")

Q1 2025 Earnings Call Transcript")

")

Dear readers/followers,

It’s time for another update on steel company ArcelorMittal (NYSE:MT). This is a business I’ve been covering for a number of years at this point, and have been investing in for some time as well. While I’ve already established a position, I believe the time has come for me to expand on that position even further.

The reason?

Valuation – the company has now dropped to levels where I would definitely consider the company not only cheap, but very cheap, and definitely with enough of an upside to really justify a good position here.

And in this article, I’ll show you exactly why that is.

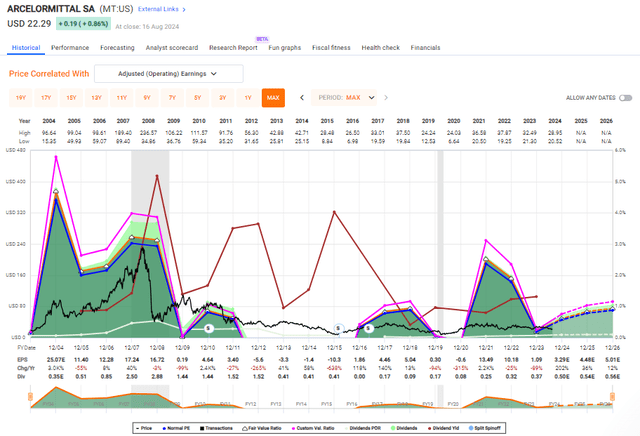

Companies in this sector are definitely some of the less stable ones out there – and ArcelorMittal is definitely a good company to exemplify this fundamental instability. Take a look at the company’s earnings trends for the past 20 or so years.

ArcelorMittal F.A.S.T graphs (ArcelorMittal F.A.S.T graphs )

Stability? Try again. While my strategy centers around stability as well, it above all trends around upside and valuation. And that is what I believe that I see here. Both good upside and valuation for this company – coupled with quite excellent overall fundamentals.

You can find my last article on ArcelorMittal here. The company’s recent drop does not really bother me. The reason is, that we’re only seeing a better and better valuation.

Remember, this company’s dividend or dividend yield isn’t the reason for investing. It’s below 2% even now after the drop. You can find my article here, by the way, if you’re curious about the past performance of this particular stock.

But let’s now look at the near-term upside.

ArcelorMittal – Looking at the latest quarter and upside

There are many things to like about ArcelorMittal. Like other steel and metal investments in Europe, such as ThyssenKrupp, the company has gone through a number of structural changes for the past few years, and it tries to change its operations to where it makes “sense” in this macro. This includes a fair bit of divestments and efficiencies.

The latest results we have are 2Q24, and these are “fresh off the presses”, less than a month old at this particular time. Plenty of positives, many of which I forecasted in my previous article, are seen materializing this quarter. It includes impressive organic growth, including an upswing in organic EBITDA by the end of -26, with positive net income upwards of $1.4B for the 1H24 period.

The company is still active in the M&A department. MT bought Italpannelli construction business, a significant 25%+ stake in Vallourec among other things, which is expected to add a premium, high-margin cash-generating business to the company’s balance sheet. Debt is still low despite these market moves, currently coming in at less than $5.5B net, with $11.4B in liquidity. The company is also taking advantage of the very low valuation by repurchasing shares. As of 1H24, over 4% of the company’s SO has been bought back, and the company estimates a BV of $66/share for the MT ticker.

Again, dividends are not the main reason why you invest here – it’s more total returns. The company is continually improving its assets, and this is shown in the current company forecasts.

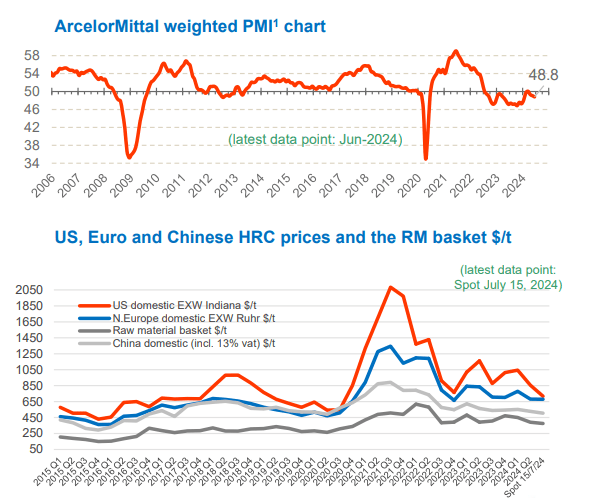

Despite what you see from company performance here in terms of share price, ArcelorMittal has been doing well. There’s a current imbalance in trade fairness that is impacting most metal companies. If you, like me, believe that this is going to be fixed in the future, then chances are good that companies that dominate these markets regionally are going to see very good returns.

