")

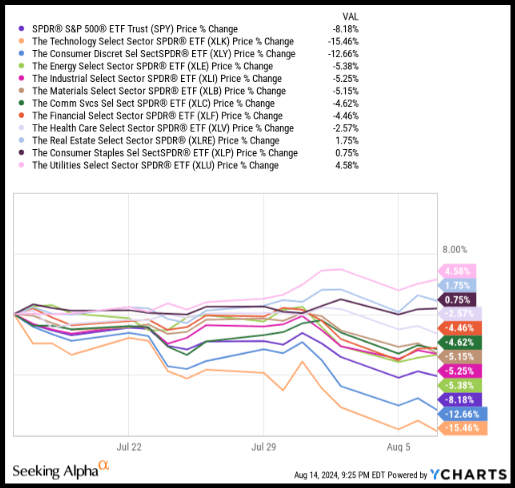

The S&P 500 fell over 8% in a three-week selloff amid fears of recession. The market bounced back last week despite big tech AI bubble fears triggered by weak jobs data and uncertainty over the impact and timing of Fed emergency rate cuts. The Tech (XLK) and Consumer Discretionary (XLY) sectors led the free fall, plunging by 15% and 12%, respectively, followed by the Industrial (XLI) and Energy (XLE) sectors, which both fell over 5%. Three defensive sectors – real estate, staples, and utilities – were the only ones to post positive returns during the market’s three-week slide. Healthcare stocks (XLV), historically a safe haven amid a downturn, outperformed and fell over 2% during the same period. The markets rebounded and continued to rise after CPI data indicated headline inflation reached below the 3% consensus estimate, setting up the Federal Reserve to start cutting rates in September.

S&P 500 Summer Sell-Off by Market Sector (July 16 – Aug 7)

Summer Sell-Off: Sector Performance (SA Premium)

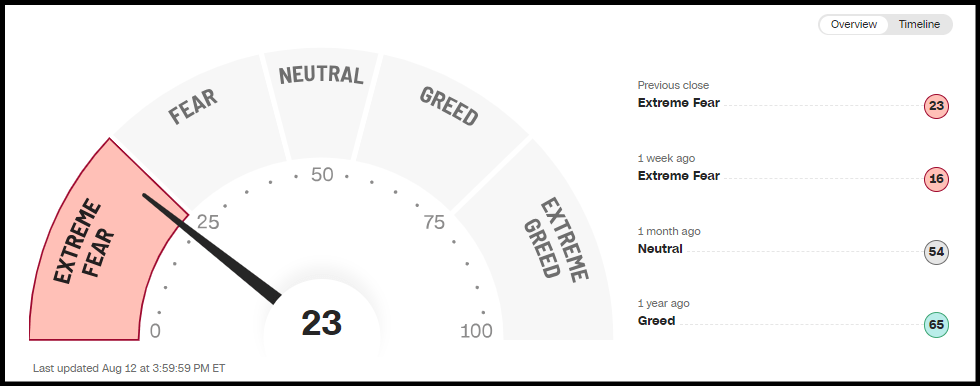

The drop triggered a search for safer investments as the CBOE Volatility Index “fear gauge” soared to pandemic-era levels amid economic uncertainty, in sharp contrast to the greed that was the main impetus a year ago. Investments in recession-proof sectors like those highlighted in 4 Best Defensive Stocks For A Potential Soft Landing have become more appealing.

Fear & Greed Index

Fear and Greed Index (CNN)

At the same time, the plunge has a potential silver lining because stocks possessing strong investment fundamentals retreated during the period and look more attractive than ever.

Down But Not Out: Be Greedy When Others Are Fearful

Using Seeking Alpha Quant Ratings and Factor Grades, we selected six stocks that retreated during the recent sell-off and were beaten down throughout the year despite consistently topping earnings. The stocks on the list have been down by double digits in the last 30 days, six- and 12 months, have Buy or Strong Buy Quant Ratings and are trading at attractive valuations. The stocks span varied sectors and exclude market caps under $500M or those lacking meaningful earnings growth data. First up, Carnival Corporation.

