")

After the “growth scare” that was instigated two weeks ago by the July jobs report, it is nice to have good news on the economic front be good news for the market again, and we had it in spades last week. Both the producer (PPI) and consumer (CPI) inflation reports were better than expected, and the upcoming core personal consumption expenditures (PCE) price index report for July, which dictates monetary policy, should fall to a new low of 2.5% for this cycle. That should seal the deal for the first rate cut of 25 basis points to occur at the Fed’s September meeting, which I think Chairman Powell may subtly acknowledge during his speech in Jackson Hole on Friday. I continue to think that the inflation gauges are on track to reach the Fed’s target of 2% by the end of this year, as the government’s calculation for shelter costs, which operates with a lag, catch up with current prices.

Edward Jones

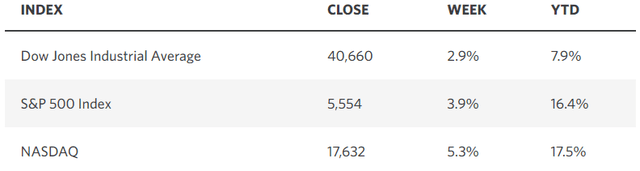

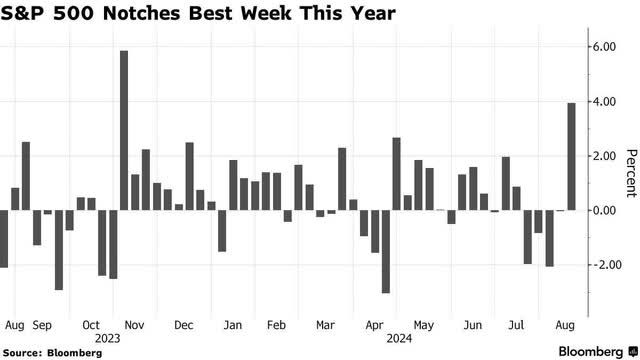

Initial unemployment claims fell for a second week in a row to a level that indicates July’s soft labor market numbers were more weather related than an indication of an impending recession, as those more pessimistic have suggested. Retail sales for July also refuted recession claims with a stronger-than-expected 1% increase over the prior month. While auto sales led the way, 11 of the 14 categories tracked saw increases in what was broad-based strength. It was this combination of disinflation and resilient economic growth that fueled the best-performing week of the year for the S&P 500 index. To top it all off, the University of Michigan’s consumer sentiment index rose for the first time in five months.

Bloomberg

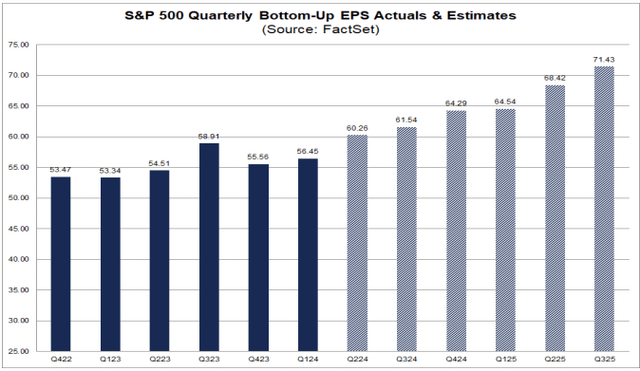

With the second-quarter earnings season about to wrap up, profits for the S&P 500 are on track to increase by 10.9% compared to expectations of 8.9% at the end of the quarter. That would be a new quarterly record of $60.26. Furthermore, the percentage of companies that are issuing negative guidance for the current quarter at 55% is below both the 5-year (59%) and 10-year (63%) averages.

FactSet

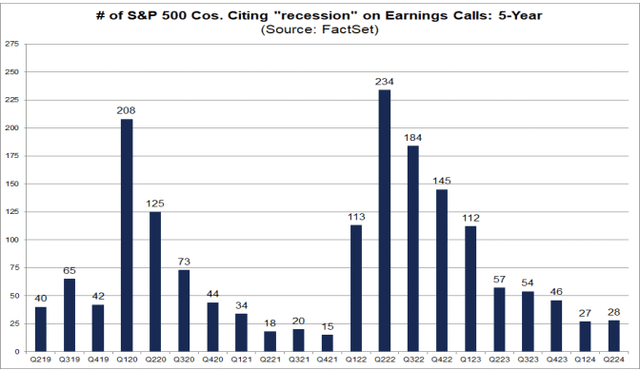

Since corporate executives are on the front lines of the economy, they have greater insight than most as to when activity is starting to slow at an alarming rate. Based on the number of times they mentioned the word “recession” during earnings conference calls over the past month, I would say we don’t have a lot to worry about at this point. Anticipating the end of the current business cycle is my primary focus and concern as an investor, for it will dictate a far more defensive position with respect to my investment strategy. In aggregate, positive rates of change in the high-frequency economic data continue to trump those that are negative. Until we see that change, the expansion should continue.

FactSet

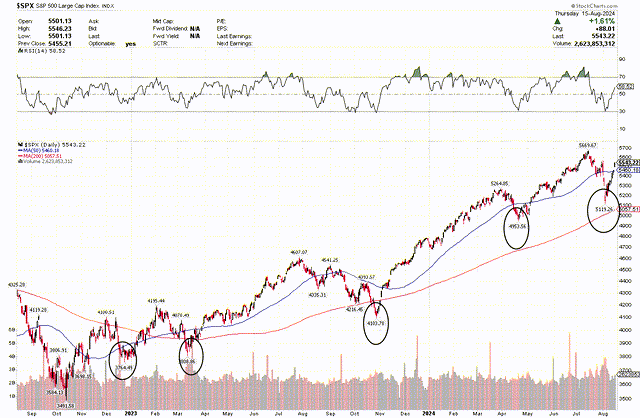

This is why I have been steadfast over the past two years in advising investors to “buy the dip” during each drawdown in the stock market. We just had the fifth pullback in the S&P 500 since the bull market started in October 2022, among which there was one correction of 10%. It has paid a lot more than dividends to buy those dips along the way, as the S&P 500 has risen 57% so far, which is modest in the context of the average bull market. On each decline, there were plenty of reasons to turn bearish, but the weight of evidence consistently leaned towards disinflation and a softer but steady rate of economic growth, which typifies a soft landing for the economy.

StockCharts

I realize this conclusion frustrates many investors, as well as market pundits, who are critical of the fiscal and monetary stimulus that has served as the fuel for this expansion and bull market, as well as the soaring deficits and debt. I sympathize with their concerns, but that does not nullify the economic growth or market returns. It may have a lot to do with the sustainability of both, but that is not yet an issue. It is in the back of my mind. From an investment standpoint, I don’t want to allow my ideological views or opinions about what the market should or should not do to interfere with a pragmatic analysis of the economic and market fundamentals. My focus is on what the economy and markets are most likely to do, as the business cycle runs its course.

Read the full article here

")

")