")

Introduction

Hims & Hers Health (NYSE:HIMS) has had an outstanding year so far, as the stock price is up 87.73% YTD. Q4’23 earnings gave investors a lot of confidence going forward, as the company exceeded expectations and raised its guidance. Q1’24 earnings also received a great reception, with the company posting great results once again. Weeks later, the company announced it would start selling compounded GLP-1 agonists to subscribers. Investors and the market responded well, as the stock price soared in the weeks following the announcement. However, controversy and short reports emerged in the following weeks, leading to a sell-off as news circulated that the company might not be able to continue selling GLP-1s.

Since my last article, Hims has dropped a considerable amount—almost 30%, to be exact. The flurry of negative news has sent the stock down to prices not seen since late May. Not much has changed fundamentally, but overall sentiment for the ticker appears far less bullish today than it did a few weeks ago. So what’s next? Let me dive into the recent earnings report and explain my thought process.

Earnings Update

Per the Q2’24 filing, the company posted updates regarding the future of their business, along with fantastic topline growth.

For Q2’24, Hims posted the following numbers:

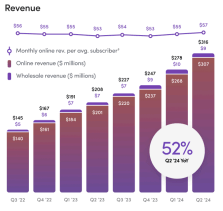

- Revenues of $315.60 million, 52% YoY growth

- Net income of $13.30 million, turning positive as this quarter last year they posted a $7.20 million dollar loss

- Free cash flow of $47.6 million! A 270% increase YoY

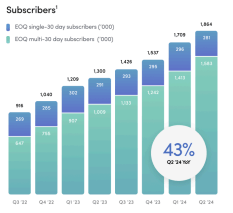

- 1.864 million subscribers, a 584 million (43%) increase YoY

- 9% subscriber growth QoQ (Q1’24 1.709 million subs)

- ARPC increased 8% YoY, from $53 per customer last year to $58 this year

Nothing but great numbers across the board.

Subscriber and ARPC Growth

Hims & Hers Subscriber Growth (Hims Q2’24 Shareholder Letter)

As noted in the previous section, Hims and Hers now has 1.864 million subscribers, up from 1.30 million this time last year. Impressive enough, subscriber growth has actually reaccelerated, as subscriber growth appears to have bottomed last quarter. Over the past 3 months, the company has seen total subscriber growth come from its core business and the new GLP-1’s. It’s worth remembering that the GLP-1 offering launched on May 20, meaning that there was less than half a quarter to record these numbers.

Hims & Hers Q2’24 Shareholder Letter ARPU (Hims & Hers)

While subscriber count has continued to grow at a rapid pace, monthly average revenue per customer (ARPU) has also increased QoQ. The importance of this cannot be understated. It would be very easy to see ARPU flat given the large increase in subscribers, but this is not the case. The company is likely benefiting from economies of scale paired with subscribers opting for personalized solutions.

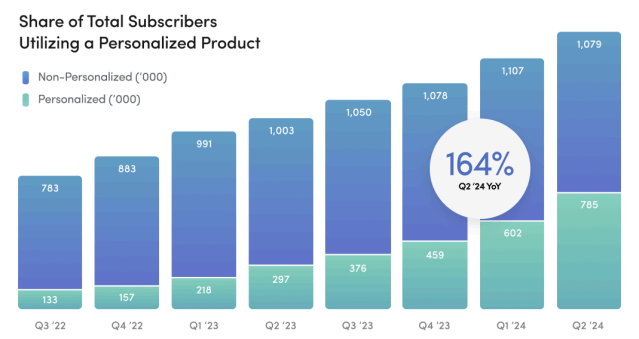

Demand for Personalized Products Remains

One of the main focal points for the company has been the idea of giving customers the ability to take advantage of personalized products. For years, Andrew and the team have emphasized the importance of personalized solutions, whether it be dosage, form factor, or compounding. The company’s website asks all types of questions, helping the customer get the solution that best fits their wants and needs.

Our focus on providing access to high quality personalized solutions at an affordable price continues to resonate with consumers.

-Andrew Dudum

On the Q2’24 call, Andrew mentioned four of their five specialty products now have ten or more personalized solutions. Customers now have a plethora of form factors for the medication they take, making them more likely to choose Hims and Hers.

According to a study conducted by an academic institution in Brisbane, 32% of subjects reported difficulty swallowing pills, tablets, or capsules whole. Hims gives options, and people want a choice.

