")

")

Woori Financial Group (NYSE:WF), Korea’s fourth-largest banking group by asset size, is among the cheapest Korean stocks, trading at 0.4 P/B and 4.41 P/E despite being a perfectly healthy bank that is even looking to expand through M&A activity. Furthermore, the bank currently pays a 7.50% dividend yield while having a dividend payout ratio of less than 30%. If WF were located in most developed countries it would be much more expensive, but WF is a Korean bank and is subject to the dreaded Korean discount that has trapped a lot of value all over the Korean stock market. In my view, WF is cheap even by Korean standards and offers solid upside potential in the short term due to an uptick in lending volume recently observed in Korea, while the mid-to-long-term offers potential due to the government’s plan to unlock shareholder value through the Corporate Value-up Program.

WF was formed in 2001 through the forced merger of 4 banks that had failed Basel capital requirements as a consequence of the Asian Financial Crisis. The local deposit insurer KDIC poured nearly $9.5bn into the bank to keep it afloat. Woori achieved full privatization after it purchased the remaining stake held by KDIC worth 136.6bn won in March 2024. WF’s largest institutional shareholders are currently BlackRock with 6.07% stake and Korea’s National Pension Service with 6.03% stake as of end-June, according to Woori’s latest 6-K SEC filing.

Peer comparison

When compared to peers, Woori is still the cheapest large Korean bank as its NYSE-listed peers KB Financial Group (KB) and Shinhan Financial Group (SHG) trade at 7.93 and 6.76 P/E, respectively, compared to WF’s 4.41. In terms of the P/B ratio, SHG and KB are also more expensive at 0.57 and 0.63, respectively. WF shines in terms of the dividend yield as it offers a 7.5% yield compared to 4.24% for KB and 3.80% for SHG. When looking at the entire Korean market as a whole, WF is also dirt cheap, as the iShares MSCI South Korea ETF (EWY) trades at 12.71 P/E and 1.04 P/B. EWY is not a particularly good way to gain exposure to Woori as Woori has only 0.99% weight in EWY, making it the 24th largest stock in the ETF.

In my view, part of the reason for Woori’s cheapness stems from the fact that it was associated with the four failed banks in the Asian Financial Crisis, while simultaneously its CET1 ratio remains lower than its peers in Korea. For instance, Woori’s CET1 ratio stood at 12.0% as of end-June, compared with KB’s CET1 ratio at 13.6% and SFG’s CET1 ratio which stood at 13.1%. At the same time, WF’s profitability remains slightly below peers with a ROE (TTM) of 7.37% compared to 7.48% for KB and 7.99% for SHG. In terms of the net interest margin, WF is in the middle of the pack with a net interest margin of 1.74% compared to 2.08% for KB and 1.62% for SHG. In addition, its cost/income ratio is a little bit higher at 39.8% compared to 36.4% for KB and 37.33% for SHG.

WF compared to peers KB and SHG (Seeking Alpha, company reports)

Woori posts highest-ever quarterly profit in Q2, eyes M&A in insurance industry

My recommendation to invest into Woori comes after the bank reported its highest-ever quarterly profit of 931.4bn won in Q2, up by 44.1% y/y. The bank also reported other positive developments, such as an increase in the cumulative ROE ratio to 10.8% and a decline of the C/I ratio below 40% for the first time ever. Positively, non-interest income also rose robustly by 92.1% y/y to 535bn won, led by higher fee income. It should be noted that fee income will continue to be a strong contributor to profit as the bank will re-launch its securities business in August after acquiring digital brokerage firm Korea Foss securities earlier this year.

Going forward, Woori bets on further strengthening non-interest income as it signed a MOU to acquire two Korean life insurers, Tongyang Life Insurance and ABL Life Insurance. The acquisition of the two insurers would position Woori as the 6th largest insurer in Korea, as they hold combined assets of 49.91tn won. This might be a good time to buy insurer companies given that the Korean M&A market is currently saturated with insurance companies for sale. Woori previously mulled over the acquisition of Lotte Insurance, but it pulled out of the deal due to the hefty asking price for the non-life insurer. The bottom line is that the entry into the insurance business will probably be beneficial for WF as it will diversify earnings, especially in light of the expected decline in interest rates.

Korean banks set to benefit in short-term from resurgence in lending volume

Recently, lending volume in Korea has picked up led by recovery in mortgage lending which is mostly fuelled by the increase in real estate prices in the capital Seoul. This should bode well for interest income even in a period of falling interest rates as the central bank BOK is preparing to start cutting rates in Q4. Historically, two of the strongest years for interest income for Korean banks were 2021 and 2022 when the housing prices surged in Korea immediately following the pandemic.