1. Carnival Corporation & plc (CCL)

-

Market Capitalization: $19.69B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 8/16/24): 8 out of 506

-

Quant Industry Ranking (as of 8/16/24): 2 out of 36

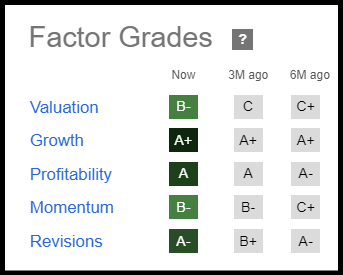

Carnival has retreated over 15% in the past month despite sound investment fundamentals, showcasing A’s in Growth, Profitability, and Revisions and B’s in Valuation and Momentum. Ranked #2 among quant-rated Hotel, Resorts and Cruise Lines stocks, CCL was hit hard as a hurricane tore through the Caribbean, overshadowing another quarter of solid earnings results, beating the consensus EPS target for the seventh time in 8 quarters.

CCL Factor Grades (SA Premium)

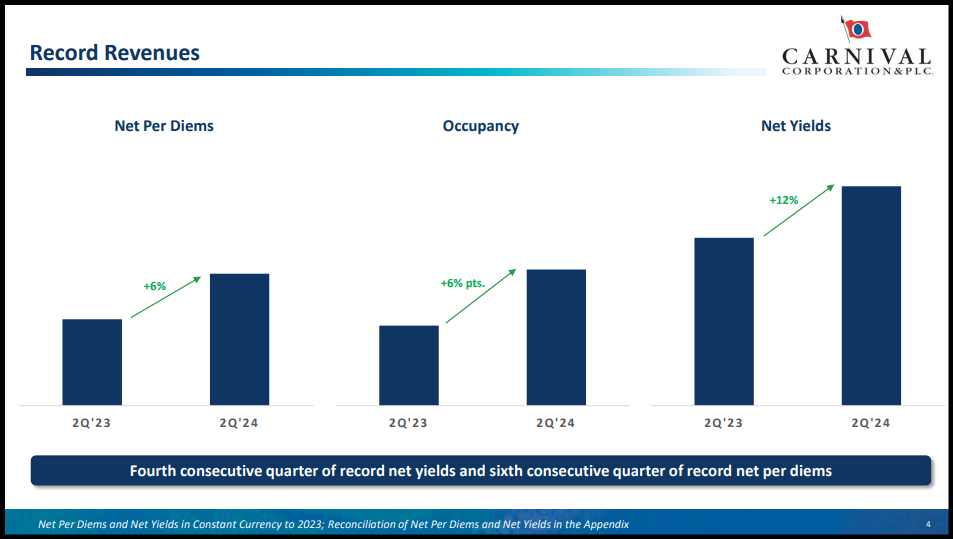

Carnival delivered record Q2 results, exceeding guidance across revenue, operating income, customer deposits and booking levels. In addition to record net yields and net per diems for the fourth consecutive quarter, CCL is confident about future profitable growth on soaring demand for 2025, CEO Josh Weinstein said in an earnings call:

“The unprecedented level of demand for 2025 sailings coupled with flat capacity growth next year translates into meaningful pricing power… both price and occupancy are already ahead of where we were last year, leaving us in a position of strength with less inventory remaining for 2025.”

CCL revenue TTM rose +34%, EBITDA +310%, and operating cash flow +516%, driving an A+ Growth Grade. CCL gross profit margin of 51%, EBITDA margin of 22%, and capex/sales of 21% crush the sector medians for an ‘A’ Profitability Grade.

CCL Q2 Results (Investor Presentation)

CCL has 19 upward revisions to 1 down revision in the last 90 days, with the consensus projecting EPS by 33% in FY24 and revenue +13%. According to the average Wall Street sell-side analysts’ price target, CCL has a potential upside of +46%.

