")

Summary

ATS Corporation (NYSE:ATS) out of Canada is a play on automation growth in the manufacturing sector with exposure to electric vehicle battery outsourcing. While the cycle is right now putting a dent in near-term growth (with Goldman recently putting a sell on the stock), the long-term story remains a good one: labor shortages and insourcing trends will create elevated demand to add North American-based manufacturing capacity and improve efficiencies.

Also a plus, ATS sells and services manufacturers in many defensive industries: healthcare, consumer products/packaging, as well as sectors like energy and electric vehicles.

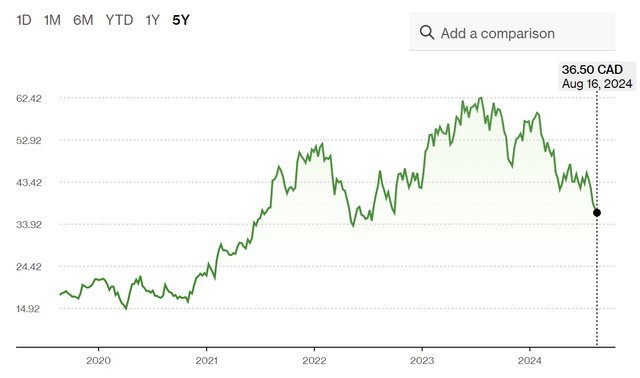

The stock has been killed in the past year, down 40% from its peak, as some large EV contracts have rolled off.

Below is a chart from Bloomberg.

Bloomberg

A stock in the automation industry, especially one with a Danaher type business system, won’t come cheap. Rockwell Automation (ROK) trades at 25.8x forward earnings and at 19x EBITDA. It is also off its highs, but not as much as ATS. We would point out that ATS has grown revenue about 3x as fast as ROK in the past five years, with EPS growth that is 40% better per year. ATS at $36.50 now trades at 16x next year’s earnings (year ending March 2025) and 10.6x fiscal year 2025 EBITDA.

It is worth pointing out that last year, ATS was a 22x P/E multiple stock.

The lowest multiple that ATS has traded historically was just under 14x during the pandemic. That suggests a 14% downside in the stock.

On the upside, ATS, we believe, is worth 12-13x EBITDA, which implies over 50% upside in a couple of years. On average over the past five years, ATS has traded at 12.3x forward EBITDA, so we feel that the upside case is quite conservative.

Recent Earnings

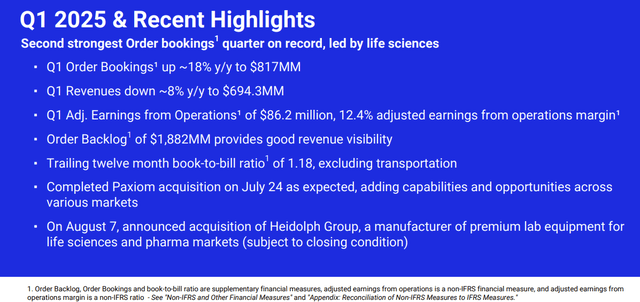

ATS reported a slight EPS miss in the June quarter. Revenues fell 8% as a lot of EV battery business rolled off compared to last year. Organic revenue growth was -12.7% in Q2. On the plus side, quarterly bookings were up 18% including some GLP-1 business as discussed on the call.

EBITDA fell 10% compared to a year ago but beat estimates by 1%.

EPS was $0.52, a 2c miss and down from $0.69 a year ago.

The company is cutting costs in their Transportation segment as EV sales slow and customers cut back on electric vehicle purchases.

The balance sheet looks fine too, with debt to EBITDA at 2.7x as of the end of June.

The company has 2 acquisitions lined up for Q3 (Paxiom closed in July and a deal to buy Heidolph Group was announced). These guys have an excellent M&A track record, so we are optimistic, but financial data is scarce so far. On the call, management simply said it was accretive on a gross margin basis and an asset they purchased out of bankruptcy.

