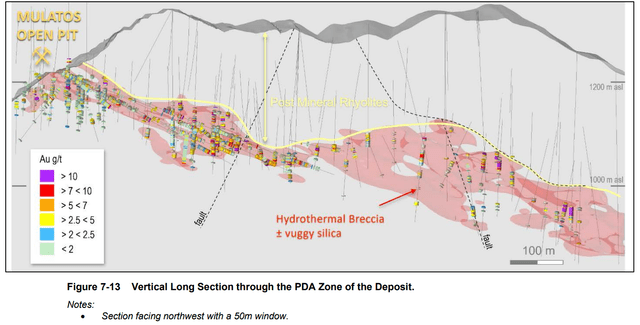

Fortunately, PDA looks to be the next opportunity to continue producing here after recently extending Mulatos’ life with La Yaqui Grande, with PDA having a high-grade reserve base of nearly 1.0 million ounces of gold. Importantly, PDA is attractive in that it can be accessed by ramp from the Mulatos Pit and while a sulphide processing facility will be required, costs could be reduced by using some components of its current milling infrastructure on site. Hence, while the short life at Mulatos is dragging down Alamos’ weighted average mine life today, I would expect this to be solved medium-term with a development plan due soon from PDA and ultimately a plan to develop this asset to extend Mulatos’ mine life well into the 2030s.

PDA Reserves – Company Website PDA Vertical Long Section & Mulatos Pit – 2023 Mulatos TR

The other key takeaway here at PDA is that Alamos has previously ignored sulphide discoveries (like a monster intercept of 50.3 meters at 14.47 G/T of gold released in Q3 2015 from Cerro Pelon) given that it was focused on higher-margin oxide ounces. However, with plans to be able to process sulphide ore as it transitions from La Yaqui Grande to PDA later this decade, Alamos has an opportunity to look at drilling out these high-grade sulphide targets which could extend the mine life further and allow for a hub & spoke type opportunity with its new sulphide mill.

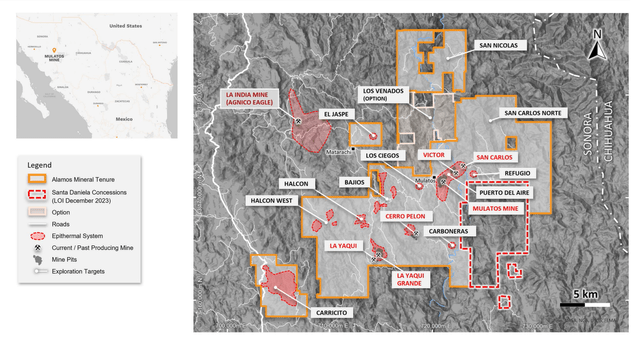

Exploration Targets & Mulatos Land Package – Company Presentation

To summarize, it’s a very exciting time at Mulatos from an exploration standpoint, as Alamos can start putting rigs back on higher-grade opportunities that were not prioritized historically. Plus, while Mulatos’ production profile is declining, PDA looks like a ~110,000 ounce per annum opportunity even without higher-grade satellite opportunities like Cerro Pelon based on a 2,000 tonne per day throughput rate, ~5.5 gram per tonne reserve grades and ~85% recoveries.

Mineral Resources

Finally, looking at mineral resources, Alamos finished the year with ~22.4 million ounces of total resources while maintaining its conservative gold price assumption of $1,600/oz for resources ($1,400/oz for reserves). This leaves Alamos trading at ~$300/oz on total gold resource ounces (~$530/oz on reserves post-Magino acquisition), a very reasonable valuation for a company pulling ounces out of the ground at sub $1,000/oz later this decade. However, it’s important to note that there are nearly 2.5 million ounces of resources excluding estimated reserves (~2.8 million ounces of gold) at Magino, pushing Alamos’ total resource base closer to 25.0 million ounces of gold at year-end 2024.

Alamos Gold Inferred Resources & Magino M&I (Reserves Inclusive) + Inferred Resources – Alamos & Argonaut Website

Summary

Alamos continues to execute near flawlessly and while it’s not cheap today, Agnico Eagle has rarely ever been cheap relative to its peers either. This premium has resulted Agnico rarely spending much time trading below 16x free forward cash flow, while the rest of its producer group often find themselves briefly spiking below 10x free cash flow in bouts of panic selling. And given that Alamos is arguably a mini Agnico Eagle with several superior attributes that includes an incredible track record of per share growth, I think it’s more difficult to justify selling out of one’s position in the stock when it becomes expensive, especially if we are entering a new bull market for miners.

This is because the highest quality (and in Alamos’ case, the highest growth) companies in any industry group will rarely provide attractive entry points in a bull market.

That being said, Alamos is an exceptional business at a fair price today and I prefer to buy exceptional businesses at a cheap price in commodity sectors due to the significant volatility and risks present in the mining sector. For this reason, I don’t see chasing the stock above US$20.50 as a wise move, with the better way to trade Alamos typically being to top up one’s position on any 15%+ pullbacks.

Overall, Alamos is simply unparalleled from a quality and growth standpoint today in the sector, it makes an excellent buy-the-dip candidate during the next sector-wide correction, and I would not be surprised to see the stock trade above a $10+ billion valuation longer-term.

Read the full article here

")

")

")