2. Trip.com Group Limited (TCOM)

-

Market Capitalization: $27.35B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 8/16/24): 13 out of 506

-

Quant Industry Ranking (as of 8/16/24): 8 out of 36

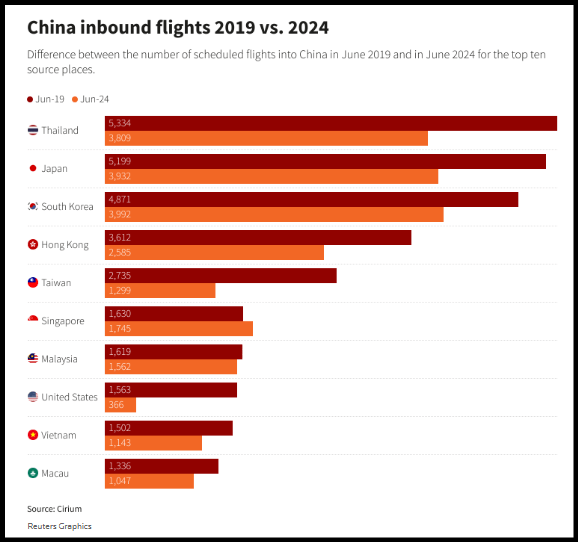

Trip.com is a Shanghai-based online travel service provider. Used for booking accommodation reservations, transportation ticketing, packaged tours, and corporate travel management, TCOM tumbled over 10% in the last 30 days. This slide in performance may seem puzzling in light of China’s hot travel season, marked by a +150% rise in foreign visitors in H124, a surge in domestic travel, and +40% uptick in summer long-distance travel orders. Fueled by Beijing expanding its visa-free policy, inbound flights exploded in the month of June versus pre-pandemic levels. Thailand (+40%), Taiwan (+111%), and Japan (+32%) accounted for most of the growth in number, and the U.S. origin saw the largest percentage boost, up 327%. In the first quarter, Trip.com saw a 400% increase in inbound bookings and +100% in outbound bookings.

China Inbound Flights in June (Reuters)

Trip.com’s EPS forward growth rate is +129%, and it is crushing the sector in profitability, evidenced by a gross profit margin of 80% and an EBIT margin of 26%. TCOM has an attractive valuation per its forward PEG of 0.29x, a discount to the sector of nearly 80%, and 20 upward revisions in the last 90 days.