On the Q1’24 earnings call, Andrew also noted that many individuals are less likely to continue medication given they don’t like the form factor. For example, the Hims product line for hair growth includes pills and sprays. It’s been reported that many customers dislike the spray, as it made their hair sticky or uncomfortable, resulting in a canceled subscription.

What’s great is that over 40% of subscribers to the company have used some version of personalized solutions. This number has increased by almost 30 points over the past two years, suggesting high demand for the customization of medication. For example, this quarter, approximately 85% of new dermatology subscribers use personalized medication.

Hims & Hers Q2’24 Shareholder Letter (Hims & Hers)

Each customer has unique needs, and the company stands out among others as the de facto option for this. Customer acquisition has benefited from this, and I expect this trend to continue, as more people want medication tailored for them.

SBC, Buybacks, and Marketing Spend

I’ll start this section with what I see as the downside. Like many companies, Hims has been granting a significant amount of stock-based compensation to employees. While this can incentivize good performance, it also dilutes shareholders, reducing their stake as the total share count increases. Hims has continued to issue stock as compensation, further diluting investors.

Hims & Hers Q2’24 Operating Activities (Hims & Hers Q2 Release)

The company also announced a new $100 million buyback program, to be completed over the next three years. This comes after the conclusion of the $50 million program announced in November of last year. The old program finished in Q2’24, purchasing back 1.9 million shares at an average price of $12.39.

The company hopes to “partially offset the effects” of the dilution caused by SBC, as well as purchase shares when the company feels that the current share price does not reflect the intrinsic value of the company. This new repurchase program is good to hear, as those within the company may see a disconnect between current share prices and fair value prices.

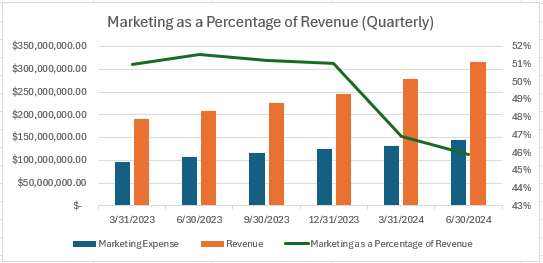

It also appears that one of the reasons the stock sold off post-earnings was the continuation of marketing-related expenses. The company has exponentially increased its marketing spend, with ads being played during the Super Bowl, NBA games, and on Hulu. Hims is still in hypergrowth mode and the company feels that ad spending will need to continue in order to acquire new customers.

Hims & Hers Q2’24 Marketing Expense (Hims & Hers Q2 Release)

Though, we can see that marketing as a percentage of revenue has dropped steeply over the past two quarters. This does not justify the massive marketing expense, but helps paint a picture of how much is actually getting spent.

Marketing as a Percentage of Revenue (Author’s Analysis, Seeking Alpha)

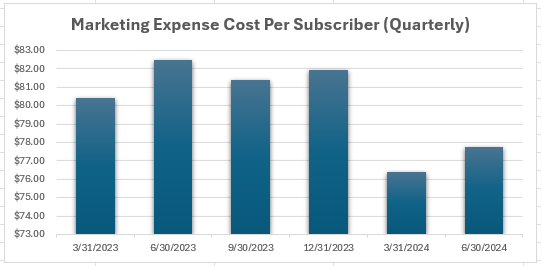

Even marketing costs per subscriber have dropped over the past few quarters, though there has been a slight uptick this quarter. Do mind this chart is quarterly, with marketing expense per subscriber floating around $25-$27 per month.

Marketing Cost Per Subscriber (Author’s Analysis, Seeking Alpha)

As the company starts to slow down and have better brand recognition in the coming quarters, it would be a good sight to see Andrew and the team slow the marketing expenses in hopes that customer acquisition becomes easier without the massive marketing expenses.

The Future of GLP-1s is Still Murky

The GLP-1 topic has been a hot topic of debate, with some individuals suggesting the shortage period is about to end and others saying it won’t end for a while. Whatever the judgment may be, it will absolutely have an effect on the company.

Many (including me) have said that the GLP-1 offering should not have an effect on the overall Hims thesis and that its core business is what matters most. While true, it is important to note that any negative news or sentiment regarding GLP-1s will now affect the company regardless of its importance to the main thesis. Let’s take a look at each side of the argument.

Andrew and the team see a future where compounded GLP-1s will be readily available through Hims and Hers. The company believes that there is a large shortage, leaving many without the ability to obtain said medication. They also believe that through personalized solutions, the company will be able to navigate its way through potential barriers along the way.

