")

")

Overview

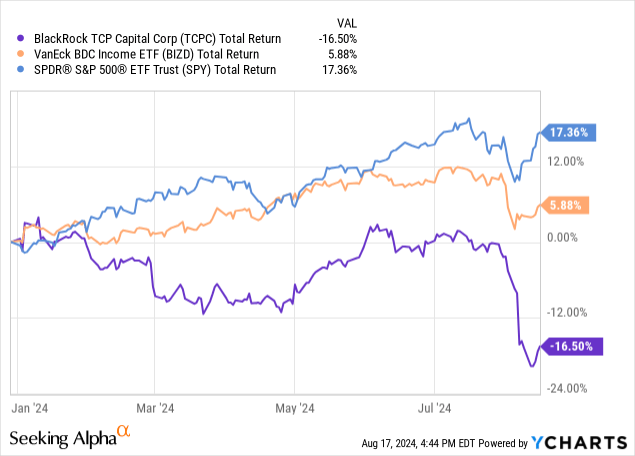

The last time I covered BlackRock TCP Capital (NASDAQ:TCPC), I issued a hold rating because I was uncertain of the portfolio strength in an elevated interest rate environment. Since my prior coverage over a quarter ago, TCPC has deteriorated in price by nearly 14% while the S&P 500 increased by 7%. If we do a quick comparison on a YTD basis, we can see that TCPC’s total return has been negative 16.5%. This significantly underperforms VanEck’s BDC Income ETF (BIZD). TCPC recently released their Q2 earnings at the beginning of August, and this prompted me to revisit this BDC to see how performance and outlook may have changed.

BlackRock TCP Capital operates as a business development company that generates its earnings by making various forms of debt investments to middle market companies. However, the range at which TCPC considers a company ‘middle market’ is quite large considering that they commit to investments with companies that have enterprise values ranging from $100M to $1.5B. With investments in larger companies, I would’ve originally thought that this BDC would offer a more reliable earnings history, but this doesn’t seem to be the case.

One of the main appeals of TCPC is the fact that this BDC provides investors with a large dividend yield of 17.8% following the most recent price drop. If the current distribution can be sustained in the future, this would be a great opportunity to lock in a large source of cash flow. Additionally, the high dividend yield allows for rapid compounding of your income over time. This would be a great tool for retired investors that may depend on the income generated from their portfolio. However, I believe that a future distribution cut may be in TCPC’s future due to rising non-accruals and the potential impact that interest rate cuts will have on the net investment income.

Portfolio Strategy

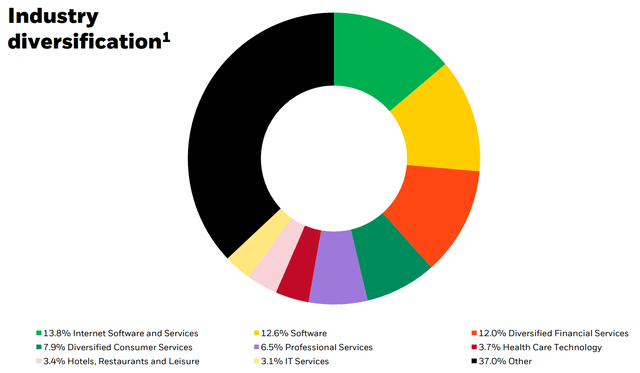

TCPC maintains a diverse portfolio of holdings with exposure across most industries. However, there is a majority weight in investments leaning in the internet software and services industry, accounting for 13.8% of their portfolio. This is closely followed by exposure to software companies and diversified financial services, accounting for 12.6% and 12% respectively. This widespread level of diversification helps mitigate any sort of concentration risk and can soften the impact of bear markets. Their portfolio of investments contains 158 different individual portfolio companies with a debt to equity ratio of 1.35x.

TCPC Q2 Presentation

TCPC is so diverse that more than 75% of their portfolio companies contribute less than 1% of their recurring income. Their portfolio of investments sits at a value of $2B at fair value and has a weighted average yield of 13.7%. Something that I like about TCPC is that approximately 91% of their debt investments are on a senior secured basis. This is notable because it means that the bulk of their debt investments are issued at the top of the corporate capital structure, which helps reduce the likeliness that all invested capital is lost in a bad deal.

Debt issued at the top of the capital structure has the utmost highest priority for repayment is cases of default. If a portfolio company underperforms and defaults on the debt, TCPC’s debt is the first on the list to get repaid when liquidating assets. More specifically, 81% of their portfolio is issued on a first lien senior secured basis and 10% is on a second lien senior secured basis. The remaining portions are comprised of exposure to both junior debt and equity investments. Equity sits at the bottom of the capital structure and takes on the most risk since it has the least repayment priority. This may leave a portion of TCPC’s portfolio a bit more vulnerable to defaults.