MT is also delivering strategic growth projects. The reason why the company is down is instead, as I see it, macro concerns, and MT doesn’t control macro. I’m talking about weaknesses not only in LVP but also in Manufacturing and Machinery output – all of which are negative numbers for the YoY period between Months 1 and 5 this particular year. And when you combine this with excessive Chinese exports due to their own domestic low consumption (given their slowdown), this means that much of the cheap Chinese steel is being “dumped” here – at least for now.

Despite this, MT has been holding up fairly well.

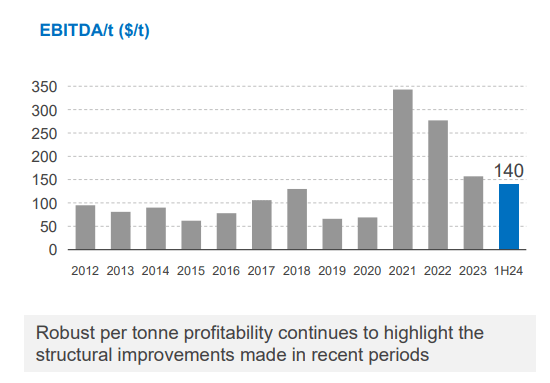

ArcelorMittal IR (ArcelorMittal IR)

As the company says, the improvements here are structural, and consistent over the past number of years. The level of EBITDA we’re seeing here is well above weak or even strong periods in the past, despite the market softness we’re seeing here.

What I am trying to convey to you is that we’re seeing a near-cyclical low, not any sort of “high” trend, and despite this, the company is doing well. It’s my opinion that this is the time to buy companies like this, not stay on the sidelines.

ArcelorMittal IR (ArcelorMittal IR)

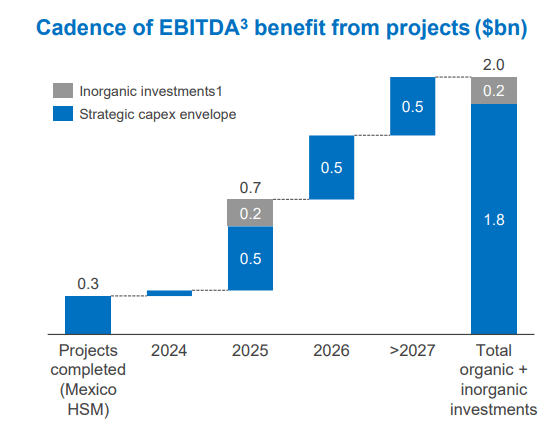

Because once ArcelorMittal is recovering, the upside we’re going to see here will be non-trivial – that part seems all but certain to me. The company has been pushing money to work on high-growth projects, and we’re going to see the fruits of those labors. This includes a near-$2B EBITDA increase by the year-end of 2026, as well as the additions from inorganic investments like Vallourec – the company’s share of this net income, will be around $150M per year, which means the company bought the 28% stake at a net multiple of ~6.6x – not exactly excessively expensive.

ArcelorMittal IR (ArcelorMittal IR)

ArcelorMittal also owns a fairly impressive renewable portfolio, which already has things going in Brazil, India, and Argentina. This is the company’s strategy for decarbonizing its steel manufacturing, rather than trying to change the way of manufacturing itself, like Swedish manufacturer SSAB is doing. I consider the way that ArcelorMittal is doing it to be superior at this particular time.

Remember, the company is targeting a doubling of the company-wide annual EBITDA. The reason I am investing in MT is because I believe this doubling to actually be feasible.

How?

I forecast that increased specialization combined with scale, growing its footprint in growth areas (I’m not allergic to growth markets as some investors seem to be, such as EMEA and India), coupled with inorganic growth and the decarbonizing of production through more mundane methods, i.e. renewable JV’s.

The company is already preparing for this, by enabling growth in the top line through higher input material availability.