3. Amphastar Pharmaceuticals, Inc. (AMPH)

-

Market Capitalization: $2.21B

-

Quant Rating: Buy

-

Quant Sector Ranking (as of 8/16/24): 98 out of 1036

-

Quant Industry Ranking (as of 8/16/24): 17 out of 193

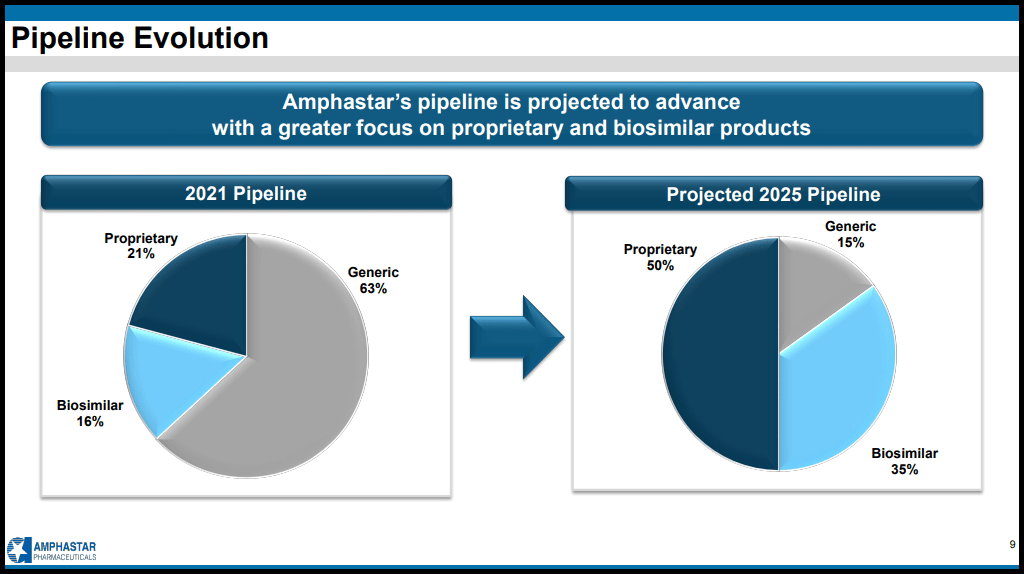

Amphastar is a vertically integrated pharmaceutical company with a strong base of FDA-approved products like Primatene MIST and the BAQSIMI diabetes treatment. Although AMPH is up over 10% in the last 30 days, the stock has been beaten down by 20% in the past year. AMPH surged by double digits after a Q2 earnings beat, exceeding expectations for the sixth time in eight quarters. Amphastar’s momentum has steadily improved in the past three months, up 2% vs. -8% for the healthcare sector, as its Quant Rating rose from a Hold. AMPH Q2 revenue soared +25% YoY to $182.39M, driven by a focus on higher value markets led by the BAQSIMI glucagon nasal powder, a strategic acquisition from Eli Lilly, which accounted for $30.85M in Q2 sales (~17% of total revenue). Amphastar’s pipeline is advancing toward a greater focus on high-margin proprietary and biosimilar products, with the generic portion expected to shrink dramatically by 2025. AMPH has seven products in development and four on file with the FDA, targeting a combined annual market size of over $13B, according to IQVIA data.

AMPH Pipeline (Investor Presentation)

Key growth catalysts for H224 include expected approvals of three products, two new filings, and the planned launch of Amphastar’s albuterol sulfate inhalation aerosol. According to IQVIA data, branded and generic albuterol sales were roughly $1.6B in the trailing twelve months. AMPHA will focus on boosting the promotion and market share of BAQSIMI, Primatene MIST, and the Glucagon injection kit recently launched in Canada. Amphastar delivered massive top and bottom line growth in the trailing 12 months and has exhibited solid earnings growth potential for an A- Growth Grade. AMPH showcases sector-crushing profitability with an EBITDA margin of nearly 40%, net income margin of 23%, and ROE of 25%. AMPH is trading at a mere 11x earnings, an attractive valuation, representing a 47% discount to the sector, and a forward PEG of 0.78 implies a discount of 58%. AMPH has 6 upward earnings revisions in the last 90 days.

