")

Q1 2025 Earnings Call Transcript")

")

Investment thesis

NN Group N.V. (OTCPK:NNGPF) has been an excellent performer in my personal portfolio, and it is one of the few with a relatively high yield. It is often the case that stocks with a high dividend yield are showing slow dividend growth. Luckily, NN is an exception.

Share price appreciation is the icing on the cake, but my investment thesis is mainly built around the total shareholder yield. At NN, this mainly concerns dividend yield and share buybacks.

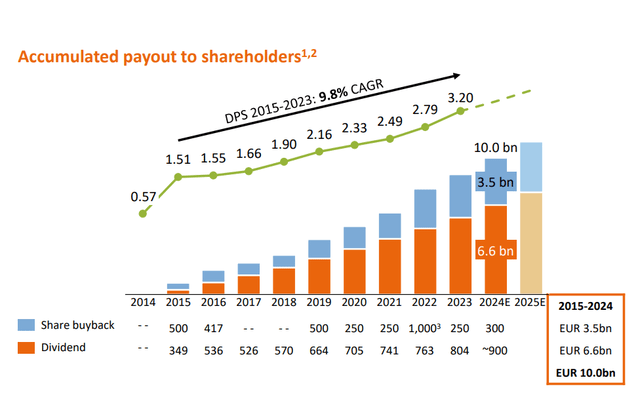

NN Shareholder distributions (Company profile August 2024)

In recent years the total shareholder yield has regularly exceeded 10%, which is a very solid return on its own. I also think that if the company continues to perform, it is certainly possible to exceed this 10% if we add up future share price appreciation.

On the 15th of August, NN has published its first half-year results of FY 2024. Amazingly, NN has increased its interim dividend by 14% compared to last year, which made my dividend heart beat faster.

However, it remains important that the company continues to perform well enough to continue to increase the dividend sustainably. I think the company is capable of doing this, just not at this growth rate.

Today we will update the investment thesis based on the latest financial results.

If you want to know more about my investment thesis, it is possible to read one of my previous articles about NN.

1H2024 results

It was expected that the growth would not be spectacular. The diversified business mix enables NN to achieve solid results.

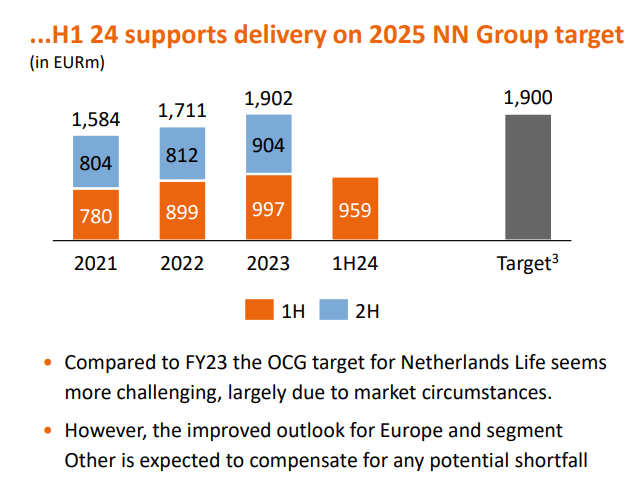

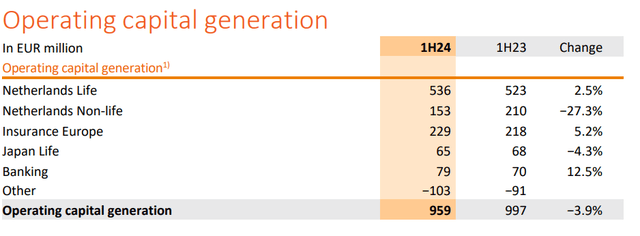

An important metric of NN is the operating capital generation, also called OCG, which was slightly lower than last year (€959 million vs €997 million). Yet, they appear to be well on their way to achieving their FY 2025 OCG target of €1.9 billion. They already achieved this in FY 2023, so enormous growth was not expected.

NN financial target FY 2025 (1H2024 investor presentation)

The reduction in OCG was mainly due to lower capital generation from the Netherlands Non-Life segment. Last year was a very good year with some windfalls when it comes to claims. Now there were some large fire claims at the start of 2024, but this segment still performs decent with a 92.2% combined ratio. This means profitability is still excellent.

OCG overview (1H 2024 press release)

The life segment of NN in the Netherlands is certainly not the fastest growing part of the company, but it is a very stable component of the business mix and is gaining some momentum again (+2.5%). The positive results were driven by higher mortgage spreads.

Netherlands Life (1H2024 investor presentation)

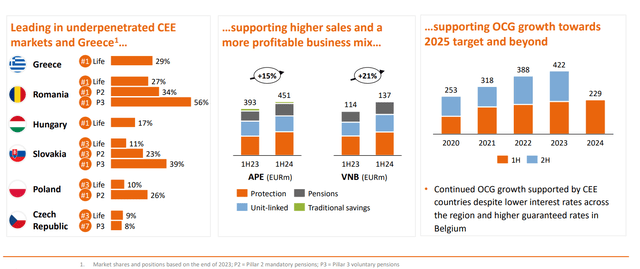

In previous articles, I have identified Insurance Europe as a potential growth engine of the company. NN continues to deliver here, and is able to show good growth in Central and Eastern Europe.