And then on the injectable side, I think there’s going to be, without question, a long horizon of on and off availability, just given the demand. We see thousands of patients coming every single day saying that they can’t get access to these medications. And so we suspect that we’ll be able to offer commercially available doses to in some form for extended periods. I think on top of that, as you said, as supply grows, we are excited to bring the branded medications for patients that are interested on to the platform as well as the personalized dosages. The compounding [Technical Difficulty] titration and dose customization exists and operates regardless of shortage. This is an exemption for which we operate the entire business under and have for the last six or seven years.

– Andrew Dudum

On the flip side, executives from Eli Lilly (NYSE:LLY) and Novo Nordisk (NYSE:NVO) have come out to say that the shortage has ended or is coming close to an end. Keep in mind that both companies have spent tons of capital in attempts to ramp up production for their respective weight-loss drugs.

Expectations are that Lilly’s drug ‘tirzepatide’ is coming off shortage soon or is already off, according to CEO David Ricks.

Lilly’s drug, tirzepatide, sold as Mounjaro for diabetes and Zepbound for weight management, will cease to be in shortage “very soon,” CEO David Ricks said in an interview with Bloomberg in Paris.

– Reuters

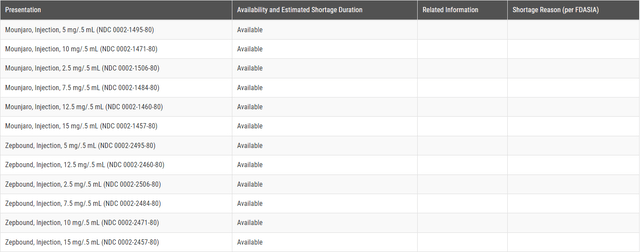

Mounjaro and Zepbound Availability (FDA)

According to the FDA website, we can see that all versions of Zepbound and Mounjaro are readily available and are currently not in shortage.

With the initial launch of GLP-1s came much excitement, as the stock price rocketed to all-time highs. So whether you want to believe it or not, GLP-1s are important to the business model, as many investors are looking closely at the potential business they bring. Hims has made its bed; now it’s time to lay down.

Updated Valuation

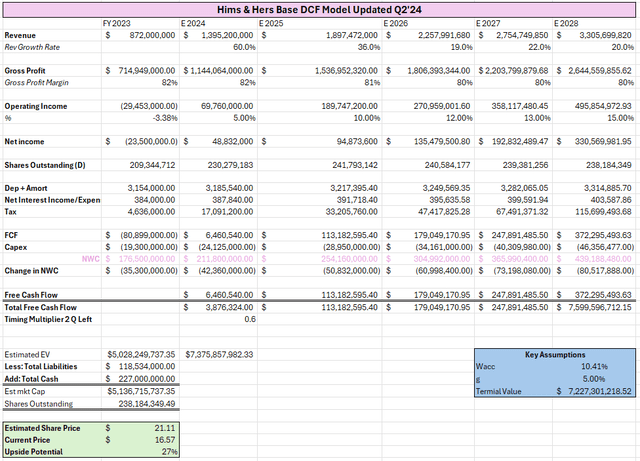

Based on my updated DCF model, Hims currently trades at a discount. The following assumptions were made to reach my final price target for the company:

- Revenue growth rates of 60%, 36%, 19%, 17%, and 25% for the years 2024, 2025, 2026, 2027, and 2028, respectively

- Shares outstanding of 238,184,449 for 2028

- Capital expenditures for this year of $24.125 million, growing roughly 18% annually

- Total liabilities of $118 million and cash of $227 million

- WACC of 10% and terminal growth of 5%

Hims DCF Model (Author’s Analysis, Seeking Alpha)

In this case, we end up with a fair value of $21.11 per share, a 27% upside from current prices. My price target has been slashed from my last article, as the potential risks have been better assessed along with a better margin of safety using more conservative numbers.

The fair value I’ve given is heavily influenced by the WACC input, so below I’ve shown where I got my WACC.

Hims & Hers WACC Analysis (Author’s Analysis, Seeking Alpha)

Conclusion

As Q2’24 wraps up, it’s clear that the company remains on the right track. If Hims can continue delivering personalized compounded GLP-1 agonists, the future looks promising. Looking ahead, I’ll be keeping a close eye on three key factors: marketing expenses, stock-based compensation, and subscriber growth/margins. If these areas show positive trends, I believe Hims could be poised for significant share price increases.

I give Hims and Hers Health, Inc. a ‘buy’ rating with a price target of $21.11.

Read the full article here

")

")