4. Corporacion America Airports S.A. (CAAP)

-

Market Capitalization: $2.57B

-

Quant Rating: Buy

-

Quant Sector Ranking (as of 8/16/24): 73 out of 630

-

Quant Industry Ranking (as of 8/16/24): 2 out of 6

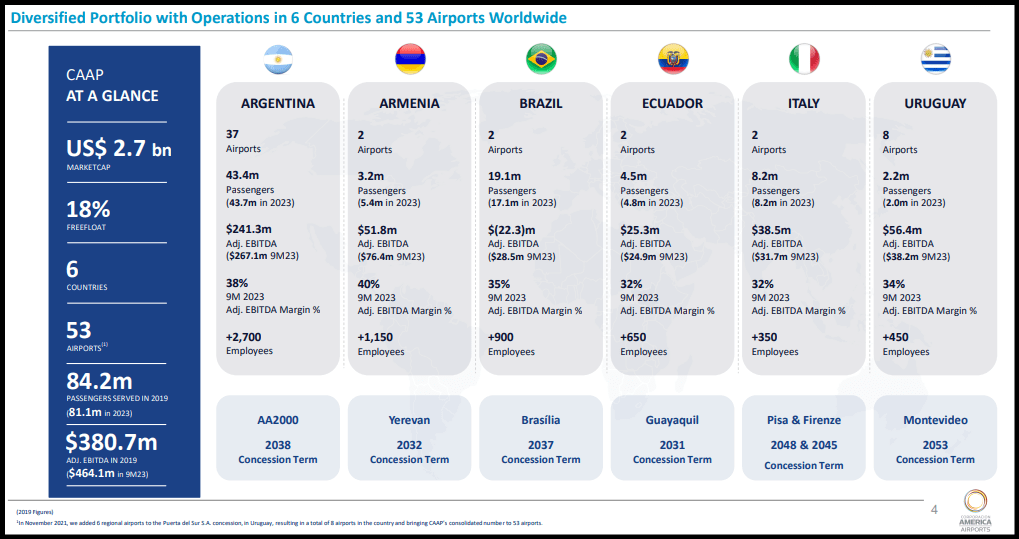

CAAP is the #2 quant-rated Airport Services stock, down ~10% in the past 30 days after getting clipped by the broader market sell-off and reporting declining passenger traffic. CAAP operates 53 airports in six countries, including 37 in Argentina, deriving revenue from aeronautical and commercial services. CAAP’s key financial growth driver is passenger traffic, which generates aeronautical and commercial services revenue. A majority of revenue comes from fees charged to departing passengers, aircraft landing and parking fees, and use of CAAP premises. CAAP also earns revenue from warehouse usage, retail, food and beverage shops, and advertising.

CAAP Portfolio (Investor Presentation)

Aside from recent momentum declines, CAAP possesses solid investment fundamentals and proven and potential earnings power. EPS grew 108% in the trailing twelve months, operating cash flow +50%, and EPS forward is at +30%. CAAP has beaten earnings targets in seven of the past eight quarters. FY24 EPS is projected to grow 20% and revenue +13.5%, according to consensus estimates, and the stock trades at a 98% discount to the sector, showcased by a trailing PEG GAAP 0.06x vs. 0.98x while price/cash flow of 5.4x is at a 61% discount.

5. Twilio Inc. (TWLO)

-

Market Capitalization: $9.75B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 8/16/24): 44 out of 551

-

Quant Industry Ranking (as of 8/16/24): 2 out of 25

Twilio is up in the last 30 days (+4.5%) but beaten down over the past year (-1%), a bit of a mystery given its strong earnings track record, including eight straight double beats, a staggering 28 upward earnings revisions in the last 90 days. Listed at #2 among quant-rated Internet Services and Infrastructure stocks, Twilio offers technology platforms to enhance end-user engagement via messaging, voice, email, flex, marketing campaigns, and user identity and authentication. Twilio surged on analyst upgrades, citing signals of success from go-to-market initiatives and packaging solutions boosting stickiness and cross-sell opportunities.

TWLO Revisions Grade (SA Premium)

Twilio sees itself as uniquely positioned for more growth by offering communications capabilities, contextual data, and the power of AI, enabling brands to boost customer engagement and drive more revenue at a lower cost. In addition to earnings projected to grow +30% in FY24, Twilio has levered FCF margin of 21% and is trading at a 68% discount to the sector based on a forward PEG of 0.59x.

6. Sterling Infrastructure, Inc. (STRL)

-

Market Capitalization: $3.52B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 8/16/24): 38 out of 630