Insurance Europe segment (1H2024 investor presentation)

The growth in Europe was mainly driven by strong performance of the pension businesses as well as an increased contribution from new business activities.

We can conclude that non-life has a significant impact on the results. Last year’s windfalls make this year’s results look worse than they actually are. The outlook also remains unchanged, and they appear to be able to achieve their long-term goals for FY 2025.

Financial health

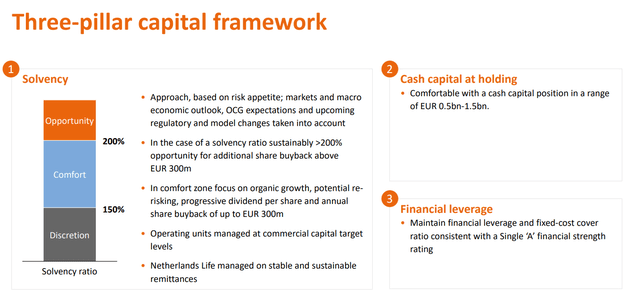

The solvency ratio is an important metric to evaluate. It is not only an important metric when it comes to the financial health of an insurer, but it is also important that it remains at comfortable levels to keep the investment thesis intact.

Why? If the solvency ratio is in the “comfort zone”, there is room to implement a progressive dividend policy and share buybacks above €300 million. When the solvency ratio is above 200%, there is even more room for additional share buybacks.

NN capital framework (Company profile August 2024)

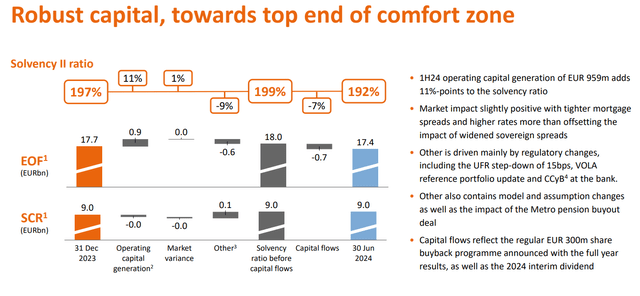

The solvency ratio decreased from 197% to 192% in 1H2024. This was actually better than expected, given the fact that the analyst consensus was 189%. The decrease was due to the deduction of the 2024 interim dividend and share buybacks. There were also some regulatory changes and reduction of the ultimate forward rate from 3.45% to 3.30% and an update of the Volatility Adjustment, which also has a negative impact on the solvency ratio. However, the impact seems manageable.

Solvency development (1H2024 investor presentation)

Credit rating agencies are also positive about NN’s financial stability, given the stable financial strength and credit rating scores.

NN Credit rating (1H2024 investor presentation)

In short, the financial picture looks good, which means NN will continue to be able to offer stellar shareholder distributions.

Shareholder returns

NN richly rewards its shareholders in the form of high dividends and share repurchases.

Paying out dividends seems to be the most important thing for NN. The company also gives the option to choose stock dividend instead of cash dividend. This is also one of the reasons why they buy back their own shares:

In accordance with its dividend policy, NN Group intends to neutralise the dilutive effect of stock dividends through the repurchase of ordinary shares. NN Group intends to cancel any repurchased NN Group shares under the programme unless used to cover obligations under share-based remuneration arrangements or to deliver stock dividend.

Source: NN investor relations

The dividend yield is currently 7.7%, which is a good starting point for the income-oriented investor.

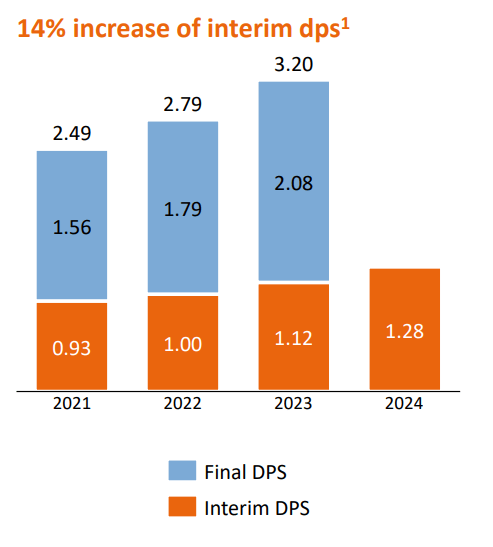

NN has also announced that it will increase the interim dividend by 14% compared to 1H2023.

NN dividend per share development (1H2024 investor presentation)

This is again an acceleration in growth compared to previous years. However, I think that this growth rate is not feasible in the future. Given the company’s growth prospects, I expect mid-single digit growth in the years to come.

The dividend can also be called safe. If we divide the interim dividend per share (€1.28) by the 1H2024 EPS (€2.21), we get a payout ratio of 57.9%, which means the margin of safety is still there. I know that the interim dividend is about 40% of the annual amount, but I expect that the EPS in the second half of the year will be sufficient to maintain a safe payout ratio.

