")

")

Thesis: Alibaba is no longer a compelling investment, even when setting aside political risk.

I last covered Alibaba Group Holding Limited (NYSE:BABA) (OTCPK:BABAF) in May, focusing on what I considered the “elephant in the room” for investing in the company: political risk.

In that article, I argued that while Alibaba was an eCommerce leader in China and a well-managed business, these strengths were overshadowed by the political risks inherent in investing in China.

However, after BABA’s latest earnings, I believe the situation has worsened. I see Alibaba now exhibiting structural revenue growth and profitability issues, on top of the persistent political risk. Although BABA’s valuation remains inexpensive, these underlying problems make the company a fundamentally unattractive investment in my view, even if one were to “ignore” political risk.

I still view Chinese equities as an asymmetric bet on the Chinese Communist Party (CCP) potentially pivoting its current economic policies. That said, I continue to avoid Chinese equities as this is not a risk I’m willing to take.

However, if I were interested in betting on Chinese equities, I would now favor other companies over Alibaba. For instance, I would consider investing in PDD Holdings Inc. (PDD), a leading Chinese eCommerce player that has captured significant market share from Alibaba in recent years and currently trades at a lower P/E ratio. Alternatively, I would opt for a diversified Chinese equity fund, such as the iShares China Large-Cap ETF (FXI).

Because of the stagnation of Alibaba’s business compared to Chinese and American peers, I reiterate BABA as a SELL at current price levels.

After anemic quarterly earnings, I do not see Alibaba as a Tech company anymore

Alibaba’s reported troubled earnings for the three months ending with June 2024, which the company considers Q1 results for their fiscal year. Earnings were a miss against analysts’ expectations on both Revenue and EPS, by -1.70% and -86% respectively.

As a long-term investor, I am usually not worried about a single quarter. Rather, I look at quarter-on-quarter and year-on-year data to assess the direction of a company. This case is not an exception – what I find interesting about BABA is not the quarterly miss per se, but rather the picture that is emerging with these new earnings.

Alibaba is growing revenue at 4% Year-on-Year, driven by its International Digital Commerce Group with a 32% growth. Taobao and Tmall, the local eCommerce markets for China, are experiencing a 1% decline in revenue, while even the company’s Cloud segment is showing a growth of 6%, which I do not find impressive when compared to peers (which I will cover next).

In terms of Net Income, the picture is worse, with a decline of 27% in Q1 against the same quarter of last year. Management talks about this figure in page 1 of their earnings deck, attributing the decline to:

[…] a decrease in income from operations and the increase in impairment of our investments.

This statement shows, in my view, how the decline is not due to a one-off item, but rather it signals a recurring, troubling issue with the company.

To put these numbers in context, I will compare them to the latest year-on-year figures reported by Walmart Inc. (WMT), Amazon.com, Inc. (AMZN), as well as two Chinese competitors of BABA; PDD Holdings and JD.com, Inc. (JD). All data is taken from Seeking Alpha for the last quarter available:

-

Walmart is growing revenue at 5% and Operating Income by 7.4%.

-

Amazon is growing revenue at 10% and Operating Income by 90%.

-

PDD Holdings is growing revenue by 119% and Operating Income by 293%.

-

JD.com is growing revenue by 13% and Operating Income by 67%.

What’s concerning, in my view, is that Alibaba, a company positioned as a tech giant, is consistently reporting financial figures that resemble those of an established, mature company rather than a high-growth tech firm.

While BABA’s valuation remains cheap, I see its fundamental appeal as limited. Even compared to established players like Walmart or its Chinese peers, the company is struggling with a significant decline in profitability, which I consider a red flag for investors.

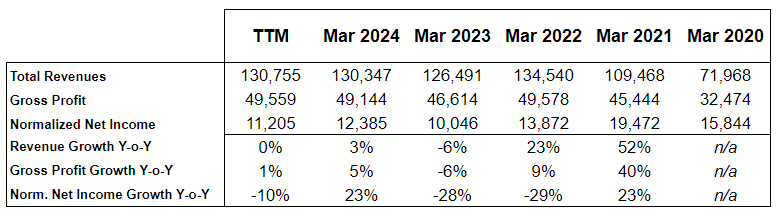

Alibaba Annualized Key Financials, 2020 to TTM (Author’s elaboration of Seeking Alpha data)

Zooming beyond single quarter results, I see a business that is now stabilizing on anemic growth both for top and bottom lines on an annualized basis. The chart above shows how BABA’s business has evolved since 2020 in terms of key financial figures. It is clear to me that following the Chinese government’s fines and crackdown on Alibaba in 2022, the company has failed to show it can turn around its business.

To conclude, I believe Alibaba is demonstrating a structurally weakening business, now facing sluggish growth in the critical Chinese domestic market. The long-awaited turnaround that I think many investors were hoping for seems increasingly unlikely to materialize at this stage, in my opinion.

A new kid on the block is stealing BABA’s lunch

During the last few years, a new player emerged as a leading Chinese eCommerce. I am talking about PDD Holdings, previously known as Pinduoduo. PDD was founded in 2015, and it rapidly became one of the most successful eCommerce platforms in China, growing at rates higher than what Alibaba experienced in its early years.

The secret sauce of PDD is having merged social media with eCommerce, and “gamified” the entire online purchasing experience for Chinese consumers.

Similarly to Alibaba, PDD has also expanded abroad, with success. Temu was launched in 2022, and it rapidly became a hit in the USA, with its App being among the most downloaded in 2024.

Partially because of PDD’s stellar rise, Alibaba has experienced a decline in their market share of eCommerce in China, by more than 10% from 2021 to 2023.