-

Quant Industry Ranking (as of 8/16/24): 7 out of 32

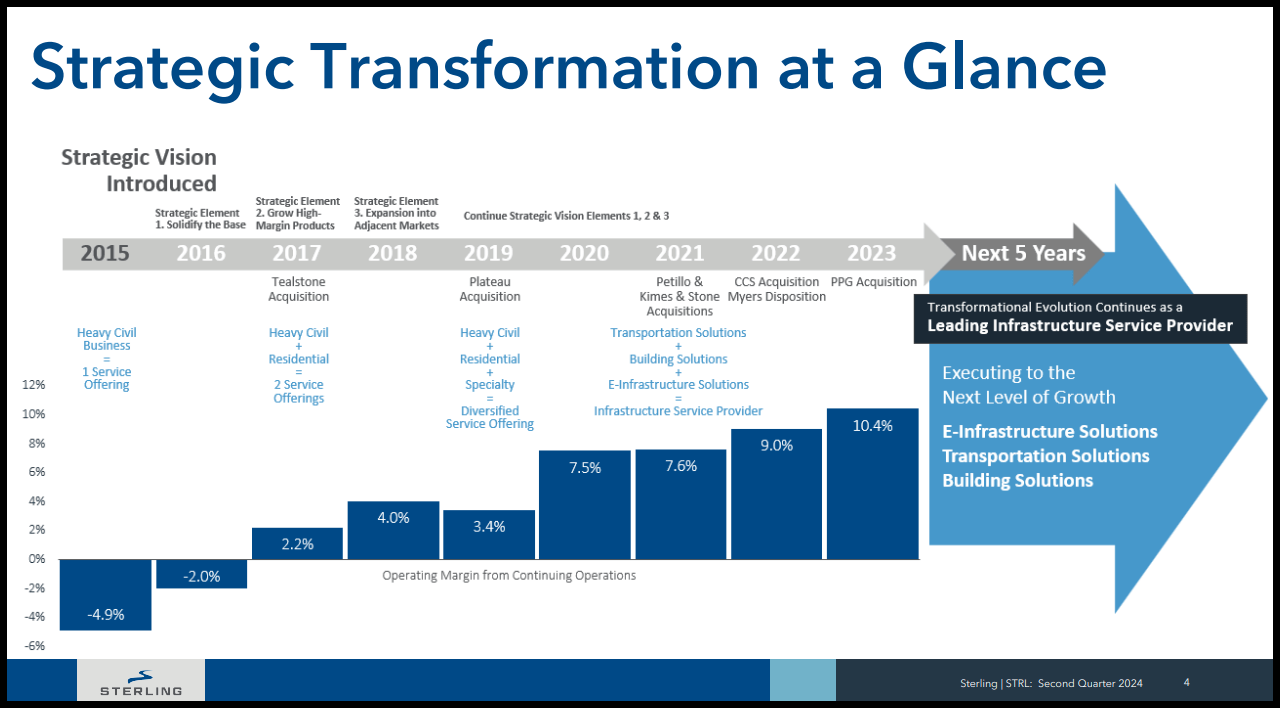

Sterling is a Texas-based provider of e-infrastructure, transportation, and building solutions primarily in the United States, down 13% in the last month but +38% in the last year. Sterling beat revenue and earnings expectations for Q224 and raised full-year guidance. Exhibiting the strength of its diversified portfolio and ongoing focus on margin expansion, Sterling beat its EPS target for the eighth straight quarter. EPS of $1.67 beat by $0.24 and revenue of $582.83M (+11.6% YoY) beat by $22.97M.

STRL Strategic Plan (Investor Presentation)

Through its strategic transformation and vision, gross profit margins of 19.3% set a new record for Sterling and backlog rose 2.2% YoY to $2.45B. Sterling’s pipeline of large multi-phase projects, not captured in backlog metrics, grew over $500M, providing multi-year visibility. EPS is projected to rise +26% in FY24 after delivering YoY growth of 46% in the trailing twelve months. Sterling has an A- Profitability Grade driven by ROE of 26% vs. 12% for the sector, a solid 16% levered FCF margin, and cash per share of $17.49 vs. $2.07 for the sector, a difference of 745%. Sterling has a solid valuation with PEG FWD of 1.28 and price/cash flow of 7x representing 25% and 48% discounts to the sector, respectively. While each of the six stocks referenced in this article has taken a beating over the year, amid market uncertainty, they are down, but not out!

Concluding Summary

The recent three-week market sell-off, sparked by recession fears led by falling tech and cyclical stocks, offers opportunities to scoop up stocks with high top or bottom-line growth prospects and attractive valuation frameworks. SA Quant identified six stocks that tumbled in the past 30 days or have been beaten down in the past 12 months despite solid investment fundamentals and strong earnings track records. We have many stocks with buy and strong buy recommendations, and you can filter them using stock screens to suit your specific investment objectives. Consider using Seeking Alpha’s ‘Ratings Screener’ tool to help find stocks that achieve diversification into desired sectors you like. Or, if you’re seeking a limited number of monthly ideas, consider exploring Alpha Picks.

Read the full article here

")