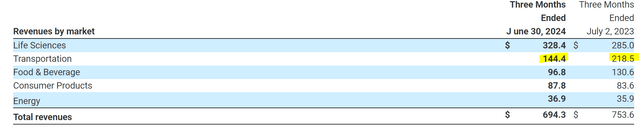

Below is revenue in Q2 by segment.

ATS Investor Relations

Excluding Transportation, revenue grew 3%.

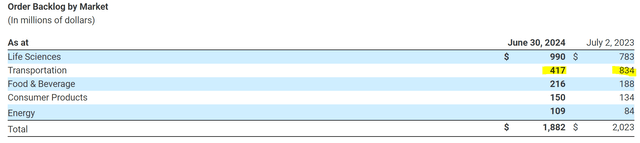

In the quarter, backlog remains depressed in Transportation of course, but is doing quite well across every other vertical.

ATS Investor Relations

Backlog growth ex-Transportation was 23% in Q2 compared to a year ago.

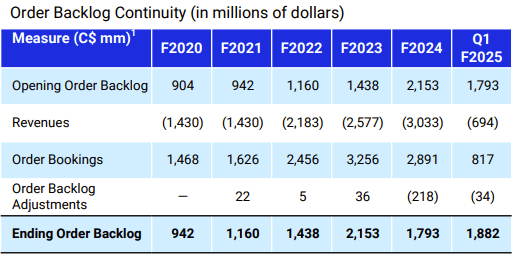

Here is backlog over the past few years.

ATS Investor Relations

Note that backlog is finally ticking up again after peaking in March 2023. Book to bill is 1.18x and bodes well for growth going forward.

Here is their most recent slide discussing order bookings:

ATS Investor Relations

Street estimate are $2.13 in EPS for 2025 (FY Ending March) and $2.60 the following year. Management discussed some margin pressure as the Transportation business winds down, and that could be a near term issues. Combined with the 2c miss to estimates, we are expecting $2.25 in EPS, give or take for the March 2025 FY.

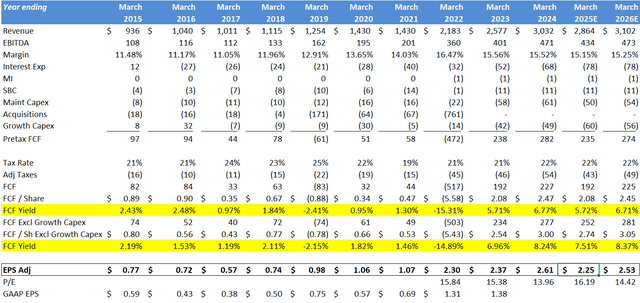

Here is our summary free cash flow and earnings model.

Company financials, Author spreadsheet

A Through the Cycle Compounder

Per the above, while near term results have been choppy with some large EV contracts rolling off in 2023 and 2024, that is mostly behind the company. Since 2015, ATS has clearly been a terrific Compounder, with EPS up almost 3x (using FY 2025 estimates, which looks like a trough year).

We credit the relatively new and young CEO for much of its recent success. Andrew Hider took charge in 2017 (after a long stint at Danaher) and has implemented many cultural changes that have improved margins, market share, and EPS. We have discussed the success of the Danaher Business System (DBS) in the past as it has created significant value across a range of niche manufacturers like Parker-Hannifin (PH), DHR and Flowserve (FLS) to name a few.

While the company has had a lot of long-term growth, there has been a lot of economic noise along the way. Most recently, investment in automation technology possibly peaked in 2022. It naturally lagged in 2020 during the pandemic, so much of its growth was driven by deferred orders and deliveries. Indeed, organic growth reached as high as 20% in 2021 (in certain quarters), before slowing to 5.5% in the June 2022 quarter. The most recent earnings report showed organic revenue falling 12.7% (the June 2024 quarter), but as discussed, new order bookings are lately strong, with total backlog up 5% sequentially.

We know the story with tough comps. ATS has been in the penalty box for several quarters now as the world normalizes, but the company looks poised to grow again. We also view their EV business as potentially a “free option” should demand pick up in the space.