In addition, the company would like to buy back at least €300 million of its own shares per year. Given the market cap of €12.4 billion, this comes down to 2.4% of the total shares outstanding. With the current share price, we arrive at a total shareholder yield of 10.1%, which is attractive in my view.

Unexpected news

During this quarter, there was some striking news about NN. On the 20th of June, press reports emerged that NN wants to focus more on banking. In this way, they want to compete with large Dutch banks such as ABN AMRO Bank N.V. (OTCPK:AAVMY), Rabobank and ING Groep N.V. (ING). The market is dominated by these 3, but NN is certainly not without a chance with a total of 7 million customers.

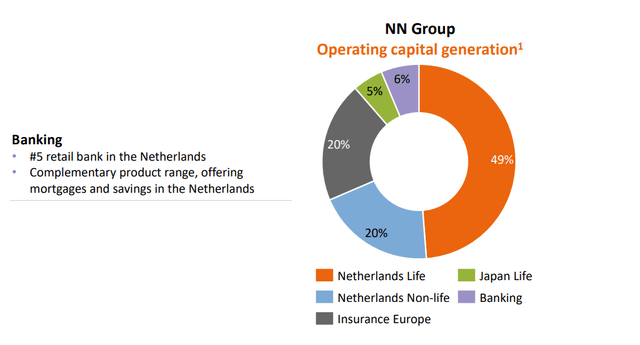

NN is not entirely new to this segment, as they now get 6% of their OCG from banking.

NN OCG overview (NN company profile august 2024)

The new banking actions mainly involve offering current accounts with an associated bank card and an app. The necessary costs will be charged for this service. This concept in itself is not very profitable, but NN sees it more as a part of a bigger picture.

A few days ago, David Knibbe, the CEO of NN, was a guest at a Dutch radio show, where he told something about the plans. He called the case “not very big”. However, the action plans should lead to more intensive relationships with customers, increasing the chances that they will also purchase other products, such as insurance.

NN is currently still in the middle of the pilot phase and will probably take shape next year. I therefore expect more clarity during the next capital markets day, which will take place in May 2025. I do hope that NN does not follow the path of diworsification and stays close to its core business. I can understand that management wants to increase NN’s visibility in this way and utilize the possible effect of cross-selling. However, I believe that the focus should remain on insurance and that the return on investment when it comes to banking activities should be closely evaluated.

Valuation

At the moment NN has a price-to-book of 0.60, which is still significantly lower compared to its sector median of 1.21. This could be an indication of undervaluation. Maybe this is partly due to its ROE of 5.6%, this is low compared to its sector median of 10.26%.

Given the new input, I think it would be a good idea to do a fair value calculation again using the dividend discount model. The model fits the company quite well because of the consistency in dividend payments and NN’s dividend growth policy.

For the “next year’s dividend” I use the interim dividend of €1.28 and the final dividend of FY 2024, which will likely be paid in June 2025. In my previous article I used a dividend of €3.40, but given the significant increase in the interim dividend it will most likely be higher. For now, I will use a “next year’s dividend” of €3.50. I think this is on the conservative side, but this is more aligned with my view of NN going forward, as I think that the current dividend growth rate is not sustainable.

The dividend growth CAGR from 2015 to 2023 is 9.8% and with the 14% growth of the last interim dividend, the CAGR will probably be even higher next year. From a business growth point of view, I think the long-term dividend growth will be more in line with their free cash flow growth assumptions of mid-single digits (2023 annual report). I tend towards a dividend growth of 5-6%.

Last but not least, I used a rate of return of 12.5% because this is my personal rate of return on my investment for NN.

I calculated a fair value of €46.66 with a dividend growth rate of 5% and €53.84 if we assume an annual 6% dividend growth.

Compared to the current share price of €43.55, NN looks 7-23% undervalued.

Conclusion

Based on the most recent data, my investment thesis hasn’t changed. NN has delivered solid business performance and manages to increase the dividend time and time again. Add the dividend yield to the share buybacks, and you have an annual shareholder yield of +10%.

In my view, NN’s business mix is also getting better. Even though the non-life segment performed somewhat less than expected, profitability is still high. The fact that they have a good position in life and non-life, both in the Netherlands and in Europe, makes NN a good choice from a diversification point of view.

As you can see above in my calculations, the dividend discount model responds very sensitively to small changes in the dividend growth rate. However, both outcomes are still above the current share price.

Of course, there are also investment risks associated with NN. Further economic headwinds can have a significant impact on financials in general and therefore also on insurers. If interest rates fall during such a scenario and fixed-income securities are going to yield less. It can also have a significant impact on the total value of the investment portfolio, which in turn affects the solvency ratio. In the worst case, a low solvency ratio leads to a discontinuation of their share buybacks and a potential dividend cut. NN’s banking plans will also be closely monitored. This could be a great opportunity to increase their visibility, but this should not distract too much from their core activities.

All in all, I give NN a “BUY” rating.

I will closely monitor developments regarding NN and update my thesis again with the next financial update.

Happy investing everyone!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

Q1 2025 Earnings Call Transcript")

")