What I find interesting about the rise of PDD, in the context of the demise of Alibaba, is that his founder, Colin Huang, seems to be liked by the CCP. Mr. Huang is today the richest man in China. What the CCP seems to like about him is the fact that he is reserved, well-spoken and adherent to party lines.

That is in stark contrast with Alibaba’s legendary founder Jack Ma, who has almost completely disappeared from the public since having been vocal in his criticism of the CCP in 2020.

I am not suggesting that Alibaba’s business issues stem exclusively from politics. However, I do believe that having a strong, innovative competitor with a CEO that is well liked by the CCP is a strong headwind for Alibaba. A headwind that, data is starting to show, BABA’s management has not been able to address, falling behind peers.

BABA and PDD: quick comparison and reason why I would pick the latter

Personally, I do not invest in Chinese equities because I find the overall political risk not worth the potential upside. However, until the last earnings, I still believed that an investment in BABA would be beneficial for investors willing to bet on the CCP pivoting its economic policies.

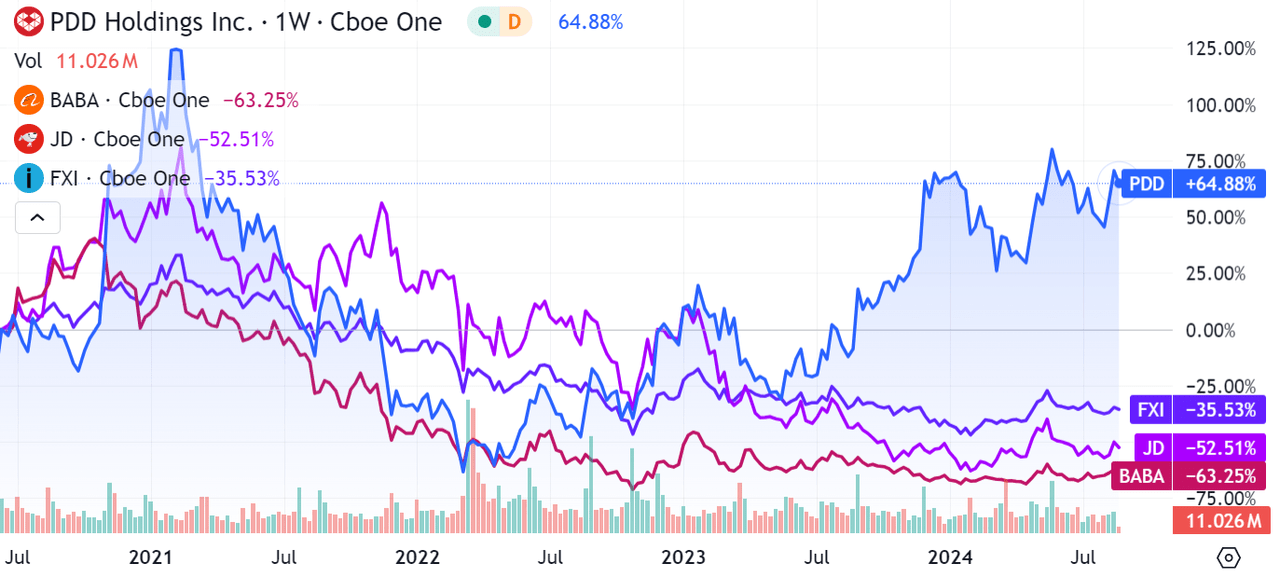

PDD, BABA, JD, FXI Comparison Dec 2020 to date (Seeking Alpha)

Since BABA was disproportionately targeted by the CCP (and its stock suffered accordingly), I assumed the company would disproportionately benefit from a pivot in party lines, or even from a slight increase in China’s openness to the West.

This is no longer the case. I find an investment in PDD way more compelling than one in BABA given the current situation. Both companies are cheap, but PDD is a leading and growing eCommerce platform, while BABA seems a stagnating giant.

While I won’t provide a target price for PDD—this is beyond the scope of my article—I do want to highlight the following key metrics in terms of comparison:

-

PDD has a FWD P/E of 7.6, against BABA’s 9.52

-

PDD has a current dividend yield of 2.21%, only slightly less than BABA’s 2.33%

In summary, buying PDD offers investors a well-valued, leading Chinese eCommerce company. In my opinion, this makes it a far superior choice compared to investing in Alibaba.

Risks to my thesis

The main risk to my thesis is that Alibaba’s management could successfully execute a business turnaround, finding a way to restore growth and profitability in its Chinese eCommerce segment. If that were to happen, Alibaba’s depressed stock could experience a significant bounce back.

Another risk is that the CCP might shift its stance on private companies being required to prioritize “common prosperity”. If such a pivot were to occur, I have no doubt that all Chinese equities would see significant gains, returning to valuations more in line with international peers.

Although I no longer believe Alibaba would disproportionately benefit from such a change, it’s still a risk worth noting.

Conclusion

Even though I am bearish on Alibaba and, more broadly, on Chinese equities, I want to emphasize that my stance is not against China, the CCP, or the Chinese people. I feel it’s important to clarify this in my conclusions, as sometimes negative opinions on Chinese equities can be mistakenly seen as criticisms of the country itself.

From an investment perspective, it doesn’t matter whether Alibaba’s struggles are partly due to political factors or solely down to management. The reality is that the company has become a stagnating business with significant profitability issues that need urgent attention. This, in my opinion, makes it fundamentally unappealing for shareholders. That’s why I reiterate my SELL rating for the stock.

If I were inclined to invest in Chinese equities, particularly in the eCommerce space, I would prefer PDD. For investors seeking broader exposure to the Chinese market, a diversified large-cap fund like the FXI ETF would be a more attractive option.

Read the full article here

")

")

")