Lastly, 97% of their debt investments were also made on a floating rate basis. This has helped TCPC pull in higher amounts of income while interest rates remain elevated. Higher rates directly translate to higher amounts of interest income that TCPC can collect from borrowers. However, this also means that earnings can be impacted by interest rates being cut.

Financials & Risk Profile

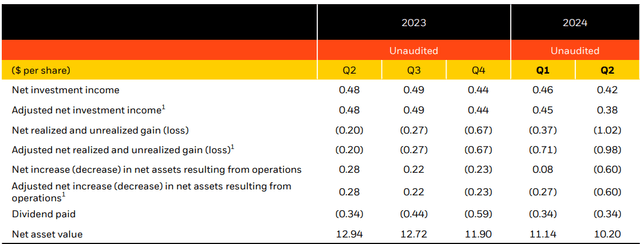

At the beginning of August, TCPC reported their Q2 earnings and the results were a bit mixed. On one hand, adjusted net investment income landed at $0.38 per share, but this missed expectations by $0.05. This is a decrease from the prior quarter’s adjusted net investment income of $0.45 per share. However, total investment income grew by a whopping 32.6% year over year, totaling $71.53M. Most of the losses in adjusted NII were driven by net realized losses of ($0.98) per share.

TCPC Q2 Presentation

These losses also resulted in the deterioration of TCPC’s NAV (net asset value). We can see that a year ago, TCPC’s NAV sat at $12.94 per share, but this has since fallen down to $10.20 per share. This amounts to a NAV reduction of about 21.2% over the last year. I believe the risk has also elevated since the debt to equity ratio has grown to 1.35x, up from the prior year’s debt to equity ratio of 1.17x. This simply means that TCPC is using more debt to fund some of these investments, but this can increase risk and amplify losses if these do not work out.

I also noticed that TCPC may not be growing their portfolio at a fast enough rate to offset the hit in net investment income. For instance, gross acquisitions for Q2 totaled $129.6M. However, TCPC also had exits, including repayments, equal $184.9M which nets out to an overall reduction of $55.2M. On a more positive note, liquidity has improved, with cash and equivalents totaling $194.6M. This is an increase from the prior year’s total of $123.1M. This increased cash position can be strategically used to capture new deals at opportune times.

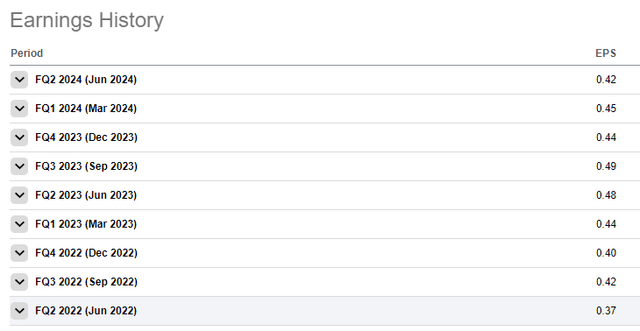

Interest rates were aggressively hiked to their decade high throughout 2022 and 2023 which helped TCPC pull in higher amounts of net investment income. Taking a look at the earnings history, we can see that in net investment income in Q2 of 2022 only amounted to $0.37 per share. As rates went up, so did the NII per share amounts. However, I believe that interest rate cuts may be on the horizon and this will negatively affect the earnings potential. Lower rates will mean that TCPC cannot pull in the same level of NII per share, since most of their portfolio operates on a floating rate basis. This would increase the risk of the distribution remaining the same.

Seeking Alpha

Speaking of risk, when I last covered TCPC, the non-accrual rate sat at 1.7% of fair value and 3.6% of cost. Non-accruals represent the rate of portfolio companies that are materially underperforming expectations and can no longer keep up with the required debt maintenance. As a result, companies in non-accrual status are no longer actively contributing to the earnings growth for TCPC and can limit the overall quality of their investment portfolio.

As of the most recent earnings call, non-accruals have significantly grown and now sits at 4.9% of fair value and 10.5% of cost. This indicates a weakening portfolio quality and has now reached levels that we should be concerned about. If the non-accruals continue to grow, this can also negatively impact the earnings for TCPC. Management addressed the issue on the last earnings call and reassured us that they were handling the issue.

Roughly 70% of the increase in non-accruals is related to just three companies: SellerX, Pluralsight and McAfee, most of which we have discussed in previous quarters. We have been working intensely with each of these companies towards a fulsome balance sheet restructuring that we believe can facilitate a path to recovery – Raj Vig, CEO

To be fair, rising non-accruals haven’t been unique to only TCPC. There are a handful of other BDCs that have also seen rising non-accruals as a result of higher interest rates. Even though a higher interest rate can produce larger amounts of interest income for TCPC, it can also put additional strain on borrowers as the cost of holding debt on the balance sheet increases. Here are some of the non-accrual rates of peer BDCs:

- Ares Capital (ARCC): non-accrual rate of 1.5% at cost and 0.7% at fair value.