In the long term, we love the secular trend toward spending on increased manufacturing capacity and efficiencies in ATS’s core markets (US and Europe). There are always manufacturers looking to improve margins, and re-sourcing trends can only aid this growth.

We view ATS as a solid Compounder, noting the following:

– Revenue has grown organically by 7% over the past five years;

– EPS has compounded by 12% annually since 2016, up over 3-fold;

– EPS has compounded by 22% annually since Eric Hider took over;

– The balance sheet is solid at 2.7x on a debt/EBITDA basis, intending to keep leverage below 3.0x;

– A terrific CEO who hails from Danaher; and

– A strong acquisition track record.

Risks include a recession, which could slow spending among many manufacturers. Europe certainly faces weak growth today and while ATS has a solid acquisition track record, they could make a mistake in this regard. Also, the company collects revenue in a variety of currencies and so there is F/X risk here.

Valuation Thoughts

While ATS could sit in the penalty box for a few more quarters, we believe in a year, at its average 19x P/E multiple, ATS is a $48 stock (in Canadian terms, from $36.50 in C$ today). That is an upside of 11% and a decent base case.

With smaller names, we often do more diligence than more established companies, given the elevated risks with a small cap. With ATS, we spent a little time speaking with the CFO on a range of topics. We also gathered intel from other industry insiders.

One buysider believes that IMA (Industria Macchine Automatiche) based out of Italy, might be an interested buyer of ATS. IMA is owned by a private equity consortium including BC Partners, BDT, and MSD Partners. This group purchased IMA in January 2021 for 14x 2020 EBITDA and 12x forward EBITDA estimates.

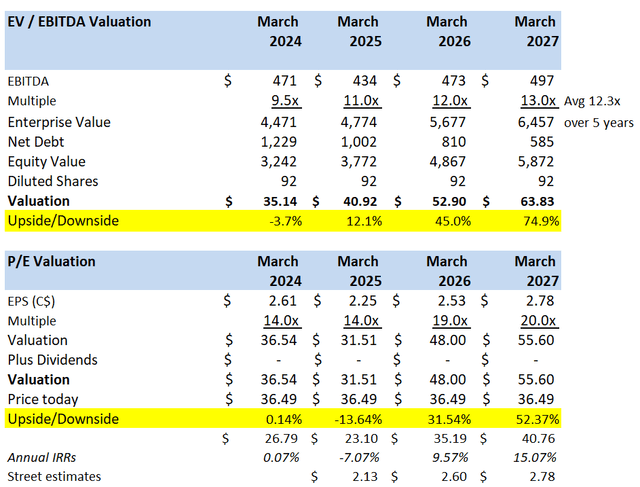

At 12x forward EBITDA, ATS has 45% upside.

Here are some valuation scenarios.

Company Financials, Estimates, Author Spreadsheet

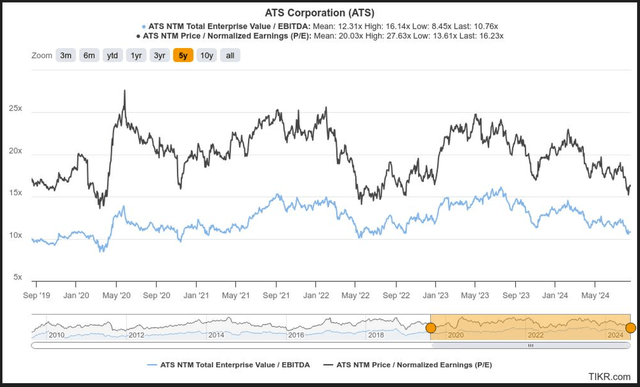

Here is a chart illustrating ATS’s average forward multiples on both an EV/EBITDA basis and a P/E basis. The stock is close to pandemic lows.

TIKR.com

While ATS reports in Canadian dollars, the stock is actively traded on the NYSE in US dollars too. We own the USD version.

Buy.

Read the full article here

")

Q1 2025 Earnings Call Transcript")