ArcelorMittal IR (ArcelorMittal IR)

So, in short – 1h24 was good, and 2Q24 was good as well. The negatives come from factors the company does not control, including an illegal blockade in Mexico, lower PCEs in India, and lower shipments due to planned maintenance. Also, mining saw a negative impact due to iron ore reference prices.

Despite everything the company is doing, the balance sheet is hardly changed from a year ago – an increase of about $700M, but given that ArcelorMittal invested $1.5B from which it got $2.6B of investable cash flow, the company is getting a very good potential ROI. And the things about the Chinese mentioned, well, many of those are being addressed as well.

ArcelorMittal IR (ArcelorMittal IR)

I’m never “happy” that an investment I made is going down, but I am very happy to see that I can pick up this IG-rated steel company at a great price – and that is what I am doing here.

Let me show you the valuation for ArcelorMittal.

ArcelorMittal – Valuation shows a potential upside

So, given that we’re talking about a book value of around $66/share, you can already tell that this company is not “properly valued” here because we’re now talking about 33% of that book value or a 0.33x multiple. That is ridiculous to me, and this alone is enough for an investment here.

ArcelorMittal’s historical valuation levels are somewhat tricky, given the incredible volatility of its earnings over the past 20 years – but I’d be willing based on normalized valuation to go, aside from a 0.5-0.7x BV, to around 10-13x P/E, or around 11-12x normalized and weighted, which comes to an implied FV of $35/share for this year. But this is really only the beginning.

I say this because the company is expected to generate upwards of 30%+ annualized EPS growth for the next few years.

If this even comes close to the truth, then a normalized conservative multiple would imply triple-digit returns here to the tune of 150%, even at a low 10.9x P/E (Source: Paywalled F.A.S.T graphs link)

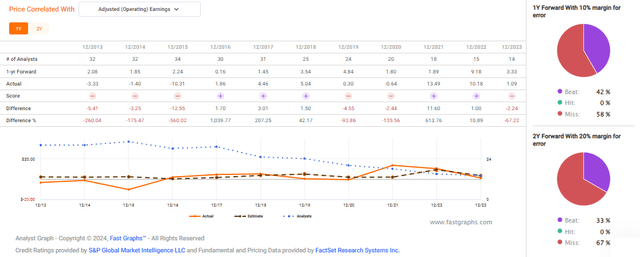

The arguments against such an investment are really limited to the company’s yield, and the difficulty of forecasting it. And when I say difficulty, I do mean difficulty. Because analysts just can’t get it right with this company. They either overshoot or undershoot the mark here.

F.A.S.T Graphs Forecast Accuracy MT (F.A.S.T Graphs Forecast Accuracy MT)

So if you want a nice, stable steel company with a good upside, something safe to hold, then ArcelorMittal is decidedly not for you.

However, if you’re willing to wait for an upside, the company does have all the signs you’d want that the next 3 years would result in a higher share price than we see today. And that 150% upside in total RoR, that’s the conservative target. A 15x P/E would imply over 200% RoR here. It’s also wrong to say that the company has never been upwards of $50/share during its history – because it has.

ArcelorMittal is also likely to continue to grow. Why? Because the current macro trends are in favor of growth for these segments, including things like population growth, a growing middle class, higher demands for specialization and customization, the circularity of steel and metals, and so forth. Even without China, the steel demand across the world is likely to be 35% over the next decade, including a doubling in demand from India, 15% growth in the EU, and 20% growth in the US.

This outweighs all of the risks I see for the business, including the ongoing volatility.

My previous target for MT was $37/share. I’m upping this to $40/share, or a conservative 0.5x to the company’s BV, and going “BUY” here. I’m increasing my position in MT.

Thesis

- My these are for ArcelorMittal is currently a positive one for one of the leaders in global steel. I view the company as investable on the basis of its sector-leading low debt and coverage and decent upside. There are “better” investments out there, meaning higher upside with decent safety, but if you want exposure in this sector, there aren’t many companies that can measure up to ArcelorMittal.

- Based on this, I go into the company with a “BUY” rating, and I’m planning to add to my current position in the business.

- My PT for MT remains conservatively $40/share, with the company currently trading at less than $30/share as of August 2024.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I won’t call the company “cheap” here, but it does fulfill all of my other criteria for investing, making it a “BUY”.

Read the full article here

")

Q1 2025 Earnings Call Transcript")

")