- Blackstone Secured Lending Fund (BXSL): non-accrual rate of 0.3% at cost.

- FS KKR Capital (FSK): non-accrual rate of 4.3% at cost and 1.8% at fair value.

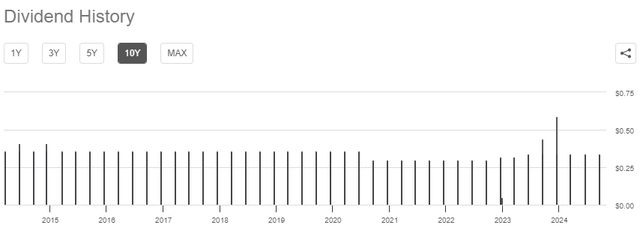

Dividend

TCPC recently declared a quarterly dividend of $0.34 per share, bringing the forward dividend yield up to 17.8%. If TCPC is able to turn things around and improve their portfolio performance, this could be a great opportunity to lock in a much higher yield than normal and add a source of high-yielding income to your portfolio. For reference, the four-year average dividend yield sits closer to 11.6%.

TCPC doesn’t have the best dividend history out there, with a cut taking place at the tail end of 2020 in response to lower earnings related to the market conditions surrounding the pandemic. The distribution has still not recovered to the same level prior to the pandemic. As a result, the dividend CAGR (compound annual growth rate) is actually negative over a five-year period, amounting to -1.14%. Even if we were to zoom out to a longer time horizon of a decade, the dividend has ultimately failed to show any meaningful growth. While I understand that it may be a bit naive to expect dividend growth on an asset that is already sporting a double-digit yield, I still think that a negative dividend growth over this time frame is an indication of the overall quality of the portfolio of investments.

Seeking Alpha

Ideally, long-term holders would want to see a dividend rate that remains the same at the very least. This would help instill a higher level of confidence that management values the distribution and will take measures to ensure it never has to get reduced. As previously mentioned, adjusted net investment income per share landed at $0.38 for Q2.

This means that NII covers the distribution of $0.34 per share at a rate of 111.7%. While it’s great that the distribution is currently being covered, I remain cautious about what will happen when interest rates get cut and earnings are reduced. Interest rates rose to the highest level they’ve been over the last decade. While TCPC was able to capitalize and issue over several supplemental distributions to shareholders, it’s been a bit disappointing to see that the quarterly rate has never recovered back to its pre-pandemic levels.

Valuation

TCPC’s recent price drop has made it trade at a sizeable discount to NAV, so this may be a good time to enter if you believe there will be a turnaround. The price currently trades at a discount to NAV of 11.37%. For reference, the price has traded at an average discount to NAV of 7% over the last three-year period. However, I believe that the discount may get larger if performance doesn’t improve and non-accruals continue to grow. Wall St. seems to agree with this outlook, as they currently have an average price target of $8.83 per share. This represents a potential downside of about 2.3% from the current level.

CEF Data

In a scenario where the interest rates continue to remain elevated, non-accruals could continue to increase, and the NAV will likely deteriorate further. However, interest rate cuts are likely on the horizon based on the latest economic data. For instance, the unemployment rate has steadily climbed over the last year and now sits at 4.3%. Similarly, the inflation rate has consistently trended downward over the last four months, and now it’s at the 2.9% level. This is getting closer to the Fed’s 2% target and may increase the probability of a rate cut. Lastly, the US Presidential elections are upcoming and may cause elevated levels of market volatility and uncertainty. The combination of these factors may be enough to incentivize the Fed to begin reducing rates.

Rate cuts will likely impact NII per share, but there’s also a chance that this can help boost the portfolio growth for TCPC. Lower interest rates will make the environment for borrowing a lot more affordable. As a result, there may be higher volumes of potential borrowers that TCPC can use to help bolster their portfolio strength and overall health. Additionally, lower rates would mean that existing borrowers may get some relief as their required debt maintenance amount goes down. However, the rapidly rising non-accruals may indicate a deeper issue with the underwriting strategies that are implemented by management. For now, I prefer to stay away from TCPC, as there are better alternatives in the BDC space.

Takeaway

In conclusion, TCPC’s portfolio quality has continued to deteriorate as a result of higher interest rates. In addition, the BDC has realized higher losses and caused net investment income levels to shrink as well. Non-accruals have increased over the last quarter and may be an indication that of lax underwriting criteria. While the distribution is still full covered, I remain cautious about how higher interest rates will negatively affect their portfolio’s earnings potential. If you believe that they will be able to manage, TPCP trades at a higher discount to NAV than average and may be an opportune time for entry for the risk-averse investors. You’d be able to lock in a higher yield at this level and create a sizeable income stream. However, I prefer to stay away as there are many alternative BDC choices that are performing well.

Read the full article here

")