Housing prices have briefly corrected in 2023, but have resumed their uptrend in 2024 and are now rising at the fastest pace since 2018 in the capital area, according to this Bloomberg report. This has caused some concerns among policymakers, but the government has mostly responded by presenting a package with housing supply measures rather than restricting housing demand. Increasing housing supply will underpin lending volumes even further and will be bullish for banks going forward. Meanwhile, the Korean economy remains in good shape and is projected to expand by 2.5%, according to the latest IMF forecast, which continues to drive corporate lending demand.

Looking at Woori’s credit data for the last quarter, total credit increased by 9.6% y/y mostly on the back of rising corporate loans which expanded by 13.8% y/y, whereas household loans rose by 4.1% y/y. That said, the bank achieved part of the lending expansion by lowering interest rates on interest-earning assets to 4.67% in Q2 from 4.73% in Q1 as competition between banks intensified.

Corporate Value-up programme remains key to unlock value in medium-to-long-term

For Korean stocks to exit their value trap, the government needs to proceed with the implementation of the Corporate Value-up programme which was announced in February. Overall, I am moderately optimistic that the Value-up plan will be successful in the mid-to-long-term mainly because of the growing popularity of stock investing in Korea, which will boost investor activism and put pressure on the government to protect minority shareholders. In addition, most Korean banks are not controlled by powerful founding families, which makes them more willing to implement value-enhancement plans. The Corporate Value-up programme relies entirely on voluntary participation, so it would be up to individual companies to implement it.

That said, the changes in the Korean stock market are going to be challenging and will take a considerable amount of time to implement as they run against the powerful chaebol interests. In addition, the Korean parliament currently remains dysfunctional, and it would be difficult to reach bipartisan consensus for tax reform. Needless to say, if the Corporate Value-up programme fails, it would put downward pressure on Korean stocks.

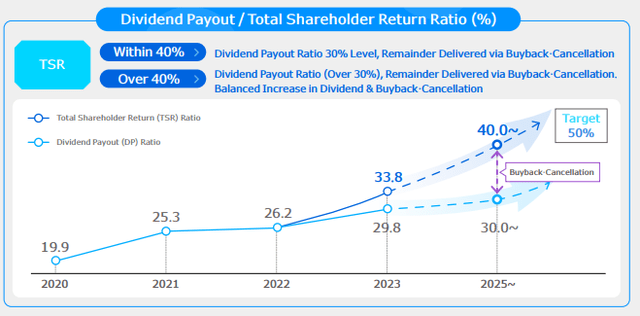

Woori’s shareholder return plans (Woori value enhancement plan)

WF released its own Corporate Value enhancement plan in July which is based on three key objectives to raise ROE to above 10% in the mid-to-long-term, improve the CET1 ratio to above 13% and return more than 50% of profits to shareholders. To note, WF’s current shareholder return remained quite low by global standards at around 33.8% in 2023 on the back of 29.8% dividend payout ratio and the rest coming from share buybacks. As the WF improves its profitability and shareholder payout, it is expected to benefit from the government’s plan to provide tax breaks to companies that raise shareholder value. That said, the details regarding the government’s tax breaks for value-enhancing companies are still scant, but judging from WF’s very low multiples it could be one of the primary recipients of tax cuts.

Conclusion

Woori Financial Group remains very attractive at these price levels, especially considering that there is nothing intrinsically worrying about the bank, and it remains cheaper than its Korean peers. In addition, Korean banks as a whole might get a tailwind from the government’s Corporate Value-up programme as they all trade well-below book value.

The current monetary policy conditions in Korea remain tight, but lending volumes have picked up recently, and real estate prices seem on the verge of entering another bull market. This should underpin interest income for banks even as central banks are preparing to ease policy and net interest margins decline. In addition, WF is seriously considering to enter the insurance market which will diversify its income and provide inorganic growth.

Downside risks for the stock stem from Korea’s large exposure to the semiconductor sector, which could drag down the entire market if the semiconductor sector enters a bearish market. As it was seen on August 5, the entire market could be sold off on concerns about semiconductor demand and economic slowdown abroad. On the other hand, the market has bounced back from the Aug 5 low and the moment might be right to look at some of the attractively valued Korean stocks.

Read the full article here

")

")

")