BigBear.ai (NYSE:BBAI) sees its stock soar on the back of a press release that is high on dreams, but it’s more turbulence than takeoff.

If we cut the chase, I make the case that BigBear.ai will use the fact that its share price is soaring to dilute shareholders, as the company holds about $70 million of cash and equivalents, significant debt, and is on a path towards burning $40 million of free cash flow in 2024.

Avoid this stock as this share pump will not hold its ground.

Rapid Recap

Back in April, I said,

I believe that in the next twelve months, BigBair.ai will be forced to raise funds by diluting investors.

Ultimately, I contend that over the next few quarters, investors will look back to BBAI at $1.76 as a high share price.

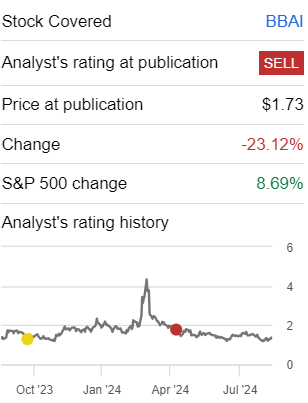

Author’s work on BBAI

Since I penned my previous analysis, the stock moved lower but has now rebound on the back of a press release, that has sparked a short squeeze that, I believe, is unjustified.

Critical Update to the Thesis

BigBear.ai gets awarded a shared contract. The press release is light on detail. But this is what we are told, ”Concept Solutions, LLC (CS). CS is one of fourteen companies awarded a Federal Aviation Administration (FAA)”.

From CS, which is one of 14 companies the awarded the contract, BigBear.AI is one of 12 subcontractors.

There’s no point in trying to overthink this. Very simple math means that per year, in the best-case scenario, the companies could make $240 million per year, for a grand total of $2.4 billion.

Of that $240 million, BigBear as one of 12 subcontractors, with CS being one of the 14 companies, implies that BigBear will probably make $1 to $4 million per year.

$240 million/14 companies = $17 million

$17 million/12 subcontractors = $1.40 million for BigBear.ai.

Note, that this is a pure estimate on my part, and I have nothing to substantiate my reasoning.

Here, I’ve simply assumed that BigBear gets an even portion relative to all the other subcontractors. More specifically, I divided the $240 million per year by the 14 companies to share the award, and then divided CS’s figure, by the 12 subcontractors.

Needless to say, CS isn’t working for free, of course. They too have their own overhead and since they have been awarded the contract and are responsible for the hiring, I wouldn’t be surprised to see them take 20% of the award as “simple running costs”.

But does thinking all this matter? No, it doesn’t. Because in the market there’s as much truth as there are willing believers. As it stands right now, the stock is up more than 30% after hours. This implies that this $1 to $4 million annualized revenue, has increased BigBear.ai’s market cap by more than $100 million. An impressive amount to capitalize on minimal revenue!

Given this context, let’s now discuss its fundamentals.

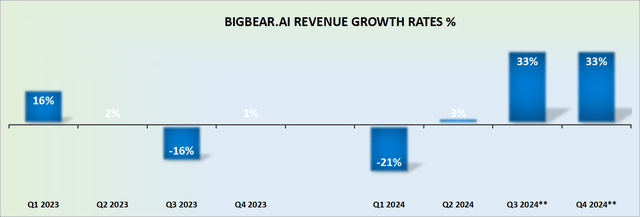

BBAI.ai’s Revenue Growth Rates

BBAI revenue growth rates

Here’s where the plot thickens. The second half of 2024 points towards BigBear.ai’s revenue growth rates accelerating. But let’s keep a few aspects in context.

Firstly, Q3 revenues are up in the plus 30% y/y increase since the prior year, its revenues were down 16% y/y. This means that even with minimal topline growth, its revenues would significantly increase since the comparables are so easy.

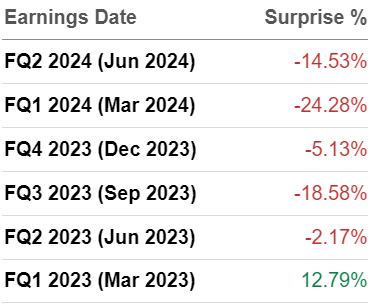

Secondly, consider the following graphic, where you see BigBear.ai’s revenue misses against analysts’ expectations.

SA Premium — revenue misses

This is not the sort of company that is at all conservative with its estimates to allow for a demonstrable beat later on. This is a company that does the opposite.

Given this context, let’s discuss its valuation.

BBAI Stock Valuation – Too Difficult to Quantify

BigBear.ai has approximately $120 million of net debt. For a company with a market cap of around $400 million (including the premarket jump), this is a lot of debt on its books for the size of its market cap.

Then you have to keep in mind that for the first 6 months of 2024, BigBear.ai burnt through $24 million of free cash flow. This means that, for all intents and purposes, BigBear.ai will probably burn through $40 million of free cash flow in 2024.

Put another way, I strongly believe that in the next 12 months, BigBear.ai will need to raise capital, as its $72 million of cash dries up. Indeed, realistically, if BigBear.ai’s management team isn’t acting now to dilute shareholders, and raise capital, as its stock is soaring, I would sum it up as a very poor capital allocation strategy.

The Bottom Line

In light of BigBear.ai’s soaring share price, it’s clear to me that the management must act swiftly to dilute shareholders and raise capital while they still can. With significant debt and a cash burn rate that’s rapidly depleting their reserves, delaying this move would be a missed opportunity.

If they don’t seize this moment, they’ll be missing the bear market before it hibernates.

")

")

")

")

")